|

|

|

|

|||||

|

|

|

Over the past six months, Markel Group has been a great trade, beating the S&P 500 by 6.6%. Its stock price has climbed to $1,977, representing a healthy 11.8% increase. This run-up might have investors contemplating their next move.

Is there a buying opportunity in Markel Group, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

We’re glad investors have benefited from the price increase, but we don't have much confidence in Markel Group. Here are three reasons why we avoid MKL and a stock we'd rather own.

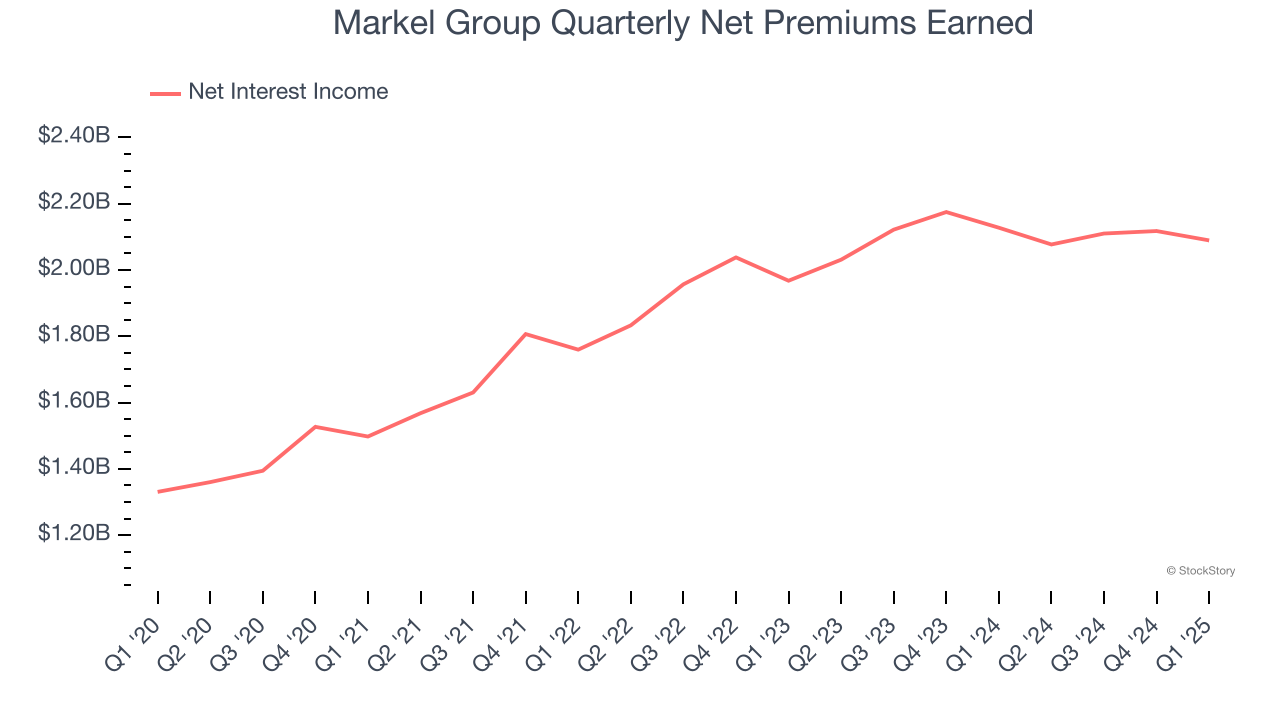

While insurers generate revenue from multiple sources, investors view net premiums earned as the cornerstone - its direct link to core operations stands in sharp contrast to the unpredictability of investment returns and fees.

Markel Group’s net premiums earned has grown at a 3.8% annualized rate over the last two years, worse than the broader insurance industry and slower than its total revenue.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Markel Group’s revenue to stall, a deceleration versus its 10.6% annualized growth for the past two years. This projection is underwhelming and implies its products and services will face some demand challenges.

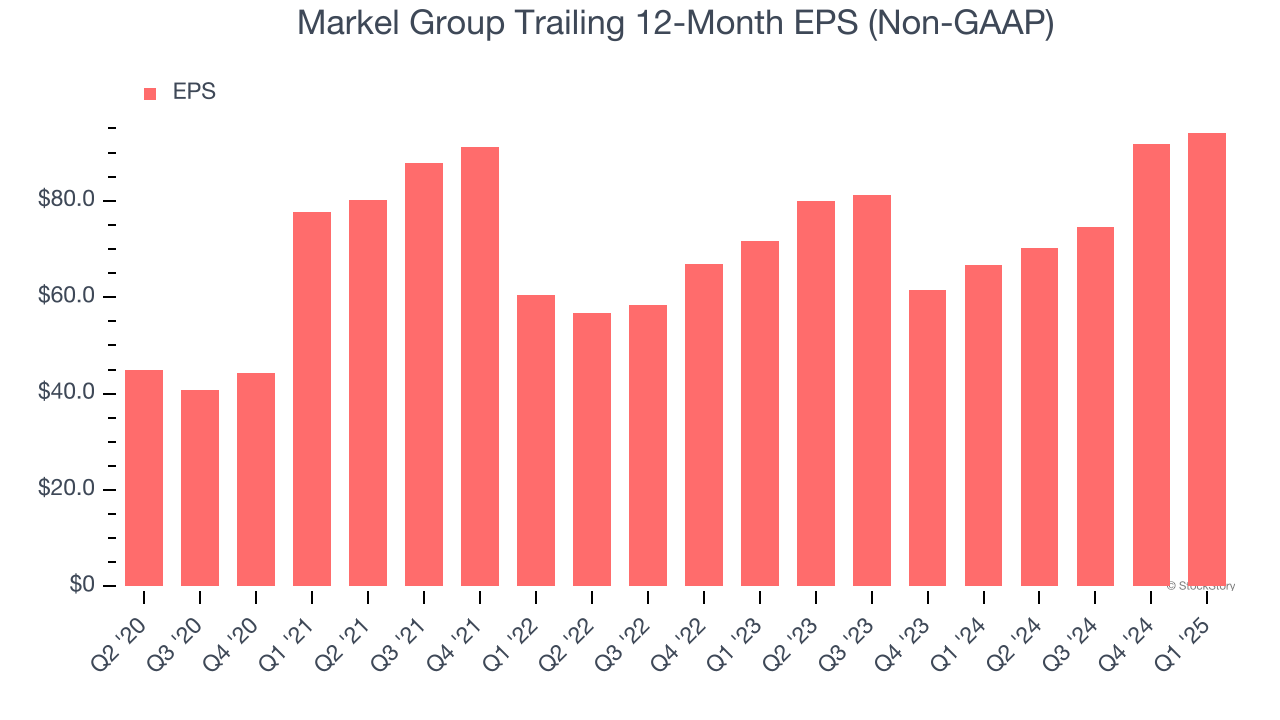

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Markel Group’s EPS grew at an unimpressive 14.7% compounded annual growth rate over the last two years. On the bright side, this performance was higher than its 10.6% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

Markel Group isn’t a terrible business, but it doesn’t pass our bar. With its shares beating the market recently, the stock trades at 1.4× forward P/B (or $1,977 per share). This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now. We’d suggest looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| 12 hours | |

| Mar-12 | |

| Mar-11 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 | |

| Mar-03 | |

| Feb-28 | |

| Feb-26 | |

| Feb-24 | |

| Feb-23 | |

| Feb-22 | |

| Feb-20 | |

| Feb-20 |

Markel and Upfort collaborate on cyber risk tools for US policyholders

MKL

Life Insurance International

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite