|

|

|

|

|||||

|

|

|

Shareholders of Booz Allen Hamilton would probably like to forget the past six months even happened. The stock dropped 23% and now trades at $105. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Following the drawdown, is this a buying opportunity for BAH? Find out in our full research report, it’s free.

With roots dating back to 1914 and deep ties to nearly all U.S. cabinet-level departments, Booz Allen Hamilton (NYSE:BAH) provides management consulting, technology services, and cybersecurity solutions primarily to U.S. government agencies and military branches.

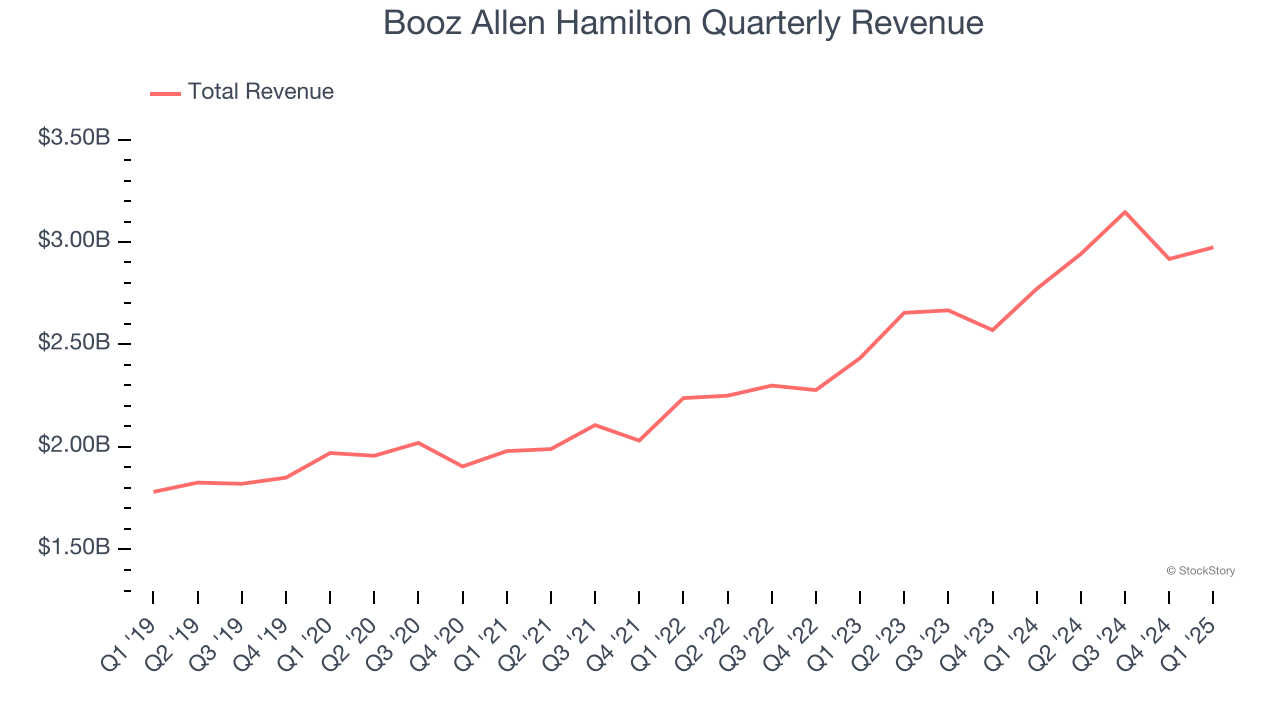

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Booz Allen Hamilton’s 9.9% annualized revenue growth over the last five years was impressive. Its growth beat the average business services company and shows its offerings resonate with customers.

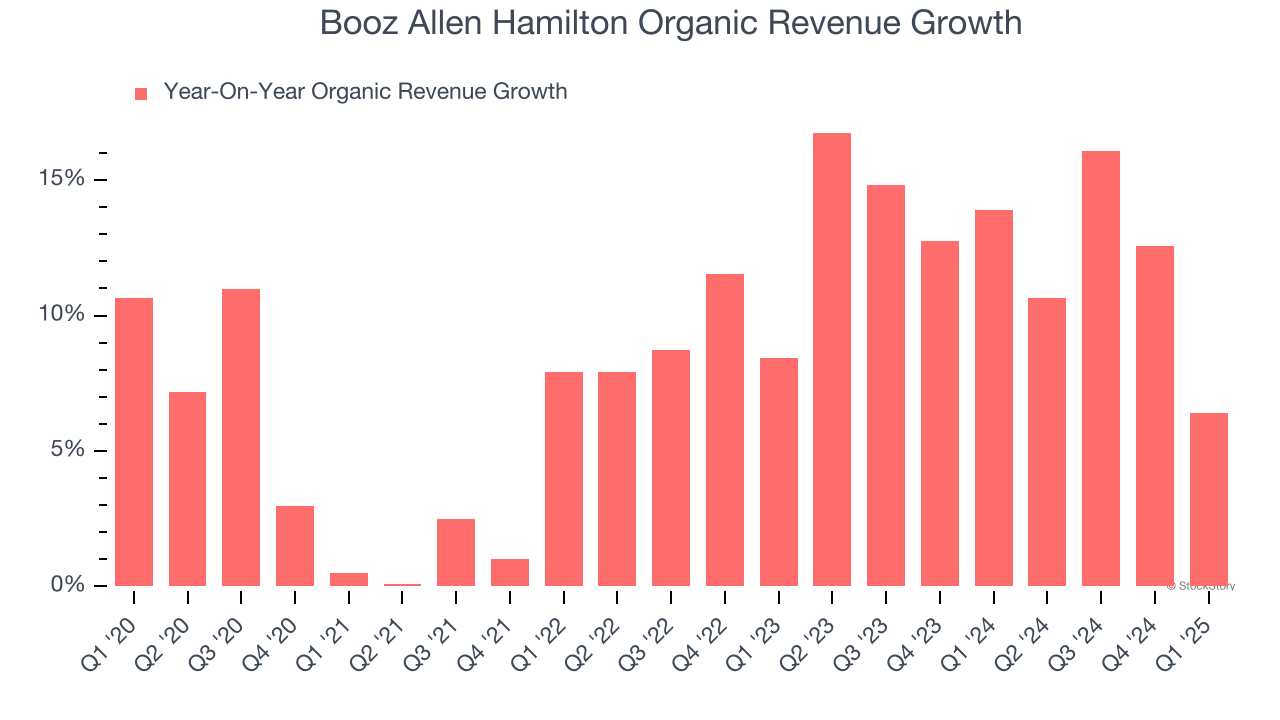

We can better understand Government & Technical Consulting companies by analyzing their organic revenue. This metric gives visibility into Booz Allen Hamilton’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Booz Allen Hamilton’s organic revenue averaged 13% year-on-year growth. This performance was impressive and shows it can expand quickly without relying on expensive (and risky) acquisitions.

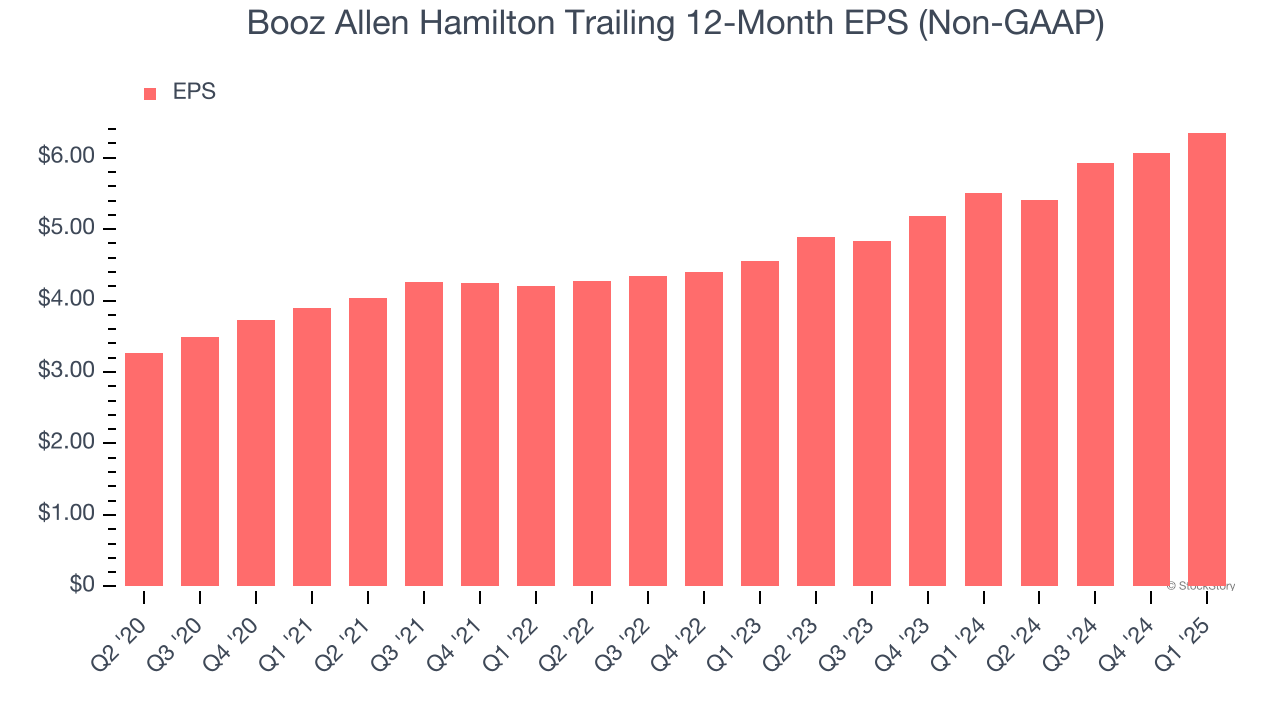

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Booz Allen Hamilton’s EPS grew at an astounding 16.3% compounded annual growth rate over the last five years, higher than its 9.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

These are just a few reasons Booz Allen Hamilton is a high-quality business worth owning. After the recent drawdown, the stock trades at 15.2× forward P/E (or $105 per share). Is now the right time to buy? See for yourself in our in-depth research report, it’s free.

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| 12 hours | |

| Mar-26 | |

| Mar-24 | |

| Mar-20 | |

| Mar-15 | |

| Mar-11 | |

| Mar-10 | |

| Mar-06 | |

| Mar-05 | |

| Mar-04 | |

| Mar-02 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite