|

|

|

|

|||||

|

|

|

Shares of Viking Therapeutics soared last year on high hopes for its obesity drug VK2735.

The stock stumbled beginning in November of last year, however, seemingly on concerns over manufacturing costs.

In retrospect, this action mirrors a pattern dished out by other biopharma names in similar situations, often leading to a rally.

Any investor who owned Viking Therapeutics (NASDAQ: VKTX) before November of last year is sure to be disappointed and maybe even a little worried. Shares are down nearly 60% since October last year and lower to the tune of 68% from their early 2024 high after soaring in 2023. Yikes.

If you were on this wild ride, don't panic yet. And for interested newcomers, the sell-off may arguably be a buying opportunity. Here's why: History says this kind of sharp rise and fall in biopharma stock prices often precedes a slower but more even and more-rewarding rally.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

But first things first.

Never heard of it? It wouldn't be surprising if you hadn't. Its $3.5 billion market cap doesn't turn many heads. It's a pre-revenue company too, which of course means it's also pre-profit.

That doesn't mean it's not worth owning even if it is inherently risky -- and volatile. It just means you'll want to handle it differently if you choose to handle it at all.

And you just might want to, given Viking's developmental pipeline.

This company's currently testing four different drugs in five different clinical trials, each of which is aimed at relatively rare metabolic and endocrine disorders. Its highest-profile drug is also the one that's furthest along the developmental trail. That's an injectable form of an anti-obesity drug currently referred to as VK2735. Its molecular structure is similar to that of the approved GLP-1 weight-loss drugs Ozempic from Novo Nordisk (NYSE: NVO) and Eli Lilly's (NYSE: LLY) Zepbound.

In fact, the differences are significant enough to avoid patent infringement challenges. VK2735 began phase 3 testing earlier this year, which is the final stage of trials necessary before the U.S. Food and Drug Administration (FDA) makes its ultimate approval decision.

And this is a big reason Viking Therapeutics has been so volatile since 2022. As the drug in question has worked its way through the lengthy testing process, investors have pre-emptively purchased shares in anticipation of good news.

Image source: Getty Images.

However, as is so often the case with biopharma stocks of companies working on game-changing drugs, the market has overshot its target more than once and then suffered a sizable setback.

That's what happened beginning in November of last year, anyway. The company announced solid testing results for VK2735. But the market panicked over concerns that manufacturing the phase 2 drug therapy's injectable version and an orally administered version simultaneously could prove quite costly.

The stock's been pressured lower ever since, even though the underlying story hasn't actually changed much in the meantime. The fickle crowd trading this stock has simply decided to see the glass as half-empty rather than half-full. It happens.

The thing is, it's not like this same story hasn't played out many times within the biopharma realm. When the drug in question is the real deal though, a recovery typically takes shape, eventually carrying the ticker in question to much higher highs.

One doesn't need to look that far back in time to see that transpire.

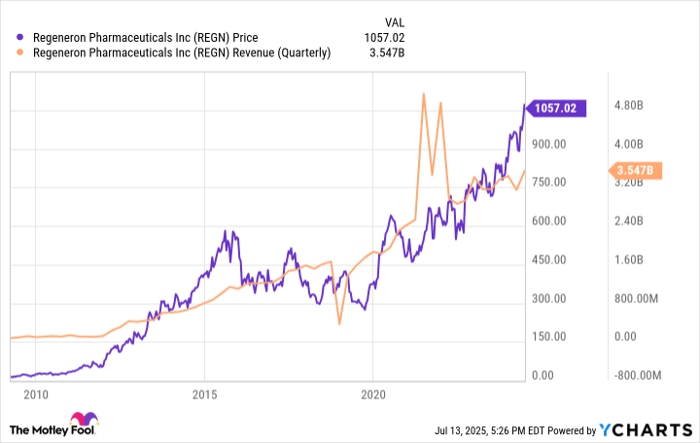

Take Regeneron Pharmaceuticals (NASDAQ: REGN) as an example. Although it's got a handful of drugs in its portfolio, eczema and asthma treatment Dupixent is its breadwinner, making up the single-biggest source of Regeneron's revenue. Eylea is a respectable close second; there is no close third. The ongoing sales growth of both drugs is a big reason this stock gained so much between late 2019 and late last year. Hope for both was also the reason Regeneron shares soared between 2010 and 2015.

There was a stretch of time between 2015 and 2019, however, when shares just weren't finding any traction even though Dupixent was approved to treat atopic dermatitis in 2017 and won its approval as an asthma treatment in 2018. It took a handful of more approvals of Dupixent through 2021 to light a lasting fire under the stock.

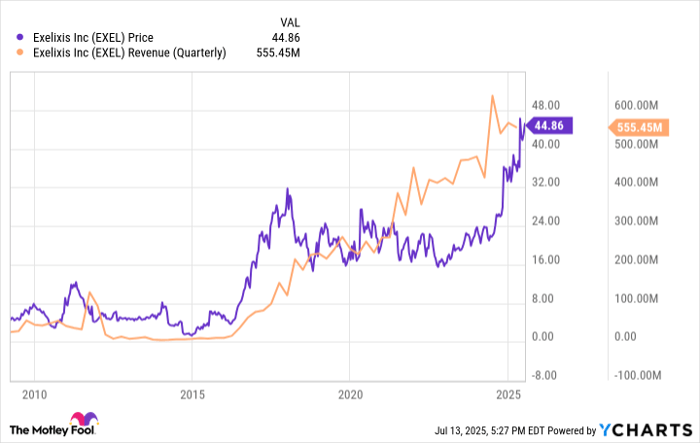

Then there's Exelixis (NASDAQ: EXEL). This stock went nowhere between 2017 and 2023 but has doubled in value since then thanks to the rapid sales growth of its oncology drug Cabometyx. In fact, its revenue reached $511 million last quarter versus $376 million for the comparable quarter a year earlier. The thing is, Cabometyx was actually first approved by the FDA back in 2016 and won several more approvals through 2021 that started driving real sales growth that same year. The market just chose to sit on the fence for a couple more years.

If you need more examples of biopharma stocks that climbed and fell out of sync despite the progress being made by the company, there are many more -- Iovance Therapeutics, ACADIA Pharmaceuticals, and CRISPR Therapeutics are just to name a few. It happens all the time.

The bigger point is, there's a frequent disconnect between a biopharma company's stock and that biopharma company's developmental and fiscal progress. Often times, investors plow in too much and too soon. At other times, they're surprisingly late, perhaps wary of another market pullback.

When the drug in question shows true potential, sooner or later the market figures it out and properly prices in its success, as it did for Regeneron and Exelixis.

But aren't Novo Nordisk and Eli Lilly already established players with very similar obesity drugs? Fair enough.

Just know that consumers are often quite willing to try "something else," particularly if it's easier, cheaper, faster, or more convenient than established alternatives. And with Morgan Stanley's prediction that the global weight-loss drug market could swell from last year's $15 billion to a peak of $150 billion by 2035, there's arguably more than enough business -- and growth -- to make Viking Therapeutics' VK2735 a smashing success. But probably not immediately. And that's where patience comes to the forefront. As we often say at The Motley Fool, if you are convinced about the company's business fundamentals, hold its stock for at least three years.

Viking's stock should eventually rally, most likely within a two-year time frame. After all, it shouldn't take nearly that long to at least start getting meaningful updates on the weight-loss drug's phase 3 testing.

Perhaps the bigger concern here should be the potential cost of manufacturing VK2735 in both an injectable and an oral form. Even then, in light of Morgan Stanley's forecasted demand, the potential cost of simultaneously manufacturing two competing drugs seems like a modest hill to climb. Most investors are arguably too worried about that possibility. Perhaps they were just looking for the right justification to take profits on last year's red-hot run-up... a justification that has since run its course.

On that note, just remember this is still a volatile small-cap biopharma name with a speculative crowd of followers. You'll only want to dive in if you're sure you've got the patience and can handle the tricky navigation this name will almost certainly require.

Before you buy stock in Viking Therapeutics, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Viking Therapeutics wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $687,149!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,060,406!*

Now, it’s worth noting Stock Advisor’s total average return is 1,069% — a market-crushing outperformance compared to 180% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of July 15, 2025

James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends CRISPR Therapeutics, Exelixis, Iovance Biotherapeutics, and Regeneron Pharmaceuticals. The Motley Fool recommends Novo Nordisk and Viking Therapeutics. The Motley Fool has a disclosure policy.

| 8 hours | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 | |

| Mar-05 | |

| Mar-05 | |

| Mar-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite