|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Palantir's revenue is accelerating as it wins more and more large software contracts.

It is working to expand into new industries like nuclear power.

The stock trades at an extreme valuation.

One of the best-performing stocks of the last 12 months is Palantir Technologies (NASDAQ: PLTR). It has gone on an incredible run for shareholders in that period with a 436% gain, adding to its whopping 2,300% return since the beginning of 2023. That is a more than 20x return in just two and a half years, making many shareholders rich in the process. The artificial intelligence (AI) company serves many large organizations like the Department of Defense, and it's seeing accelerating revenue growth and huge customer wins.

Investors are so bullish that Palantir stock recently zoomed past $150 per share, giving it a market cap of nearly $350 billion. Here's my prediction for what comes next for Palantir Technologies.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

The first thing that jumps out about Palantir is the company's accelerating momentum at scale. Last quarter, its revenue grew 39% year over year to $884 million, driven by strong domestic sales. U.S. revenue was up 55%, while U.S. commercial revenue (coming from the private sector) growth accelerated to 71% year over year.

At the same time, Palantir is expanding its profitability. Operating margin was 20% last quarter and 13% over the last 12 months. With strong gross margins, Palantir has a clear path to keep expanding its profit margins as the business scales.

Forward indicators look bright for Palantir as well. Just in the first quarter, it closed 139 deals with customers worth over $1 million, plus an additional 31 deals worth at least $10 million. As the AI operating system for large enterprises, Palantir is proving its worth and seeing huge spending from these customers. The U.S. Department of Defense alone has contracts worth over $1 billion with Palantir, with room to expand over time.

Revenue and earnings should keep growing for Palantir as it shapes up to be one of the biggest software winners of the decade.

Image source: Getty Images.

Using its AI and software analytics, Palantir is aiming to move into more and more industries to help spur innovation. For example, it's working with a start-up called The Nuclear Company to install Palantir software as the operating system for its entire nuclear energy supply chain. The company is aiming to build gigawatt-scale nuclear energy plants in the U.S. to help with rising electricity demands.

Industries like this could end up being large growth drivers for Palantir in the long term. The U.S. government wants the industry to spend hundreds of billions of dollars, if not trillions of dollars, building new nuclear energy facilities. If they are powered by Palantir's AI software -- which could speed up regulatory approvals and save on major cost overruns -- then it could be a huge opportunity for the company.

Overall, Palantir has its hands in a lot of pies, both in the public and private sectors. Organizations are seeing the value of its AI tools, which is why revenue has reached a $3.5 billion annual run rate. Spending on AI software is set to grow for the rest of the decade, meaning that Palantir's market opportunity is expanding. It's not unreasonable to believe the company can reach $10 billion or $20 billion of annual revenue in the future.

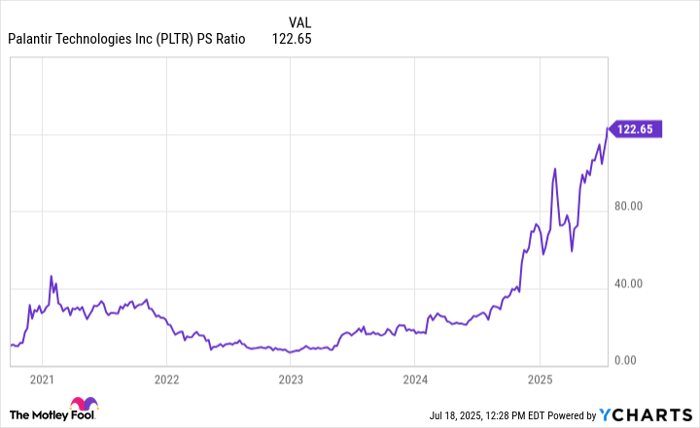

Data by YCharts.

There is a lot to like about Palantir's business. But when it comes to the stock, it may be the most overvalued company in history.

With a market cap of more than $350 billion, its price-to-sales (P/S) ratio is 122.7. To be clear, that is its price-to-sales ratio, not its price-to-earnings (P/E) ratio. Meanwhile, the S&P 500, which many investors are warning is already overvalued, sports a P/S ratio of 3.2. That incredible premium means investors are pricing in huge expectations for growth that will be difficult for even a company like Palantir to deliver.

Even if Palantir grows its revenue to $20 billion over the next decade and achieves a 30% profit margin, that is $6 billion in annual earnings. Its P/E ratio would be nearly 60 based on its current market cap. That 10-year forward P/E ratio of 60 is still well over twice the long-term average of the S&P 500. These are not the conditions for strong long-term returns.

I predict Palantir stock's future does not look like the recent past as the share price butts up against reality over the next decade. It is a great business but one that is extremely overvalued. I would avoid buying Palantir stock at these levels.

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $665,092!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,050,477!*

Now, it’s worth noting Stock Advisor’s total average return is 1,055% — a market-crushing outperformance compared to 180% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of July 21, 2025

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Palantir Technologies. The Motley Fool has a disclosure policy.

| 52 min |

AI Stocks Hit Reset. Will Nvidia, Snowflake, CoreWeave, Salesforce Earnings Decide What's Next?

PLTR

Investor's Business Daily

|

| 2 hours | |

| Feb-22 | |

| Feb-22 | |

| Feb-22 | |

| Feb-22 | |

| Feb-22 | |

| Feb-21 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite