|

|

|

|

|||||

|

|

|

Over the past six months, LeMaitre’s shares (currently trading at $82.61) have posted a disappointing 16.6% loss, well below the S&P 500’s 4.5% gain. This might have investors contemplating their next move.

Is there a buying opportunity in LeMaitre, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Even with the cheaper entry price, we don't have much confidence in LeMaitre. Here are two reasons why you should be careful with LMAT and a stock we'd rather own.

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $226.3 million in revenue over the past 12 months, LeMaitre is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

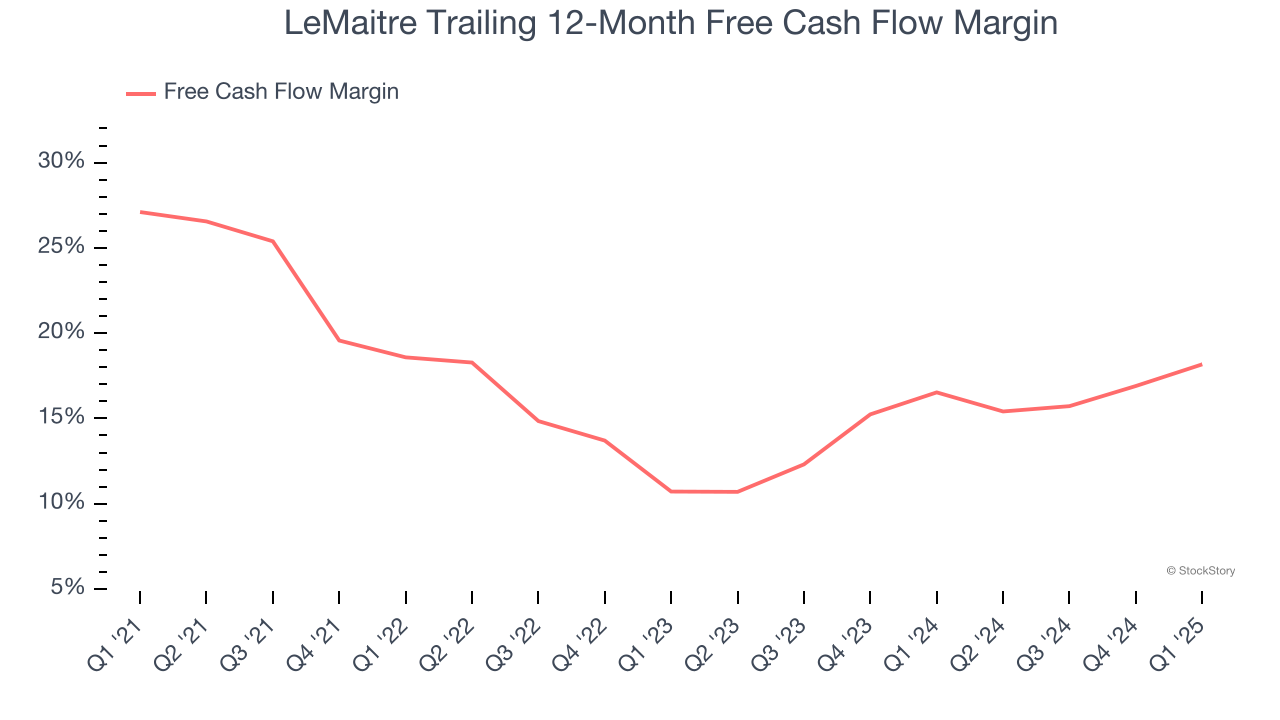

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, LeMaitre’s margin dropped by 8.9 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. LeMaitre’s free cash flow margin for the trailing 12 months was 18.2%.

LeMaitre isn’t a terrible business, but it doesn’t pass our quality test. After the recent drawdown, the stock trades at 35.7× forward P/E (or $82.61 per share). At this valuation, there’s a lot of good news priced in - we think there are better opportunities elsewhere. We’d suggest looking at the Amazon and PayPal of Latin America.

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-14 | |

| May-20 | |

| May-07 | |

| May-06 | |

| May-05 | |

| May-05 | |

| Apr-14 | |

| Apr-07 | |

| Mar-02 | |

| Feb-28 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite