|

|

|

|

|||||

|

|

|

Target Corporation’s TGT store-as-hub model remains a pivotal competitive moat, seamlessly blending the physical and digital shopping experiences to enhance customer convenience. Despite facing macro pressures, Target has leaned heavily on its nearly 1,981 store locations (as of May 3, 2025) to drive both in-store and digital fulfillment. 96% of first-quarter fiscal 2025 sales volume were fulfilled through stores, underscoring the efficacy of this model. The model enables faster delivery, enhanced customer convenience and cost efficiencies that pure-play e-commerce retailers struggle to match.

Same-day services, including Drive Up and same-day delivery through Target Circle 360, are tightly integrated into this store-as-hub network. These offerings have shown robust momentum, with same-day delivery growing more than 35% in the last reported quarter. Furthermore, the average "click to deliver" speed improved nearly 20% year over year, with more than 70% of first-quarter digital orders fulfilled within a single day. This infrastructure actively drives higher engagement and supports the digital ecosystem, including Roundel and Target Plus.

Furthermore, ongoing store remodels and commitment to opening about 20 new stores indicate Target’s belief in this strategy. While competitors may chase similar omnichannel capabilities, Target’s embedded network and operational experience position it to maintain a meaningful advantage in fulfillment speed. Despite recent sales challenges, the store-as-hub model remains integral to Target’s growth playbook, offering flexibility, efficiency and relevance in the current retail landscape.

Walmart Inc. WMT continues to strengthen its store-as-hub model, using its expansive store network to power same-day pickup and delivery. Walmart’s integration of stores with digital fulfillment remains a key competitive advantage, supporting its U.S. e-commerce orders through store-based operations. Walmart’s ongoing investments in automation and last-mile delivery reinforce this strategy, allowing it to compete aggressively on speed and convenience.

Best Buy Co., Inc. BBY also leans heavily on its store-as-hub strategy, utilizing its store fleet to fulfill a significant portion of online orders through same-day pickup and ship-from-store. Best Buy’s stores enable rapid fulfillment, while enhancing operational efficiency. Best Buy’s ability to leverage physical locations as fulfillment hubs strengthens its competitive positioning.

Target stock has risen 10.4% over the past three months compared with the industry’s growth of 0.3%.

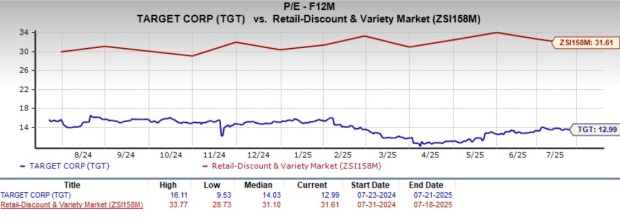

Target’s forward 12-month price-to-earnings ratio of 12.99 reflects a lower valuation compared with the industry’s average of 31.61. TGT carries a Value Score of A.

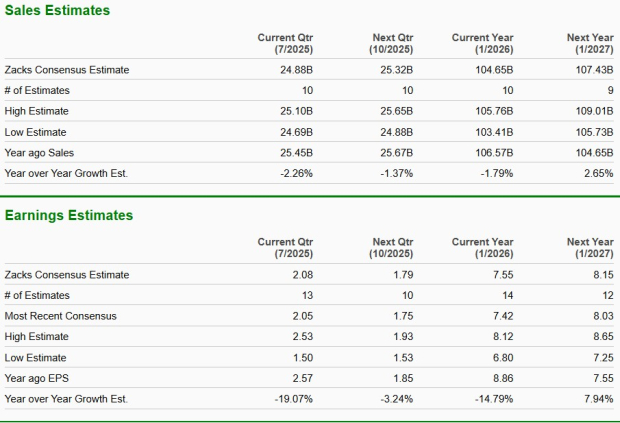

The Zacks Consensus Estimate for Target’s current financial-year sales and earnings per share implies a year-over-year decline of 1.8% and 14.8%, respectively.

Target currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| 6 hours | |

| 8 hours | |

| 14 hours | |

| 15 hours | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-08 | |

| Jun-08 | |

| Jun-08 | |

| Jun-08 | |

| Jun-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite