|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Since July 2020, the S&P 500 has delivered a total return of 93.1%. But one standout stock has more than doubled the market - over the past five years, Woodward has surged 228% to $258 per share. Its momentum hasn’t stopped as it’s also gained 34% in the last six months thanks to its solid quarterly results, beating the S&P by 30%.

Is there a buying opportunity in Woodward, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

We’re glad investors have benefited from the price increase, but we're cautious about Woodward. Here are three reasons why WWD doesn't excite us and a stock we'd rather own.

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Woodward grew its sales at a sluggish 2.8% compounded annual growth rate. This fell short of our benchmarks.

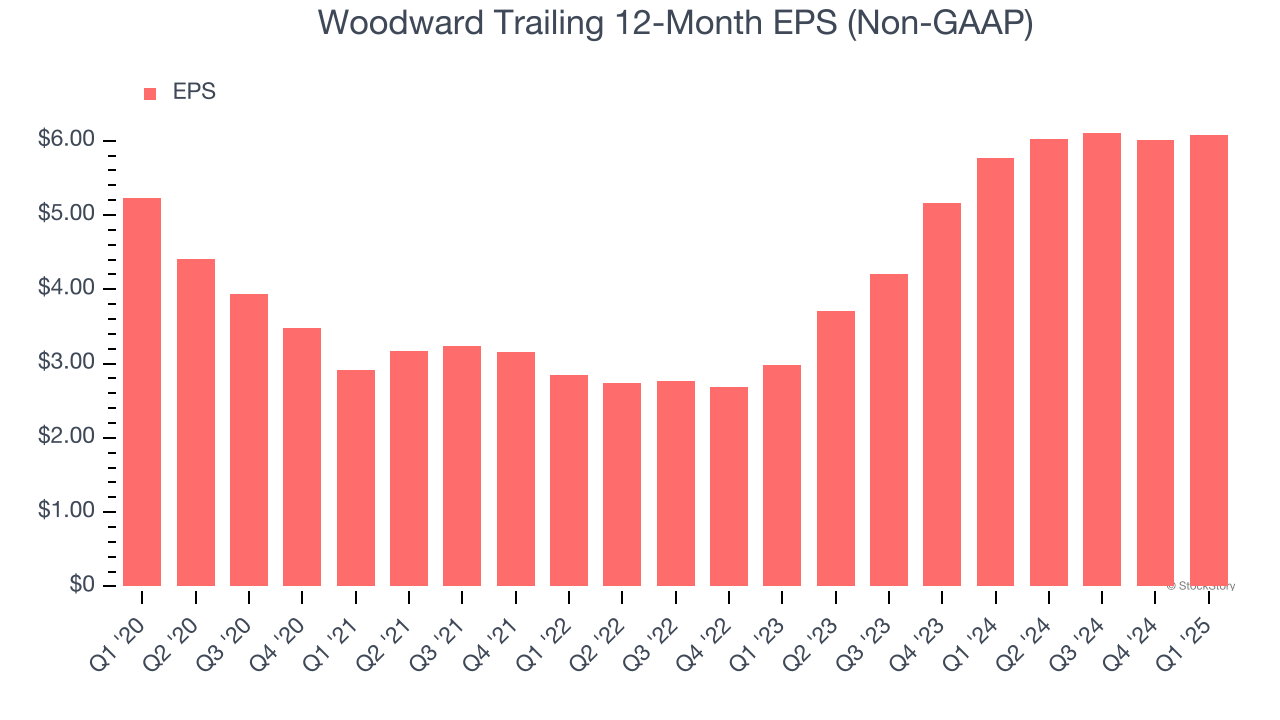

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Woodward’s weak 3.1% annual EPS growth over the last five years aligns with its revenue performance. On the bright side, this tells us its incremental sales were profitable.

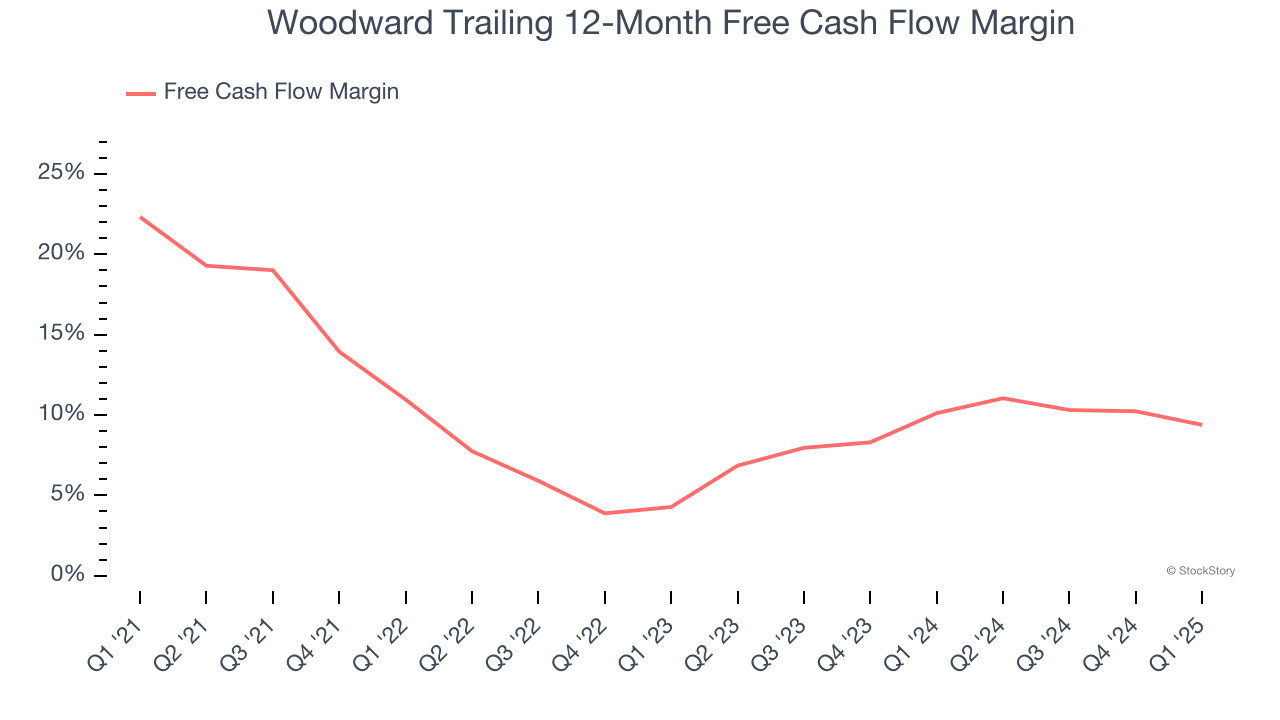

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Woodward’s margin dropped by 12.9 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Woodward’s free cash flow margin for the trailing 12 months was 9.4%.

Woodward’s business quality ultimately falls short of our standards. With its shares beating the market recently, the stock trades at 39× forward P/E (or $258 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now. We’d recommend looking at our favorite semiconductor picks and shovels play.

Trump’s April 2024 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Feb-20 | |

| Feb-18 | |

| Feb-18 | |

| Feb-17 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-09 | |

| Feb-09 | |

| Feb-09 | |

| Feb-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite