|

|

|

|

|||||

|

|

|

Target stock is as cheap as it has been in the last five years.

The retailer remains a reliable dividend payer as a Dividend King.

Target's differentiation gives it a competitive advantage.

Not much has gone right for Target (NYSE: TGT) in recent years.

The stock has tumbled from the peak it touched during the pandemic as its sales growth slowed and then declined. Macroeconomic headwinds crimped sales in discretionary categories, but the retailer also lost market share to Walmart and Costco, and faced other challenges. More recently, the company provoked backlash and a boycott by backing away from its DEI policies.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

As a result, profits have slipped, and the stock price is about as low as it has been in about six years.

While investors have had their patience tested, the stock could finally be ready for a comeback. Let's take a look at three reasons to buy Target stock now.

Image source: Target.

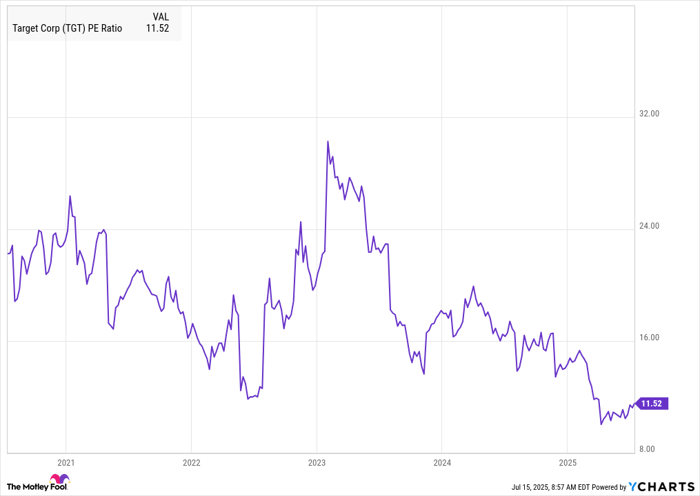

Target might be struggling, but its challenges have already been priced into the stock. The stock now trades at a price-to-earnings ratio of 11.5, which is a fraction of what investors are paying for Walmart and Costco.

Target expects earnings to fall this year, so that valuation would be higher on a forward basis, but the continued decline lowers the bar for a recovery, which should eventually come.

In conjunction with its first-quarter earnings report, Target announced it was forming what it calls an "Enterprise Acceleration Office" that has been tasked with improving speed and agility across the company, helping management make quicker decisions, bringing new products to the market, and revamping its stores.

Despite those challenges, Target still has a number of strengths that should help it return to growth. At least 10 of its owned brands generate more than $1 billion each in annual sales, among them grocery brand Good & Gather, kids apparel line Cat & Jack, and athleisure line All in Motion.

It's introducing products like new food brands and has forged shop-in-store partnerships with brands like Ulta, setting the company up for a recovery.

As the chart below shows, Target is cheaper on a price-to-earnings basis than it has been in the last five years.

TGT P2.E Ratio data by YCharts.

If investors can look past the current challenges, there's potential for Target to mount a convincing recovery, driving the stock significantly higher.

Target has long rewarded income investors. In fact, with its 54-year streak of annual payout raises, the retailer is a Dividend King. In June, the company hiked its dividend by another 1.8% to $1.14 per share, showing it remains committed to keeping that streak going even as the business is struggling. At its recent share price, its yield was 4.5%.

Despite its recent challenges, Target remains solidly profitable and its dividend is well covered. Even if its earnings land at the bottom of its guidance range for the year, its payout ratio would still be less than 70%, meaning the company should have no problem paying the dividend for the foreseeable future.

Plenty of brick-and-mortar retailers have gradually collapsed over the last decade, including department store chains, but Target remains a unique option in the retail space. It's one of only a few multicategory, national retailers, selling a wide variety from food to electronics to apparel and home goods, and it's the only one with store formats that serve customers in urban, suburban, and rural areas equally well. Unlike Walmart and Costco, most of Target's sales come from discretionary goods categories, and it has built a reputation for selling "cheap chic" merchandise.

Management has said it recognizes that it needs to get back to delivering the "Tarzhay" magic that helped differentiate the company historically, and I think the company can do that.

It might take a few years, given the reputational damage it incurred with its retreat from DEI and the broader pressures it will face from tariffs and other macroeconomic headwinds, which will take a toll on consumer discretionary spending. However, with its same-day delivery options, its popular owned brands, and its ability to reach customers in all demographics, Target should eventually find its way back to growth.

Before you buy stock in Target, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Target wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $674,281!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,050,415!*

Now, it’s worth noting Stock Advisor’s total average return is 1,058% — a market-crushing outperformance compared to 179% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of July 15, 2025

Jeremy Bowman has positions in Target. The Motley Fool has positions in and recommends Costco Wholesale, Target, and Walmart. The Motley Fool has a disclosure policy.

| 33 min | |

| 35 min | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite