|

|

|

|

|||||

|

|

|

Krispy Kreme offers substantial upside if management can stabilize sales and reduce debt.

Lululemon's premium brand positioning in the sports apparel market is significantly undervalued.

Even with the stock market hitting new highs, there are plenty of industries with beaten-down stocks that could benefit from an improving economy over the next five years.

Krispy Kreme (NASDAQ: DNUT) stock is down 67% over the past year due to weak financial results, but the stock could soar if management's moves to improve profitability pay off.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Lululemon Athletica (NASDAQ: LULU) stock is trading 57% off its recent highs over slowing growth and concerns about competition, but its recent financial results indicate that this brand is in a much stronger position than the market is giving it credit for.

Let's dive deeper into why these stocks are underperforming, and why they could at least double from here.

Image source: Getty Images.

Shares of Krispy Kreme haven't looked so crispy lately. The stock nosedived earlier this year after delivering disappointing revenue and earnings results. Making matters worse was the announcement that the company would suspend paying dividends to shareholders. But this just reflects the greater problem the company must solve to pay down its debt and shore up profitability.

Krispy Kreme reported a loss of $33 million in the first quarter on $375 million of revenue, and revenue was down 15% over the year-ago quarter. It has restructured the leadership, and one of the initiatives is expanding the number of locations where doughnuts can be purchased. Global points of access grew 21% year over year in Q1 to 17,982, and management is aiming to reach 100,000 purchase locations in the future.

While opening up more ways for customers to buy doughnuts can help strengthen sales, management is also focused on growing cash flow and paying down debt. The business is saddled with nearly $1 billion in debt and just $18.7 million in cash on its balance sheet. However, the business generated $42 million in cash from operations on a trailing 12-month basis, giving management resources to reduce debt.

To strengthen sales, management is reducing reliance on discounting, being more diligent with marketing expenses, and focusing on higher-value options that drive higher margins. On the latter, it is looking to partner with grocery stores and mass retailers like Costco and Walmart's Sam's Club to sell large-volume doughnut packs. The high-volume sales at these locations could generate higher turnover and margins for the company to boost cash flow.

Analysts expect Krispy Kreme's annual revenue to reach $2.7 billion by 2029. If the stock trades at a conservative price-to-sales (P/S) multiple of 0.50, that would translate to a 2.5x return from the current $3.13 share price. A sales multiple of 1 would translate to a $16 share price, or 5x return.

Krispy Kreme is not a pretty-looking situation, but you have to be willing to buy stocks that no one wants to own to land those elusive multibaggers. There is execution risk here, as there is for any turnaround situation. But if current leadership can stabilize sales and reduce debt, this is a promising turnaround play for a high return in the next four years.

Lululemon stock delivered market-beating returns over the last 15 years, as its brand emerged in the mainstream with the leaders in a historically growing industry. Some investors might see Lululemon as being past its prime, but its trailing 12-month revenue of $10.7 billion is still a very small share of the athletic apparel industry. It's got a lot of growth potential that isn't reflected in the stock price.

A number of new competitors have emerged over the past decade. Apparel is one of the most competitive industries out there, but Lululemon was still growing revenue at over 20% annually just a few years ago. A crowded market didn't prevent Lululemon from taking on industry leaders like Nike and Adidas to get to where it is today. The only thing that has changed over the past few years is the economic environment, which has weighed on sales across the industry.

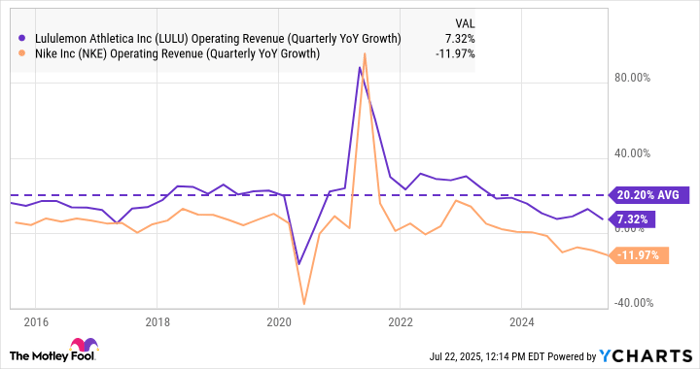

The economy has been through multiple headwinds over the past five years with the pandemic, rising inflation, and elevated interest rates, which have exasperated people's appetite for spending on non-essential items like new clothes. This is pressuring Nike more than Lululemon. Lululemon's revenue grew 7% year over year last quarter, while Nike posted a decline.

Lululemon's sales have consistently outperformed the industry leader over the last 10 years. Wall Street doesn't give the company enough credit for this.

Data by YCharts.

Lululemon's brand strength is evident in its gross margin, which came in at 58.3% in fiscal Q1 2025, up from 57.7% in fiscal Q1 2024, and slightly higher than 57.5% in fiscal Q1 2024. In a stronger consumer spending environment, Lululemon's premium brand positioning is capable of delivering stronger growth.

Lululemon's above-average margins and financial strength should allow it to weather sluggish sales trends, as well as any obstacles that tariffs on imported goods might present in the near term. Lululemon has $1.3 billion of cash and no debt on its balance sheet.

The stock is trading at just 15 times this year's consensus earnings estimate, implying that analysts expect Lululemon to continue reporting a healthy profit. This is a bargain for a company that is still expanding into new categories, like footwear, and that has a lot of room to grow internationally over the long term. A combination of earnings growth and a higher price-to-earnings multiple could at least double the stock by 2030.

Before you buy stock in Krispy Kreme, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Krispy Kreme wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $636,774!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,064,942!*

Now, it’s worth noting Stock Advisor’s total average return is 1,040% — a market-crushing outperformance compared to 182% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of July 21, 2025

John Ballard has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Costco Wholesale, Lululemon Athletica Inc., Nike, and Walmart. The Motley Fool has a disclosure policy.

| 4 hours | |

| 9 hours | |

| Feb-15 |

Companies Are Replacing CEOs in Record Numbersand Theyre Getting Younger

LULU

The Wall Street Journal

|

| Feb-15 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite