|

|

|

|

|||||

|

|

|

Ball trades at $58.01 per share and has stayed right on track with the overall market, gaining 6.8% over the last six months. At the same time, the S&P 500 has returned 3.7%.

Is there a buying opportunity in Ball, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

We're swiping left on Ball for now. Here are three reasons why we avoid BALL and a stock we'd rather own.

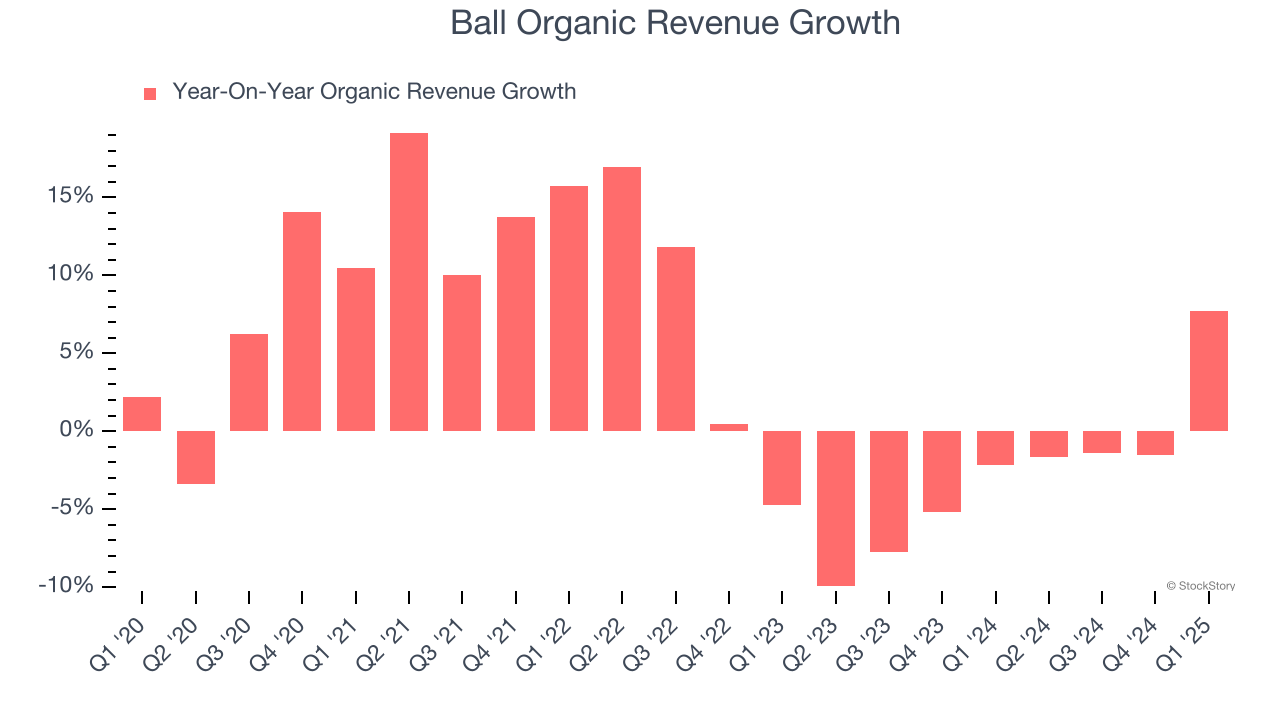

Investors interested in Industrial Packaging companies should track organic revenue in addition to reported revenue. This metric gives visibility into Ball’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Ball’s organic revenue averaged 2.7% year-on-year declines. This performance was underwhelming and implies it may need to improve its products, pricing, or go-to-market strategy. It also suggests Ball might have to lean into acquisitions to grow, which isn’t ideal because M&A can be expensive and risky (integrations often disrupt focus).

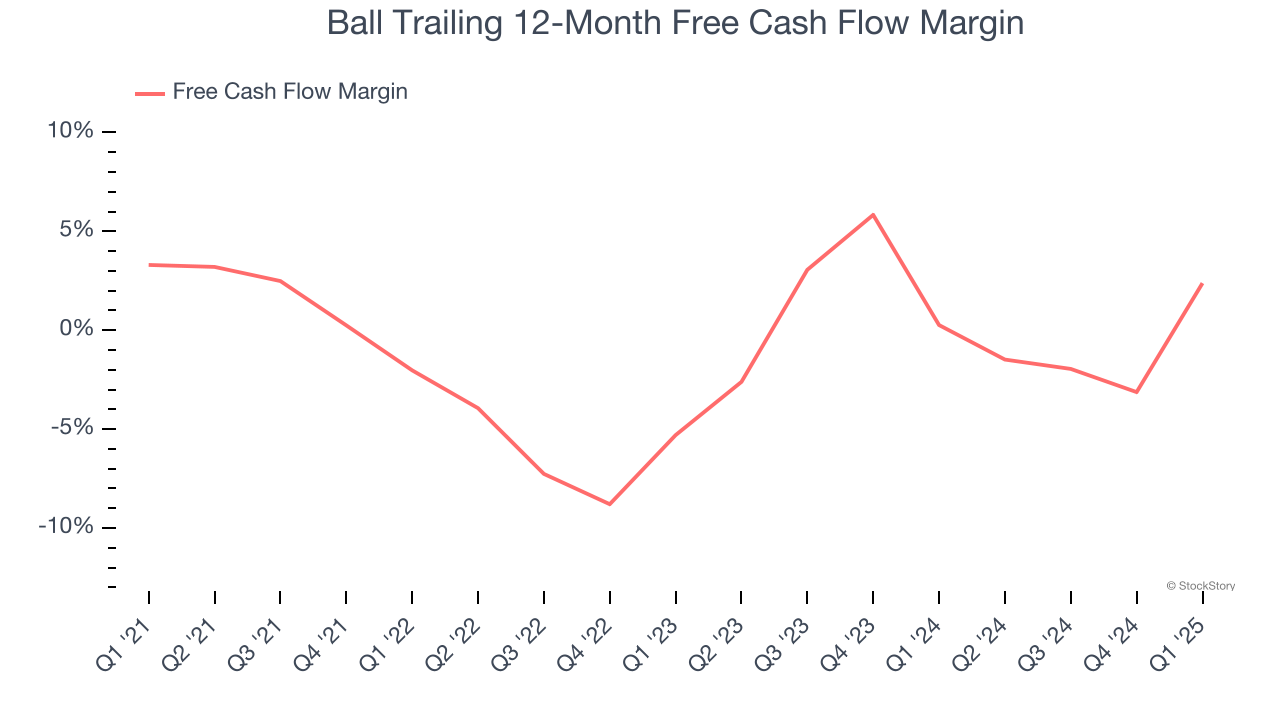

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Ball broke even from a free cash flow perspective over the last five years, giving the company limited opportunities to return capital to shareholders.

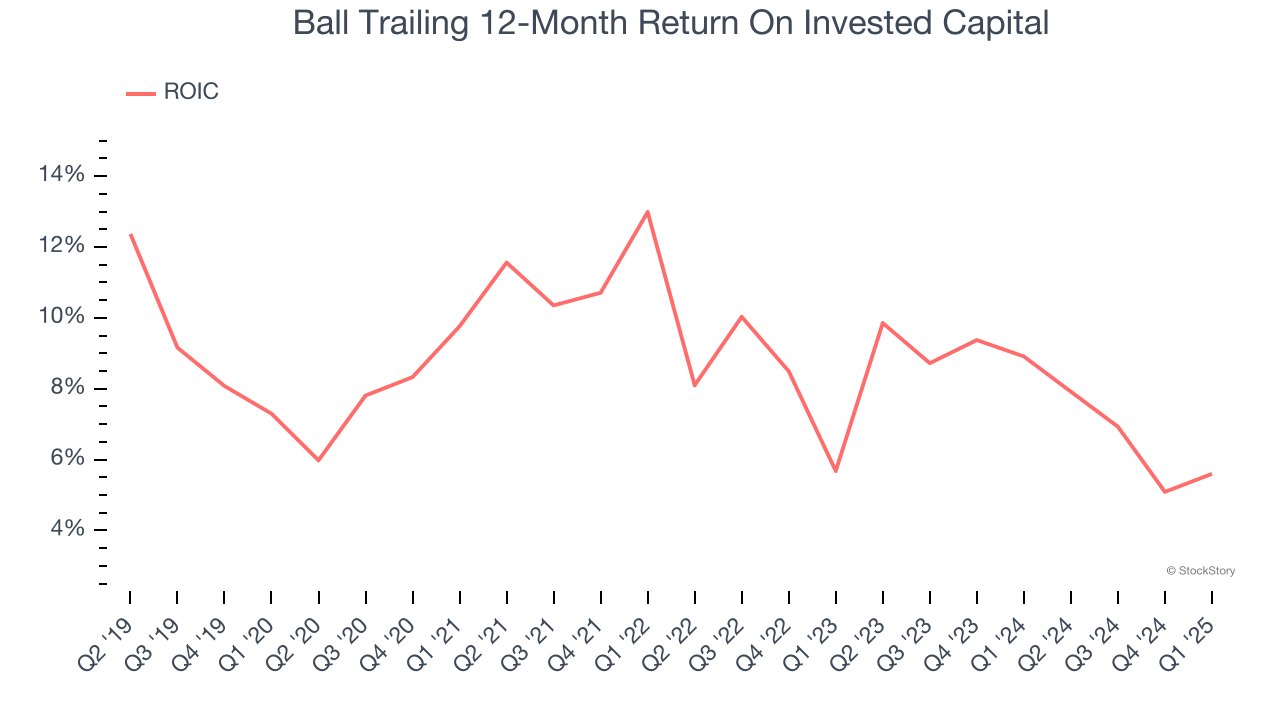

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Ball’s ROIC averaged 4.1 percentage point decreases over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

We cheer for all companies making their customers lives easier, but in the case of Ball, we’ll be cheering from the sidelines. That said, the stock currently trades at 16× forward P/E (or $58.01 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are better stocks to buy right now. We’d recommend looking at one of our top software and edge computing picks.

Trump’s April 2024 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Feb-17 | |

| Feb-12 | |

| Feb-10 | |

| Feb-10 | |

| Feb-09 | |

| Feb-09 | |

| Feb-04 | |

| Feb-04 | |

| Feb-03 | |

| Feb-03 | |

| Feb-03 | |

| Feb-03 | |

| Feb-03 | |

| Feb-03 | |

| Feb-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite