|

|

|

|

|||||

|

|

|

The rise of artificial intelligence (AI) has captivated the attention and capital of investors.

Palantir stock has gained more than 2,800% since the start of 2023 thanks to the irreplaceability of its two foundational operating segments, Gotham and Foundry.

However, an assortment of macro and company-specific headwinds should eventually bring its near-parabolic ascent to a grinding halt.

For the better part of the past 30 years, investors have had a game-changing technology or next-big-thing trend to captivate their attention and wallets. Some of these hyped advancements include the internet, genome decoding, blockchain technology, and the metaverse. But not since the proliferation of the internet have investors demonstrated the level of enthusiasm they have for the rise of artificial intelligence (AI).

In Sizing the Prize, the analysts at PwC pegged the addressable opportunity for AI, inclusive of productivity improvements and consumption-side effects, at $15.7 trillion globally by 2030. It's mammoth figures like this that have fueled a near-parabolic climb in Wall Street's AI darling, Palantir Technologies (NASDAQ: PLTR).

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Image source: Getty Images.

As of this writing on Aug. 10, Palantir has ascended the ladder to become the 19th largest publicly traded company in the U.S., with a market cap topping $443 billion. To put its more than 2,800% gain since the start of 2023 into context, it's now larger than:

Another 2% upside and Palantir will eclipse ExxonMobil, which is the largest publicly traded energy company in the United States.

To say that Palantir's rally has been impressive would understate just how far it's come in such a short period. But it also highlights how perilous Palantir's ascent just might be.

Palantir Technologies transitioning from just another tech stock to one of the sector's most important businesses in two years wasn't an accident. It's a reflection of bringing well-defined and sustainable competitive advantages to the table.

Palantir's premier operating segment is Gotham. This AI- and machine learning (ML)-powered software-as-a-service (SaaS) platform is used by federal governments to collect and analyze data, as well as plan and oversee military missions. Typically, Gotham secures multiyear contracts from the U.S. government, which provides highly predictable operating cash flow year after year.

The other core operating segment for Palantir is Foundry. This AI- and ML-inspired SaaS platform helps businesses make sense of their data in order to streamline/automate their operations. This is a newer segment, relative to Gotham, and is therefore capable of delivering a juicier growth rate.

Neither Gotham nor Foundry has large-scale competitors angling for their clients. Businesses that are deemed irreplaceable are usually bestowed with a healthy premium on Wall Street.

Palantir has also helped its cause by becoming profitable on a recurring basis well ahead of consensus expectations. Alex Karp's company has consistently blown past even the loftiest growth and profit projections.

Image source: Getty Images.

While there's no denying Palantir is worthy of a premium valuation given its sustainable competitive edges, there's a rational limit to what this premium entails. Put bluntly, Palantir has all the hallmarks of a house of cards that will, eventually, collapse.

Make no mistake about the following argument: I'm not attempting to precisely call a top in Palantir stock. If Wall Street has taught me anything about investing over the past 27 years, it's that stocks can stay irrational longer than short-sellers can remain solvent. But at some point, in what I'd presume is the not-too-distant future, this near-parabolic ascent will end in an unceremonious fashion.

First, Palantir will have to overcome macro pressures. For instance, the S&P 500's (SNPINDEX: ^GSPC) Shiller price-to-earnings (P/E) ratio recently hit its third priciest multiple when backtested 154 years. History tells us that when stock valuations become this extended, it's simply a matter of time before Wall Street's major indexes endure a bear market decline. If history were to follow suit, some of Wall Street's biggest winners (ahem, Palantir) would likely be hit hardest during a marketwide downturn.

Along these same lines, there hasn't been a game-changing technological advance or innovation that's avoided a bubble-bursting event in more than three decades.

Including the internet, every hyped trend has eventually fallen off, with investors consistently overestimating the utility or adoption rates of game-changing technologies. Even though businesses are spending big bucks on AI infrastructure, early returns suggest most have yet to optimize their AI solutions or generate a positive return on their investments. If the AI bubble bursts, Palantir would have a bullseye on its proverbial back.

But let's not beat around the bush: Palantir's valuation is completely unjustifiable.

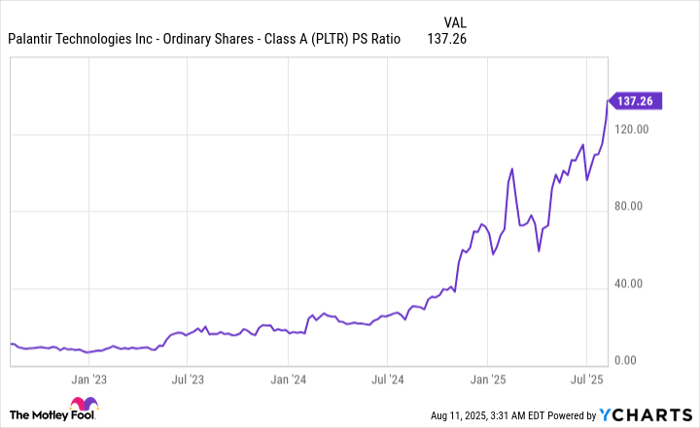

PLTR PS Ratio data by YCharts. PS Ratio= price-to-sales ratio.

Before the S&P 500 and Nasdaq Composite lost 49% and 78% of their respective value during the bursting of the dot-com bubble, Wall Street's leading businesses peaked at price-to-sales (P/S) ratios ranging from 31 to 43. Perhaps not coincidentally, AI powerhouse Nvidia topped out at a P/S ratio of 42 last summer. The point being that P/S ratios of 30 to 40 have historically served as ceilings for megacap companies.

As of the closing bell on Aug. 8, Palantir's P/S ratio was 137! That's not 37 with an accidental typo. That's 137 times trailing-12-month sales for the 19th-largest domestic public company. There isn't a megacap company that's come even remotely close to justifying or sustaining such a premium valuation throughout history.

Even if Palantir's stock went sideway for the next four years, it would be still be valued at 116 times forecast earnings per share and trade at 38 times projected sales, which again is right in line with where previous bubbles popped.

A final concern that can't be swept under the rug is the lack of clarity on defense spending for Gotham beyond 2028. While President Trump's administration has made defense spending and internal AI innovation a priority, midterm elections and Trump's departure from the White House in January 2029 can change everything.

Palantir is truly priced for perfection. Unfortunately, no situation is ever perfect.

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $660,783!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,122,682!*

Now, it’s worth noting Stock Advisor’s total average return is 1,069% — a market-crushing outperformance compared to 184% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 13, 2025

Sean Williams has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Costco Wholesale, Home Depot, Nvidia, and Palantir Technologies. The Motley Fool recommends Johnson & Johnson. The Motley Fool has a disclosure policy.

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite