|

|

|

|

|||||

|

|

|

Nebius stock has soared impressively this year, and its rise seems justified considering its outstanding growth and solid prospects.

Goldman Sachs believes that the stock remains undervalued when its growth potential is taken into account.

The Nvidia-backed cloud AI infrastructure provider has a strong balance sheet that should allow it to quickly expand capacity and win more business.

Nebius Group (NASDAQ: NBIS) has been one of the hottest stocks on the market in 2025, rising a whopping 92% as of July 16. It looks like the cloud computing company's red-hot rally is here to stay, thanks to a huge addressable market and positive Wall Street sentiment.

The Dutch company is in the business of providing artificial intelligence (AI) cloud infrastructure to customers. Its full-stack AI infrastructure allows developers and customers to rent powerful graphics processing units (GPUs) from the likes of Nvidia (NASDAQ: NVDA) on an hourly basis so that they can train and fine-tune models, run inference tasks, and create custom AI solutions with the help of third-party tools.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Let's take a closer look at what Nebius does, and check why this AI stock is expected to soar higher even after clocking phenomenal gains so far in 2025.

Image source: Getty Images.

Nebius customers can scale from a single GPU to large clusters based on their requirements, and they can use popular large language models (LLMs) from DeepSeek, Microsoft, Meta Platforms, Stability AI, and others to build apps. The company has made its name by offering top Nvidia GPUs such as the H100 and the H200, and claims that its customers "will be among the first to gain access to NVIDIA's next-generation Blackwell platform."

It's worth noting that Nvidia is an investor in Nebius. The AI cloud infrastructure provider announced a private placement financing worth $700 million in December last year. Nvidia was one of the companies that took part in this strategic financing that Nebius says was for accelerating the rollout of its full-stack infrastructure.

So, Nvidia and Nebius enjoy a close partnership. That's expected to be beneficial for the latter, since the AI chip giant is busy rolling out AI infrastructure around the globe. Importantly, Nebius' results make it clear that it is quickly making its presence felt in the fast-growing cloud AI infrastructure-as-a-service market.

The company's revenue in the first quarter of 2025 shot up by almost 5x year over year to $55.3 million. Nebius is just getting started right now, but the important thing to note here is that it's quickly building a solid revenue pipeline. The company says that its annualized run-rate revenue (ARR) increased by 684% in Q1 to $249 million, easily outpacing the growth in its top line.

Looking ahead, Nebius management is confident of achieving an ARR of $750 million to $1 billion by the end of 2025 as it rolls out more cloud capacity. The company has gone from just one location to five data center locations in the space of just three quarters, and says it is "actively exploring new sites in the U.S. and around the world."

Nebius points out that its robust balance sheet, which has over $1.4 billion in cash and only $187 million in debt, will allow it to increase its data center capacity to 100 megawatts (MW) by the end of 2025, followed by a significant increase in 2026. All this explains why the company is forecasting revenue of $500 million to $700 million in 2025, which would be a massive increase over last year's top line of $117 million, even at the lower end of the estimate.

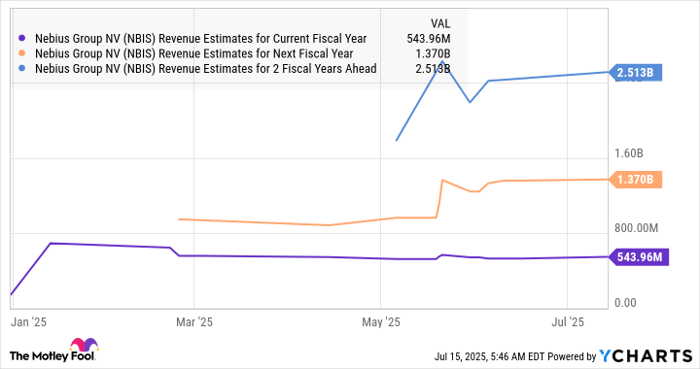

Consensus estimates are expecting Nebius' outstanding growth to continue over the next couple of years as well. That's not surprising, considering the $400 billion opportunity in the cloud AI infrastructure market.

NBIS Revenue Estimates for Current Fiscal Year data by YCharts.

So, it's easy to see why Goldman Sachs expects this AI stock to fly higher, despite its impressive rally in recent months. The investment bank believes that Nebius remains undervalued on account of the remarkable growth that it is delivering. Goldman rates Nebius as a buy and has a 12-month price target of $68 on the stock.

That points toward roughly 30% gains from current levels, though it's worth noting that Nebius stock popped 17% in a single session following Goldman's coverage. Investors, however, may be wondering if it is worth buying Nebius following its recent gains.

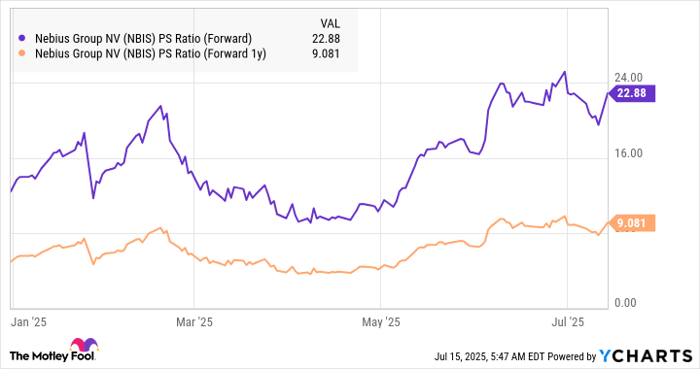

Nebius stock is trading at a rich 68 times sales right now following its phenomenal jump in 2025. But at the same time, investors should note that its stunning pace of growth justifies its expensive valuation. We have already seen that Goldman Sachs believes Nebius to be undervalued after taking its growth potential into account.

In fact, the stock's forward sales multiple is way lower than the trailing one.

NBIS PS Ratio (Forward) data by YCharts. PS = price-to-sales.

Nebius, therefore, looks like an ideal pick for growth-oriented investors right now. Its outstanding growth is likely to result in more stock market upside, just like Goldman predicts.

Before you buy stock in Nebius Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nebius Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $679,653!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,046,308!*

Now, it’s worth noting Stock Advisor’s total average return is 1,060% — a market-crushing outperformance compared to 179% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of July 15, 2025

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Goldman Sachs Group, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends Nebius Group and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 23 min | |

| 37 min | |

| 44 min | |

| 53 min | |

| 1 hour | |

| 1 hour |

Stock Market Today: Nasdaq Drops As Nvidia Plunges; Chip Spinoff Soars (Live Coverage)

NVDA -5.46%

Investor's Business Daily

|

| 1 hour |

CoreWeave Stock Falls On Q4 Earnings As Order Backlog Grows 20%

NVDA -5.46%

Investor's Business Daily

|

| 1 hour |

Nvidia Slide Shows Investors' Lukewarm Reception of Strong Earnings

NVDA -5.46%

The Wall Street Journal

|

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite