|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

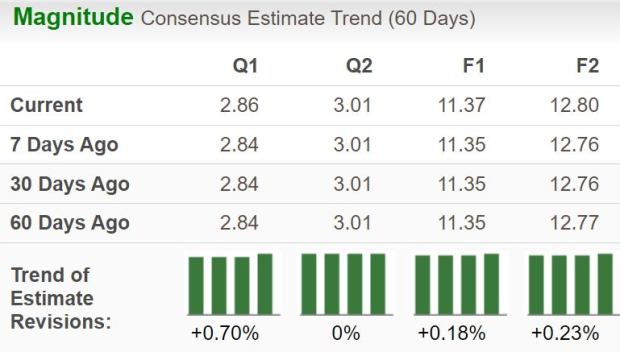

Visa Inc. V is set to report its third-quarter fiscal 2025 results on July 29, 2025, after market close. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings is currently pegged at $2.86 per shareon revenues of $9.87 billion.

The estimate for fiscal third-quarter earnings has been revised upward by 2 cents over the past 60 days. The bottom-line projection indicates a year-over-year increase of 18.2%. The Zacks Consensus Estimate for quarterly revenues suggests year-over-year growth of 10.9%.

For fiscal 2025, the Zacks Consensus Estimate for Visa’s revenues is pegged at $39.63 billion, implying a rise of 10.3% year over year. The consensus mark for EPS is pegged at $11.37, suggesting a jump of around 13.1% on a year-over-year basis.

The payments juggernaut has a robust history of surpassing earnings estimates. It beat estimates in each of the last four quarters, with the average being 3%. This is depicted in the graph below:

Visa Inc. price-eps-surprise | Visa Inc. Quote

Our proven model predicts a likely earnings beat for Visa this time around as well. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) increases the odds of an earnings beat. That’s precisely the case here.

Visa has an Earnings ESP of +0.39% and a Zacks Rank #2. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate suggests a 3.6% increase in total Gross Dollar Volume from the previous year, while our model predicts 4.6% growth. The growing adoption and popularity of digital payment methods are likely to contribute positively to Visa's overall fiscal third quarter results.

As the company draws revenues as a set percentage of total transaction value every time a customer makes payments with a debit/credit card, higher spending means more revenues in the form of transaction processing fees. The Zacks Consensus Estimate for fiscal third-quarter total processed transactions indicates 8.7% year-over-year growth, whereas our model predicts a 9.6% increase.

The consensus mark for total payment volumes indicates a 7.7% year-over-year increase. We expect the metric for U.S. operations alone to jump 6.3% year over year. Similarly, our model predicts 15% year-over-year growth in Latin America and CEMEA, each.

The Zacks Consensus Estimate for data processing revenues indicates 12.5% growth in the fiscal third quarter from the year-ago level of $4.5 billion, while our estimate suggests an 11.8% increase. Similarly, the consensus mark for service revenues suggests 8.2% year-over-year growth, whereas we expect the metric to grow by 7.4%.

Furthermore, the consensus estimate for international transaction revenues indicates 12.8% growth from a year ago, whereas our model predicts a 12.2% increase. Continuous growth in cross-border volumes is expected to have supported the metric.

The factors stated above are expected to have positioned Visa for strong year-over-year growth and an earnings beat in the fiscal third quarter. However, rising expenses and client incentives (a contra-revenue item) are likely to have partially offset the positive impact of higher volumes.

We expect adjusted total operating expenses for the quarter under review to increase more than 10% year over year due to increased Personnel, Marketing, Professional Fees and Network and Processing expenses. Also, both the Zacks Consensus Estimate and our model estimate for client incentives suggest that the metric will be well above $4 billion in the fiscal third quarter.

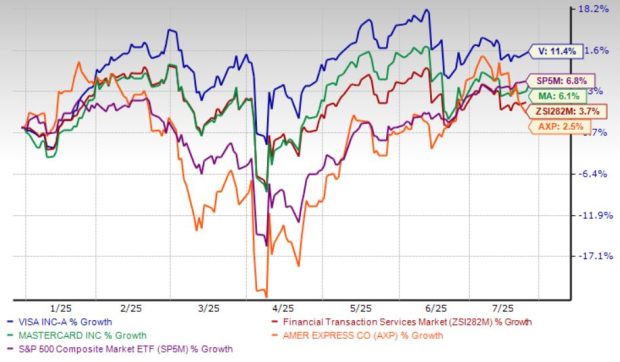

Visa's stock has gained 11.4% in the year-to-date period. It outperformed the industry and the S&P 500’s rise of 3.7% and 6.8%, respectively. In comparison, its peers like Mastercard Incorporated MA and American Express Company AXP have increased 6.1% and 2.5%, respectively, during this time.

Now, let’s look at the value Visa offers investors at current levels.

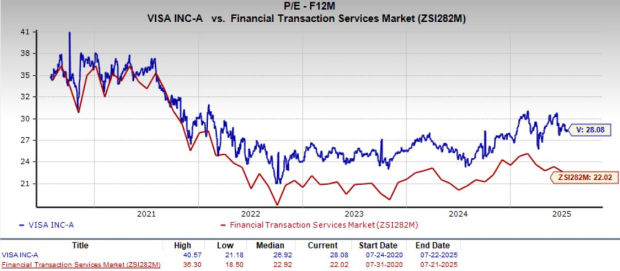

The company’s valuation looks somewhat stretched compared with the industry average. Currently, Visa is trading at 28.08X forward 12-month earnings, above its five-year median of 26.92X and the industry’s average of 22.02X.

In comparison, Mastercard is even less attractively valued, trading at 31.87X forward 12-month earnings. American Express, on the other hand, is trading at 18.54X, offering a better value at the moment.

Visa remains a compelling buy ahead of fiscal third quarter earnings, backed by resilient consumer spending, robust travel demand and a surge in payment volumes. Processed transactions continue to grow, while payments volume rises, driven by strength in Latin America, CEMEA and other regions. With a $647.5 billion market cap and global dominance, Visa is well-positioned to capture long-term growth in emerging markets and new digital payments trends. Its business model is often praised for being capital-light and relatively risk-free, unlike American Express.

Visa is pushing hard into AI-powered commerce and stablecoin settlement, aiming to enhance cross-border efficiency and security. Strategic fintech partnerships and stablecoin pilots position Visa as a leader in the future of digital finance. Peers like Mastercard are also focusing on stablecoin innovation to improve the speed and cost-efficiency. Financially, Visa is rock solid. Rising cash flow, high return on capital, and shareholder value-boosting efforts are well-liked by investors. With strong momentum and digital innovation, Visa remains a top-tier stock for investors now.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite