|

|

|

|

|||||

|

|

|

As the Q1 earnings season wraps, let’s dig into this quarter’s best and worst performers in the leisure facilities industry, including Sphere Entertainment (NYSE:SPHR) and its peers.

Leisure facilities companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted their spending from "things" to "experiences". Leisure facilities seek to benefit but must innovate to do so because of the industry's high competition and capital intensity.

The 11 leisure facilities stocks we track reported a mixed Q1. As a group, revenues missed analysts’ consensus estimates by 1.1% while next quarter’s revenue guidance was in line.

Luckily, leisure facilities stocks have performed well with share prices up 16.6% on average since the latest earnings results.

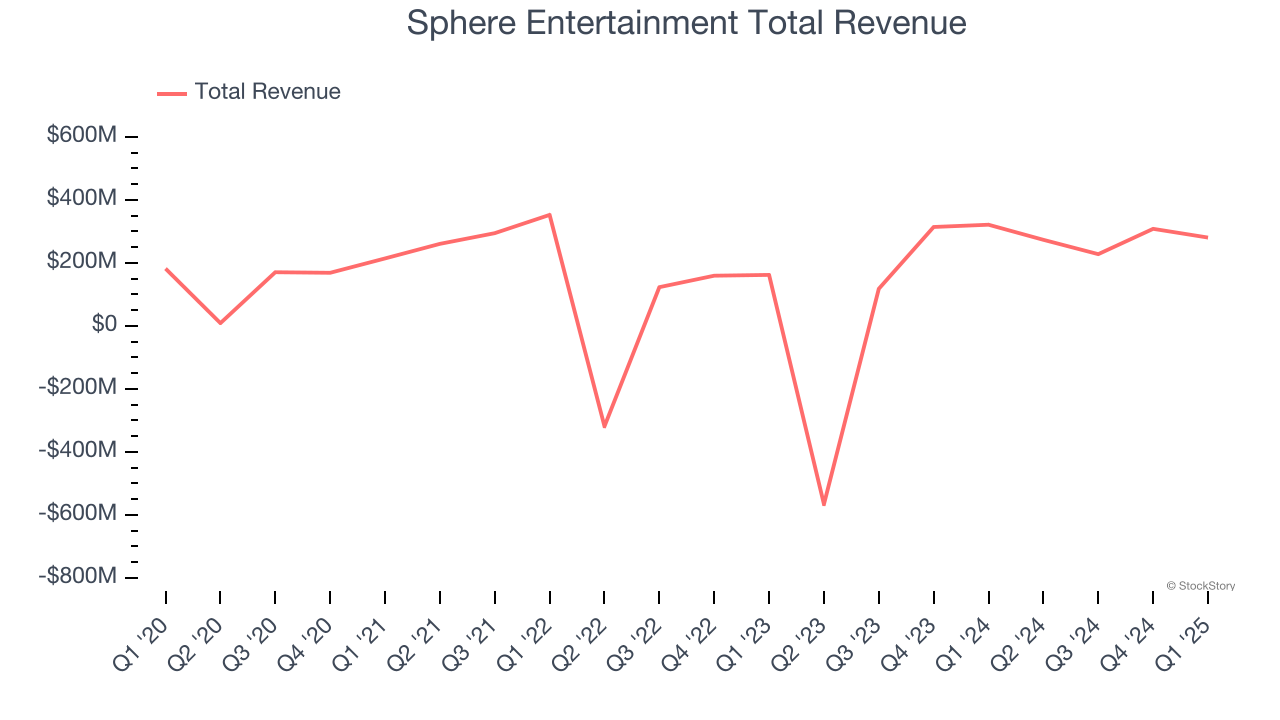

Famous for its viral Las Vegas Sphere venue, Sphere Entertainment (NYSE:SPHR) hosts live entertainment events and distributes content across various media platforms.

Sphere Entertainment reported revenues of $280.6 million, down 12.7% year on year. This print fell short of analysts’ expectations by 5.6%, but it was still a strong quarter for the company with a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ EPS estimates.

Executive Chairman and CEO James L. Dolan said, "Our Sphere segment generated positive adjusted operating income in the first quarter as we make progress on our strategic priorities for the business. We remain confident in the opportunities ahead for Sphere and our ability to drive growth this calendar year."

Sphere Entertainment delivered the weakest performance against analyst estimates and slowest revenue growth of the whole group. Interestingly, the stock is up 51.3% since reporting and currently trades at $44.98.

Is now the time to buy Sphere Entertainment? Access our full analysis of the earnings results here, it’s free.

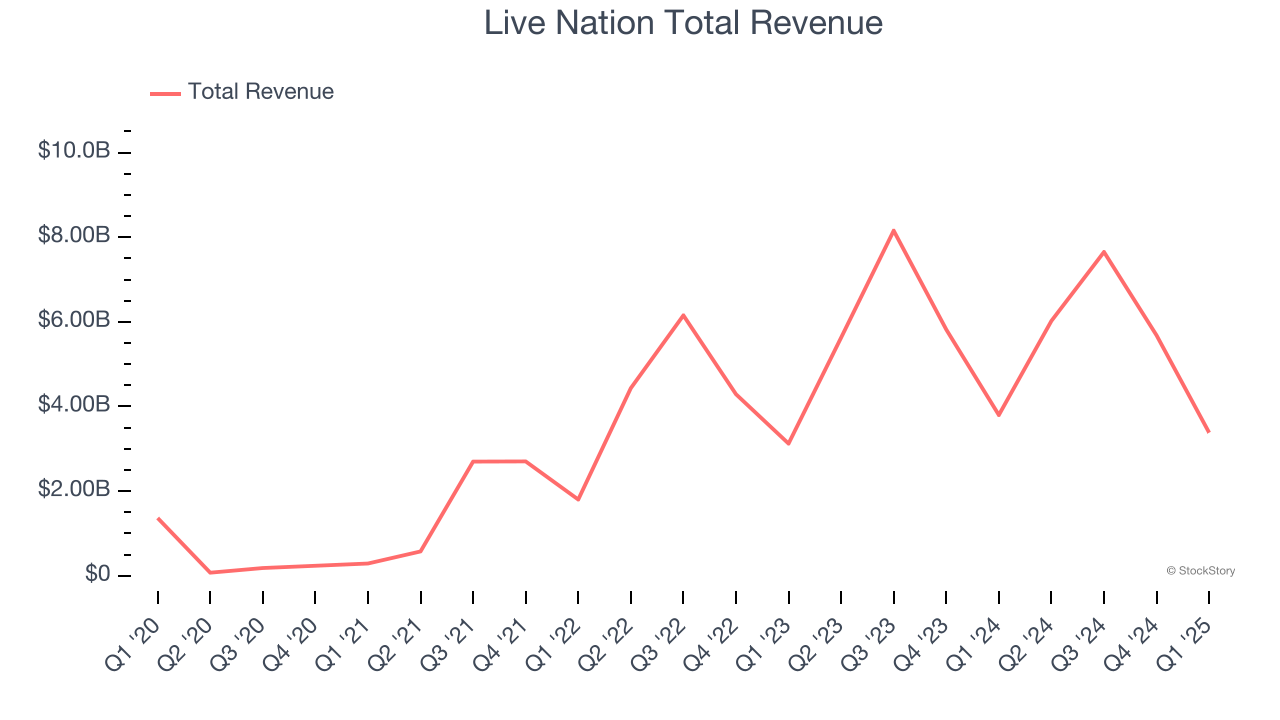

Owner of Ticketmaster and operator of music festival EDC, Live Nation (NYSE:LYV) is a company specializing in live event promotion, venue management, and ticketing services for concerts and shows.

Live Nation reported revenues of $3.38 billion, down 11% year on year, falling short of analysts’ expectations by 2.8%. However, the business still had a very strong quarter with an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

The market seems happy with the results as the stock is up 14.9% since reporting. It currently trades at $150.72.

Is now the time to buy Live Nation? Access our full analysis of the earnings results here, it’s free.

Born from the transformation of traditional bowling alleys into modern entertainment destinations, Lucky Strike (NYSE:LUCK) operates bowling alleys and other entertainment venues with upscale amenities, arcade games, and food and beverage services across North America.

Lucky Strike reported revenues of $339.9 million, flat year on year, falling short of analysts’ expectations by 5.5%. It was a disappointing quarter as it posted a significant miss of analysts’ EPS estimates and a miss of analysts’ adjusted operating income estimates.

Interestingly, the stock is up 7.1% since the results and currently trades at $10.20.

Read our full analysis of Lucky Strike’s results here.

Formed between the merger of Callaway and Topgolf, Topgolf Callaway (NYSE:MODG) sells golf equipment and operates technology-driven golf entertainment venues.

Topgolf Callaway reported revenues of $1.09 billion, down 4.5% year on year. This print beat analysts’ expectations by 2.2%. More broadly, it was a satisfactory quarter as it also produced an impressive beat of analysts’ EPS estimates but full-year EBITDA guidance missing analysts’ expectations significantly.

Topgolf Callaway had the weakest full-year guidance update among its peers. The stock is up 20.3% since reporting and currently trades at $9.53.

Read our full, actionable report on Topgolf Callaway here, it’s free.

Founded by two brothers who purchased a struggling gym, Planet Fitness (NYSE:PLNT) is a gym franchise that caters to casual fitness users by providing a friendly and inclusive atmosphere.

Planet Fitness reported revenues of $276.7 million, up 11.5% year on year. This number came in 1.2% below analysts' expectations. Zooming out, it was a mixed quarter as it also recorded an impressive beat of analysts’ adjusted operating income estimates but a miss of analysts’ EPS estimates.

Planet Fitness delivered the fastest revenue growth among its peers. The stock is up 8.2% since reporting and currently trades at $110.14.

Read our full, actionable report on Planet Fitness here, it’s free.

The Fed’s interest rate hikes throughout 2022 and 2023 have successfully cooled post-pandemic inflation, bringing it closer to the 2% target. Inflationary pressures have eased without tipping the economy into a recession, suggesting a soft landing. This stability, paired with recent rate cuts (0.5% in September 2024 and 0.25% in November 2024), fueled a strong year for the stock market in 2024. The markets surged further after Donald Trump’s presidential victory in November, with major indices reaching record highs in the days following the election. Still, questions remain about the direction of economic policy, as potential tariffs and corporate tax changes add uncertainty for 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| May-22 | |

| May-22 | |

| May-14 | |

| May-05 | |

| May-05 | |

| May-01 | |

| Apr-30 | |

| Apr-03 | |

| Apr-02 |

Sphere Entertainment Scores Positive Wall Street Reports. Stock Hits Record High.

SPHR +6.18%

Investor's Business Daily

|

| Mar-20 | |

| Mar-18 | |

| Mar-08 |

The Knicks Are Undervalued. Fixing That Will Be Harder Than Winning a Championship.

SPHR

The Wall Street Journal

|

| Mar-06 | |

| Mar-06 | |

| Mar-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite