|

|

|

|

|||||

|

|

|

1st Source has had an impressive run over the past six months as its shares have beaten the S&P 500 by 5.1%. The stock now trades at $63.36, marking a 9.5% gain. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now still a good time to buy SRCE? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Tracing its roots back to 1863 during the Civil War era, 1st Source Corporation (NASDAQ:SRCE) is a regional bank holding company that provides commercial, consumer, specialty finance, and wealth management services across Indiana, Michigan, and Florida.

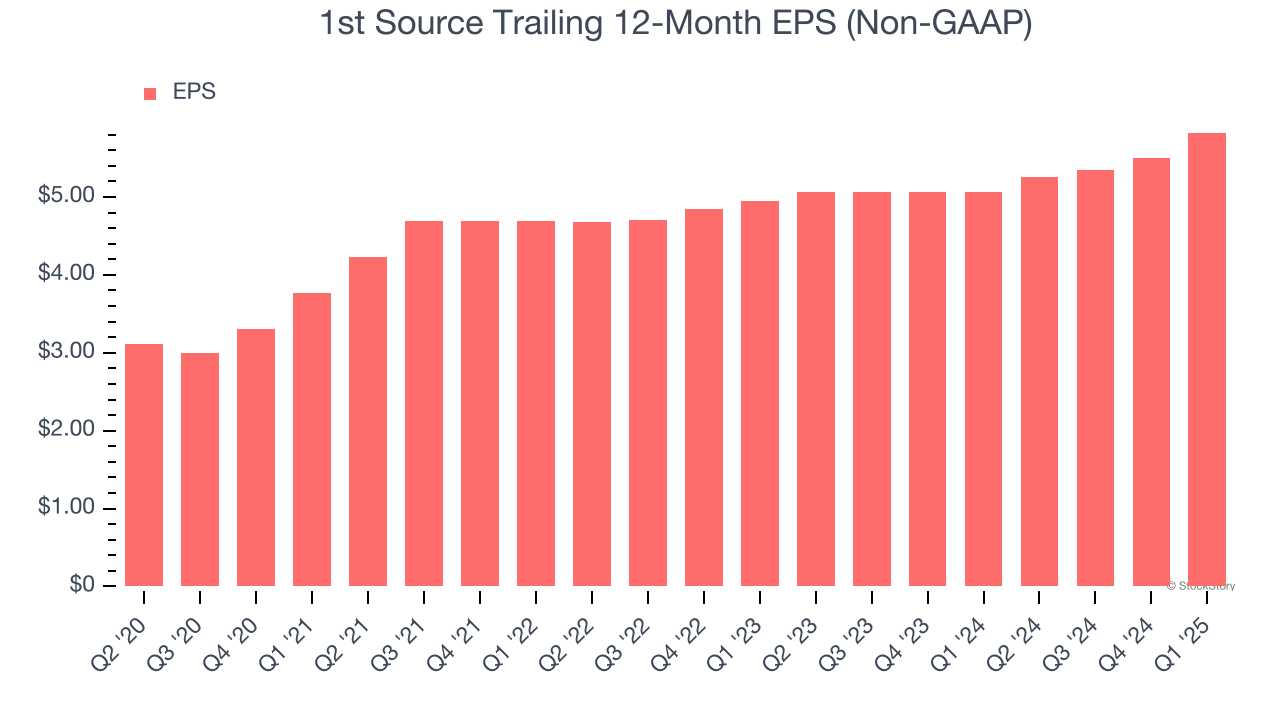

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

1st Source’s EPS grew at an astounding 12.6% compounded annual growth rate over the last five years, higher than its 4.1% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

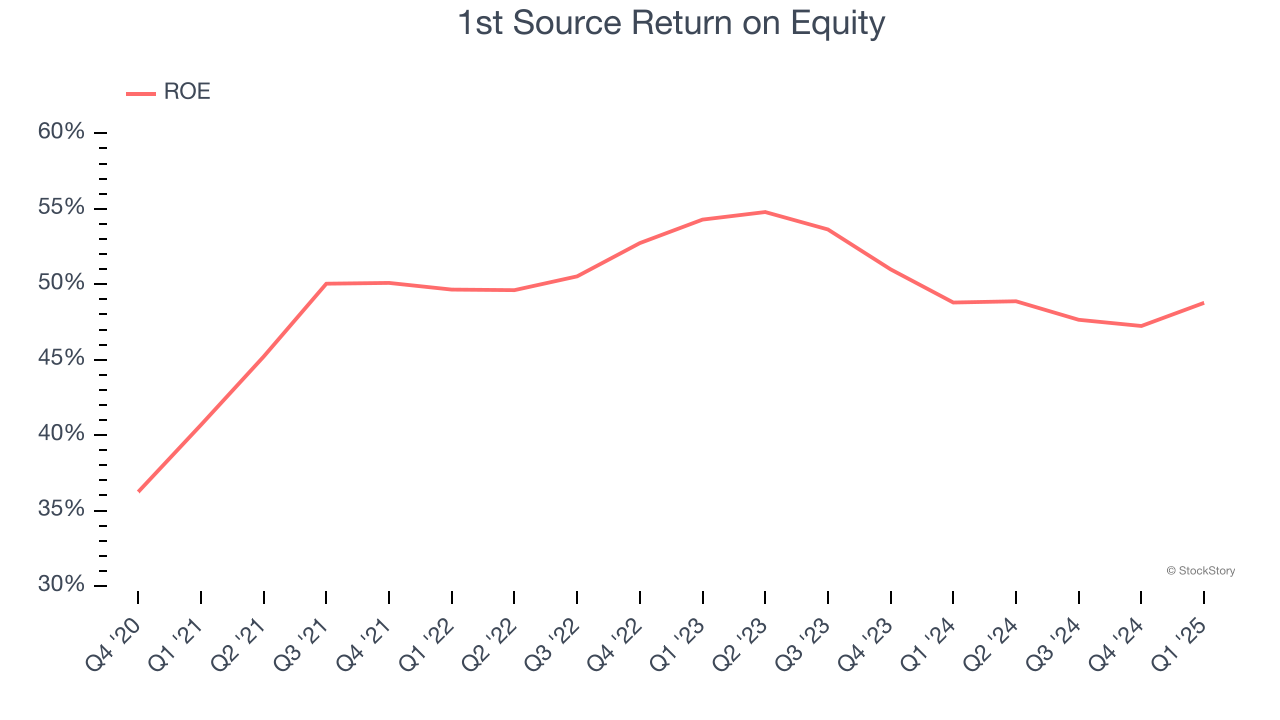

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for banks. Over a long period, banks with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, 1st Source has averaged an ROE of 12.1%, excellent for a company operating in a sector where the average shakes out around 7.5% and those putting up 15%+ are greatly admired. This shows 1st Source has a strong competitive moat.

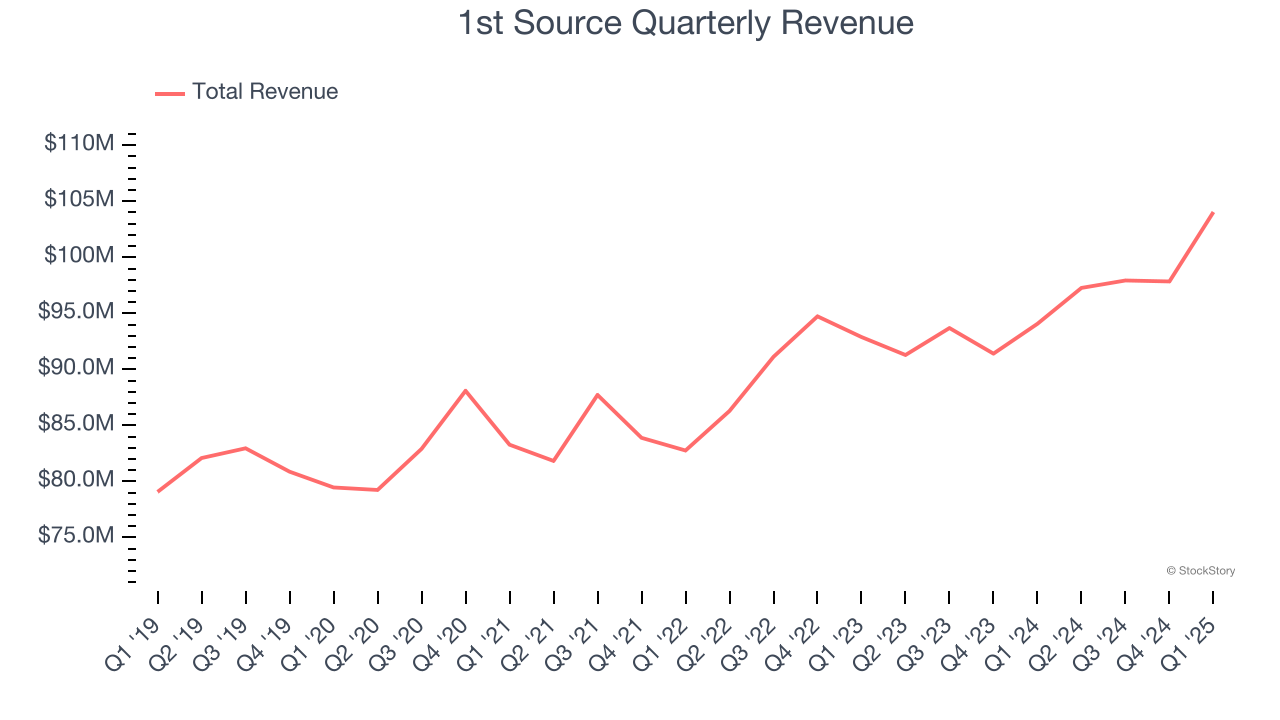

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees.

Over the last five years, 1st Source grew its revenue at a mediocre 4.1% compounded annual growth rate. This wasn’t a great result compared to the rest of the bank sector, but there are still things to like about 1st Source.

1st Source’s merits more than compensate for its flaws, and with its shares beating the market recently, the stock trades at 1.2× forward P/B (or $63.36 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-23 | |

| Jul-23 | |

| May-07 | |

| Apr-23 | |

| Apr-23 | |

| Apr-11 | |

| Mar-24 | |

| Mar-09 | |

| Feb-20 | |

| Feb-15 | |

| Feb-09 | |

| Feb-05 | |

| Feb-04 | |

| Feb-04 | |

| Jan-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite