|

|

|

|

|||||

|

|

|

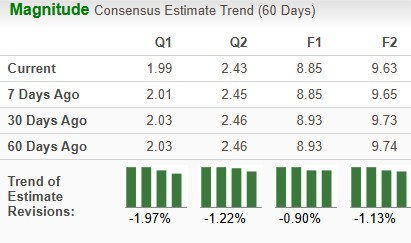

Merck MRK will report its second-quarter 2025 earnings on July 29, before market open. The Zacks Consensus Estimate for second-quarter sales and earnings is pegged at $15.77 billion and $1.99 per share, respectively. Earnings estimates for 2025 have declined from $8.93 to $8.85 per share over the past 30 days.

The healthcare bellwether’s performance has been solid, with the company exceeding earnings expectations in each of the trailing four quarters. It delivered a four-quarter earnings surprise of 3.82%, on average. In the last reported quarter, the company delivered an earnings surprise of 3.26%, as seen in the chart below.

Merck has an Earnings ESP of 0.00% and a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Per our proven model, companies with the combination of a positive Earnings ESP and a Zacks Rank #1, #2 (Buy) or #3 have a good chance of delivering an earnings beat. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Merck’s top-line growth in the second quarter is likely to have been driven by higher sales of its blockbuster cancer drug Keytruda, as in several previous quarters, driven by additional indications and patient demand.

In oncology drugs, Keytruda sales are likely to have been driven by rapid uptake across earlier-stage indications globally, particularly early-stage non-small cell lung cancer. Continued strong momentum in metastatic indications is also likely to have boosted sales growth. The Zacks Consensus Estimate for Keytruda’s sales is $7.90 billion, while our estimate is $7.87 billion.

Higher alliance revenues from Lynparza, driven by increased demand, may have boosted oncology sales. Please note that Merck markets Lynparza in partnership with AstraZeneca AZN. Merck has a profit-sharing deal with AstraZeneca to co-market Lynparza and Koselugo.

Alliance revenues from Lenvima may have also boosted oncology sales.

Sales of the new drug Welireg are likely to have benefited from the increased uptake for the additional indication of previously treated advanced renal cell carcinoma in the United States. Welireg was approved for the third indication, two rare adrenal tumors, advanced pheochromocytoma and paraganglioma, in May 2025, which may have contributed to sales in the second quarter.

With regard to the HPV vaccine, Gardasil, ex-U.S. sales are expected to have been hurt by lower demand in China due to a significant decline in demand and elevated channel inventory. Sales are likely to have increased in other markets like the United States and Japan due to higher demand. The Zacks Consensus Estimate for Gardasil is $1.3 billion, while our estimate is $1.43 billion.

In the hospital specialty portfolio, generic competition in certain ex-U.S. markets is likely to have hurt sales of neuromuscular blockade medicine — Bridion injection. However, higher demand and pricing are expected to have benefited U.S. sales. The Zacks Consensus Estimate for Bridion is $440.0 million, while our estimate is $441.9 million.

Lower demand in the United States and generic competition in certain international markets, mainly Europe and Asia Pacific, are likely to have hurt sales of the diabetes franchise (Januvia/Janumet). In the first quarter, Januvia/Janumet sales benefited from some pricing adjustments in the United States which are unlikely to have been a tailwind in the second quarter.

New pulmonary arterial hypertension (PAH) drug Winrevair is likely to have contributed to sales growth with most sales coming from the U.S. market as the company is steadily adding new patients. Another new vaccine, Capvaxive, is also off to an encouraging start in the United States, gaining from rising demand from the retail pharmacy channel. Capvaxive was approved in the European Union toward the end of March. It is likely to have contributed to sales in the second quarter.

The Zacks Consensus Estimate for Merck’s Pharmaceutical unit is $13.85 billion, while our estimate is $13.87 billion.

In the Animal Health franchise, growth in both companion animal and livestock products is likely to have contributed to sales. Sales are also likely to have benefited from the inclusion of sales from the newly acquired Elanco’s aqua portfolio. The Zacks Consensus Estimate, as well as our estimate for the Animal Health unit, is $1.55 billion.

Nonetheless, a single quarter’s results are not important for long-term investors. Let's delve deeper to understand whether to buy, sell or hold Merck stock.

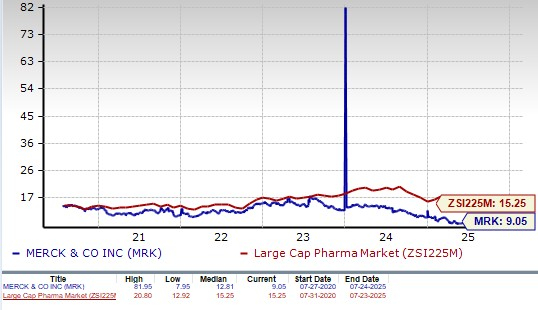

Merck’s shares have lost 13.9% so far this year against an increase of 3.3% for the industry. The stock has also underperformed the sector and the S&P 500, as seen in the chart below.

From a valuation standpoint, Merck appears attractive relative to the industry. Going by the price/earnings ratio, the company’s shares currently trade at 9.05 forward earnings, lower than 15.25 for the industry as well as its 5-year mean of 12.81.

Merck boasts more than six blockbuster drugs in its portfolio, with Keytruda being the key top-line driver. Keytruda, approved for several types of cancer, alone accounts for around 50% of the company’s pharmaceutical sales. Merck has also been making meaningful regulatory and clinical progress across areas like oncology (mainly Keytruda), vaccines and infectious diseases while executing strategic business moves.

In early July, Merck announced adefinitive agreement to acquire Verona Pharma VRNA for approximately $10 billion. The deal will add Verona’s Ohtuvayre, approved for the maintenance treatment of chronic obstructive pulmonary disease (COPD). This addition will strengthen Merck’s cardio-pulmonary pipeline and portfolio as the drug’s differentiated profile provides a significant edge over its competitors.

Though Keytruda may be Merck’s biggest strength and a solid reason to own the stock, it can also be argued that the company is excessively dependent on the drug, and it should look for ways to diversify its product lineup.

There are rising concerns about the firm’s ability to grow its non-oncology business ahead of the upcoming loss of exclusivity of Keytruda in 2028.

Also, competitive pressure might increase for Keytruda in the near future. Summit Therapeutics SMMT is developing ivonescimab, a dual PD-1 and VEGF inhibitor, which has outperformed Keytruda in a late-stage study. Summit believes iivonescimab has the potential to replace Keytruda as the next standard of care across multiple NSCLC settings.

The company’s second-largest product, Gardasil, is also seeing grim sales in China. Merck is also seeing weakness in the diabetes franchise and the generic erosion of some drugs.

Merck’s problems are numerous at present, including persistent challenges for Gardasil in China, potential competition for Keytruda, and rising competitive and generic pressure on some of its drugs. All these factors have raised doubts about Merck’s ability to navigate the Keytruda loss-of-exclusivity period successfully. Consistently declining estimates and price depreciation reflect analysts’ pessimistic outlook for the stock.

However, Merck has one of the world’s best-selling drugs in its portfolio, generating billions of dollars in revenues. Though Keytruda will lose patent exclusivity in 2028, its sales are expected to remain strong until then.

No matter how the second-quarter results play out, we suggest that investors with a long-term horizon stay invested in the stock. However, short-term investors may consider selling MRK stock due to numerous near-term challenges.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite