|

|

|

|

|||||

|

|

|

Ford Motor recently announced stellar sales numbers for the second quarter.

Tariffs will likely hurt its financials although the automaker should be able to work through it.

Higher sales and higher costs may offset each other, potentially limiting Ford's near-term upside.

The automotive industry has been reeling for months following the Trump administration's announced tariffs, which have threatened to increase costs, likely leading to higher prices for consumers.

Ford Motor Company (NYSE: F) approached the situation aggressively, marketing to its American roots and offering vehicle buyers employee-level pricing for a three-month period. It worked. Ford recently announced fantastic second-quarter vehicle sales, including an estimated 1.8-percentage-point gain in market share. Now, the company has followed it up with a new promotion aimed at lowering up-front costs for buyers.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

With Ford building sales momentum, it's fair to ask where the stock might be in three years. I dove into the numbers to find out. Here is what you need to know.

Image source: Getty Images.

Despite Ford's standing as a leading American vehicle brand, it is a global business, both in supply chain and in sales. The tricky part is figuring out just how tariffs will affect the company, which is remarkably difficult due to the Trump Administration's inconsistent messaging on policy.

As of first-quarter earnings, management was anticipating a net headwind of $1.5 billion to Ford's 2025 earnings before interest and taxes (EBIT). It appears that part of Ford's strategy has been to lean into the tariff headwinds as an opportunity to leverage its American identity with U.S. consumers. Ford extended employee-level pricing to buyers as part of its "From America, For America" campaign.

The promotion, which ran from early April to early July, was a winner. Ford's vehicle sales skyrocketed by 14.2% in Q2 2025, including:

Automotive manufacturers have high fixed costs associated with operating factories. Investors will need to see management's updated financial outlook when Ford releases its full Q2 earnings on July 30. Still, it would prove a savvy move by Ford if the company could grow its sales volume enough to offset tariff-related costs, while boosting market share and giving the Ford brand some momentum in the process.

Tariffs, in some shape or form, are looming. Analysts have already baked a sizable hit to earnings into Ford's 2025 estimates. The consensus on Wall Street is that earnings will drop from $1.84 per share last year to an estimated $1.12 this year.

Beyond the effect on earnings, the important takeaway is that Ford can remain profitable. While investors must read between the lines until Ford releases its Q2 earnings, management probably wouldn't follow its Q2 promotion with another campaign if the company were losing more money selling all those additional vehicles.

The dividend, yielding over 5.3%, is still just 54% of 2025 earnings estimates, and management reiterated Ford's balance sheet strength in Q1, which ended with $27 billion in cash and $45 billion in total liquidity. Ford should have ample financial resources to weather the tariff uncertainty, and its decision to pursue market share in this situation underscores that confidence.

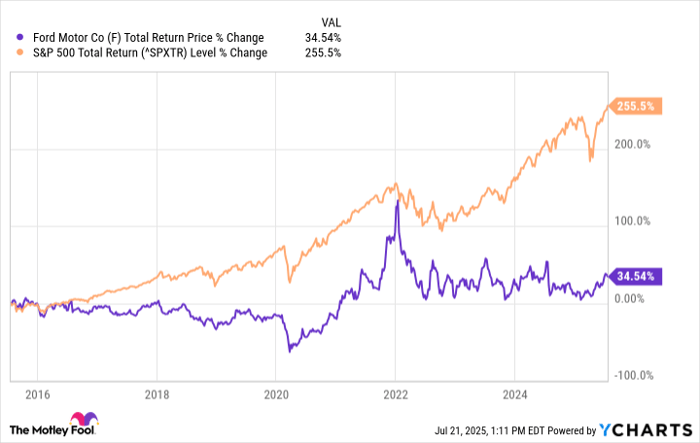

It's worth noting that the auto industry is highly competitive, and companies must continually invest in updating, maintaining, and upgrading expensive factories. Ford is a significant industry player, yet its stock has still badly lagged the broader stock market over time.

Therefore, even if Ford successfully navigates the tariff headwinds, it's not guaranteed to yield great investment results. Currently, Ford's free cash flow yield is 20%, on par with its average over the past decade.

F Total Return Price data by YCharts.

It's tough to envision the stock fetching a higher valuation while tariffs continue to weigh on the business. The hope is that Ford sells more vehicles at lower margins (due to tariffs) to the point that free cash flow grows. Upcoming Q2 earnings will give investors a fresh set of expectations regarding how tariffs will affect Ford's profits. Keep in mind that Ford's current valuation reflects pre-tariff cash flows.

I suspect that Ford will be working back to 2024 profits over the next few years. When it all shakes out, much of the tariff-related costs and higher sales volume could somewhat offset each other. In that scenario, the stock price may not change much. Ford's 5.3% dividend could represent a significant portion of the stock's investment returns.

So, for now, it appears that Ford stock has limited upside over the next three years. Of course, that could change as the tariff situation evolves.

Before you buy stock in Ford Motor Company, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Ford Motor Company wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $634,627!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,046,799!*

Now, it’s worth noting Stock Advisor’s total average return is 1,037% — a market-crushing outperformance compared to 182% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of July 21, 2025

Justin Pope has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

| 4 hours | |

| 6 hours |

Magna Stock Revs Nearly 20% In Massive Volume On Earnings; Gets Rating Upgrade

F

Investor's Business Daily

|

| 6 hours | |

| 10 hours | |

| 11 hours | |

| 12 hours | |

| 13 hours | |

| 20 hours | |

| 20 hours | |

| 21 hours | |

| 22 hours | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite