|

|

|

|

|||||

|

|

|

Allegro MicroSystems has been on fire lately. In the past six months alone, the company’s stock price has rocketed 40.4%, reaching $35.02 per share. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Allegro MicroSystems, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

We’re glad investors have benefited from the price increase, but we're swiping left on Allegro MicroSystems for now. Here are three reasons why you should be careful with ALGM and a stock we'd rather own.

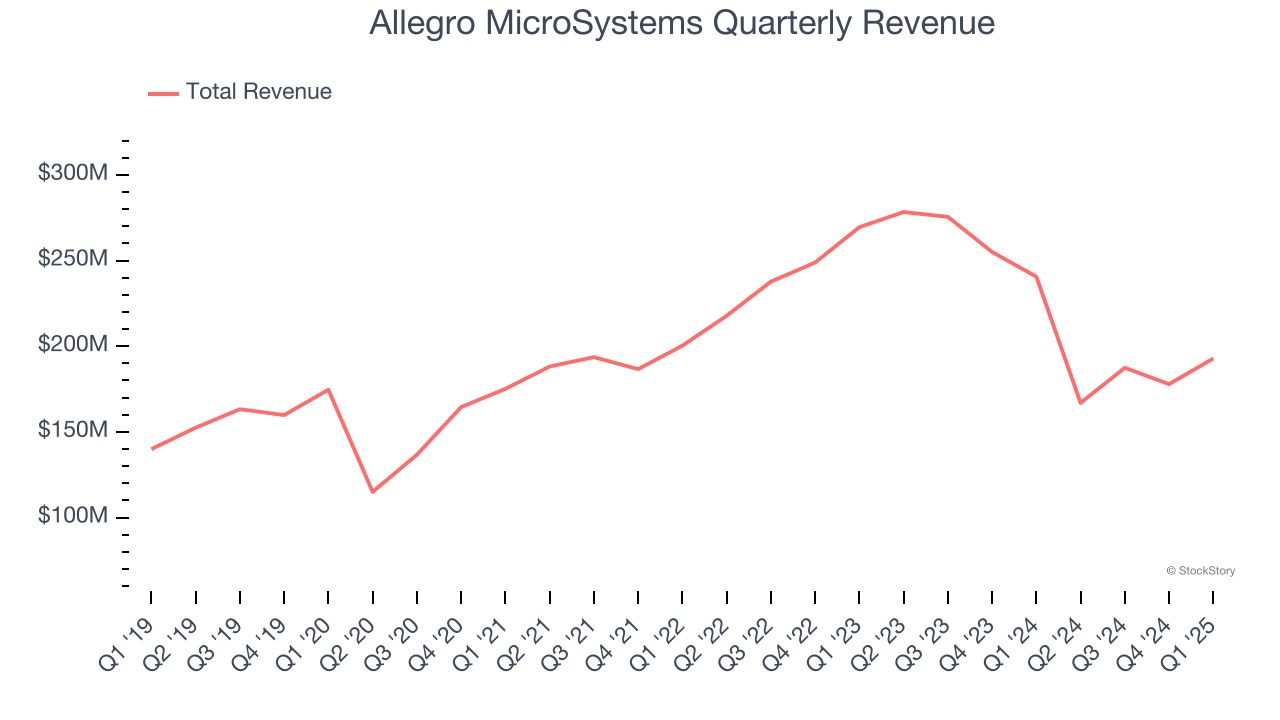

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Allegro MicroSystems’s 2.2% annualized revenue growth over the last five years was sluggish. This was below our standards. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

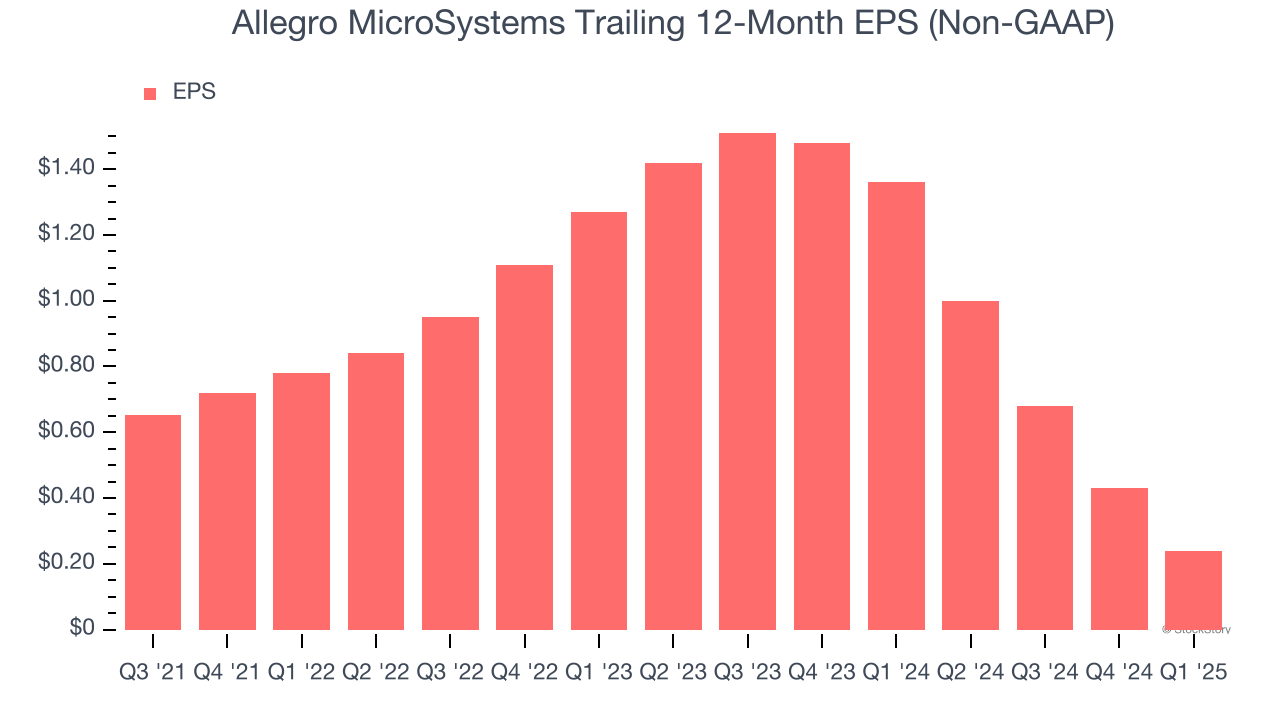

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Allegro MicroSystems’s full-year EPS dropped 86.1%, or 16.8% annually, over the last four years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Allegro MicroSystems’s low margin of safety could leave its stock price susceptible to large downswings.

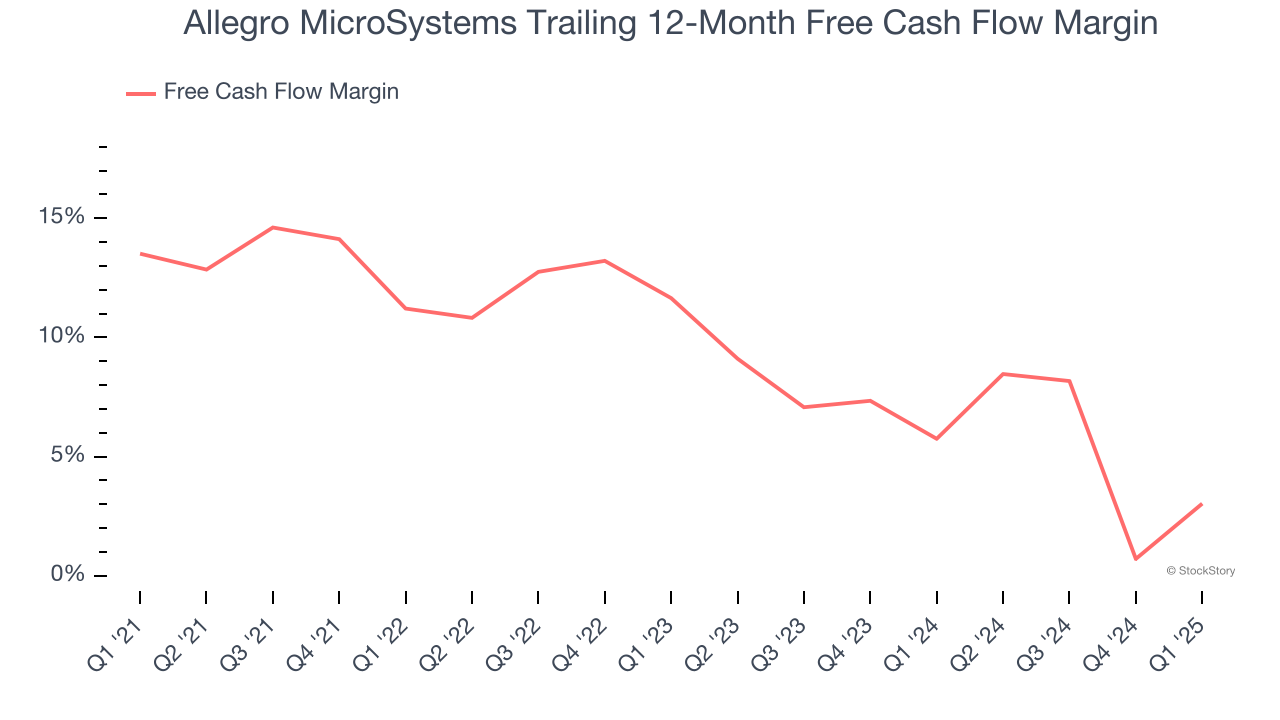

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Allegro MicroSystems’s margin dropped by 10.5 percentage points over the last five years. This along with its unexciting margin put the company in a tough spot, and shareholders are likely hoping it can reverse course. If the trend continues, it could signal it’s becoming a more capital-intensive business. Allegro MicroSystems’s free cash flow margin for the trailing 12 months was 3%.

We cheer for all companies solving complex technology issues, but in the case of Allegro MicroSystems, we’ll be cheering from the sidelines. After the recent surge, the stock trades at 71.8× forward P/E (or $35.02 per share). This multiple tells us a lot of good news is priced in - you can find more timely opportunities elsewhere. We’d recommend looking at an all-weather company that owns household favorite Taco Bell.

When Trump unveiled his aggressive tariff plan in April 2024, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| May-13 | |

| May-13 | |

| May-07 | |

| May-07 |

Allegro MicroSystems Stock Dips Despite Beat-And-Raise Earnings Report

ALGM -6.70%

Investor's Business Daily

|

| May-07 | |

| May-05 | |

| Apr-30 |

Allegro MicroSystems, IBD Stock Of The Day, Surges Ahead Of Earnings

ALGM +10.05%

Investor's Business Daily

|

| Apr-24 | |

| Apr-16 | |

| Feb-23 | |

| Feb-22 | |

| Feb-20 | |

| Feb-19 | |

| Feb-18 | |

| Feb-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite