|

|

|

|

|||||

|

|

|

Tesla TSLA is slated to release second-quarter 2025 results on July 23, after market close. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings and revenues is pegged at 40 cents per share and $22.61 billion, respectively.

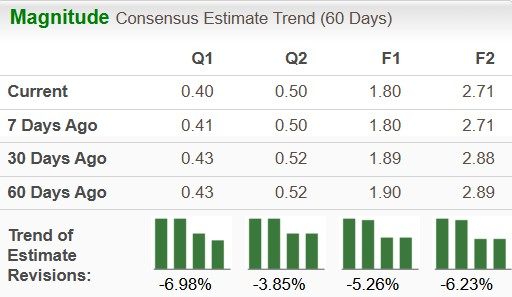

The earnings estimate for the to-be-reported quarter has been revised downward by 1 cent over the past seven days. The bottom-line projection indicates a year-over-year decline of 23%. The Zacks Consensus Estimate for quarterly revenues suggests a year-over-year contraction of 11.3%.

For the current year, the Zacks Consensus Estimate for TSLA’s revenues is pegged at $94.5 billion, implying a decline of 3.3% year over year. The consensus mark for 2025 EPS is pegged at $1.80, suggesting a drop of around 26% on a year-over-year basis.

In the trailing four quarters, this electric vehicle (EV) giant missed EPS estimates on three occasions and beat on the other, with the average negative earnings surprise being 8.33%.

Tesla, Inc. price-eps-surprise | Tesla, Inc. Quote

Our proven model does not conclusively predict an earnings beat for Tesla. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. That’s not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

TSLA has an Earnings ESP of +0.82% and a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank stocks here.

(See the Zacks Earnings Calendar to stay ahead of market-making news.)

Tesla delivered 384,122 vehicles globally in the quarter, including 373,728 Model 3/Y units and 10,394 other models. This marks a 13.5% decline year over year—the sharpest drop in Tesla’s history—and the second straight quarter of falling deliveries. The figure also fell short of our estimate of 420,079 units.

It should be noted that Tesla’s struggle isn’t reflective of the broader EV market — other players are growing just fine.General Motors GM delivered 46,280 EVs in the quarter under discussion, more than double its sales from the year-ago period. Last year, General Motors sold roughly 114,000 EVs in the United States, surpassing the 100,000 mark for the first time. China’s BYD Co Ltd BYDDY continues to challenge Tesla. In the second quarter of 2025, BYD reported 606,993 BEVs sold (up 42.5% year over year), marking its third straight quarter of beating Tesla in battery EV sales.

Notably, Tesla is now producing more than it’s selling, suggesting a demand slowdown. Europe saw the steepest sales decline, highlighting waning brand strength. An aging vehicle lineup and CEO Elon Musk’s divisive public image are hurting Tesla’s appeal amid intensifying competition.

We expect Tesla’s automotive revenues to fall more than 6% in the to-be-reported quarter. Automotive gross margin is likely to shrink to 15%, down 3 percentage points from the prior year.

On a brighter note, Tesla’s Energy Generation and Storage business is gaining traction. The company deployed 9.6 GWh of energy storage in the second quarter, slightly up from 9.4 GWh a year ago. We estimate segment revenues to hit $3.03 billion, showing growth both quarterly and annually. Services/Other revenues are estimated to be $3.15 billion, up 20% year over year. But these units form a small part of the company’s total revenues, not enough to offset the sluggish performance of the automotive business.

High operating and capital expenses are likely to clip profits and cash flows. Tesla continues to spend heavily on expanding production, battery technology, its Supercharger network, AI initiatives, and new product development.

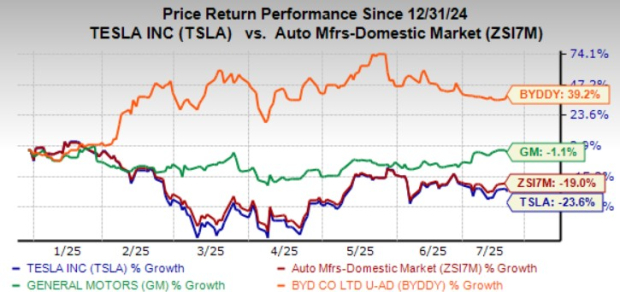

Year to date, shares of Tesla have contracted more than 23%, underperforming the industry as well as peers like General Motors and BYD.

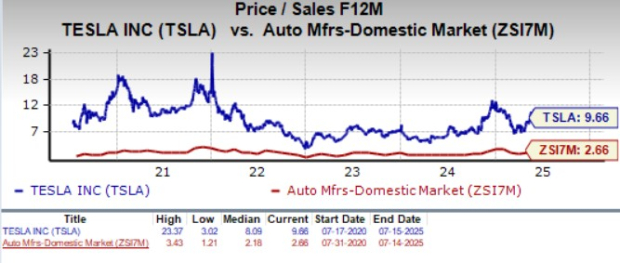

Tesla stock is also quite overvalued. Going by its price/sales ratio, the company is trading at a forward sales multiple of 9.66, higher compared to the industry as well as its own 5-year average.

Tesla heads into its second-quarter earnings report with growing questions about its core business. With no major new mainstream vehicle launches in years, Tesla is struggling to rekindle demand. Minor refreshes of existing models aren’t cutting it, especially as competitors flood the market with more innovative, affordable and stylish electric vehicles. Additionally, the “Musk factor” is becoming a real drag. Musk’s increasingly polarizing online behavior and political commentary are turning off some potential customers, further denting brand perception.

The once hyper-growth EV maker now faces a real risk of delivering fewer vehicles in 2025 than in 2024—a potential second straight year of declining sales. That’s a far cry from its earlier target of 50% annual growth.

Tesla’s much-hyped robotaxi rollout in Austin isn’t offering relief. The service launched in a limited, supervised form in Austin is facing early growing pains. Test vehicles have struggled with basic driving functions like lane changes and intersection handling. With a human safety driver still required and rivals like Waymo and Baidu well ahead in autonomy, Tesla’s robotaxi dream may be further from reality than investors had hoped.

The company’s upcoming earnings are likely to disappoint, adding to the stock’s volatility. With demand softening, competition heating up and execution risks piling on, the near-term outlook remains challenging. At this point, it’s best to avoid betting on Tesla. In fact, if you’re sitting on gains, now may be a smart time to lock them in and reduce exposure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite