|

|

|

|

|||||

|

|

|

Berkshire Hathaway (BRK.B) is expected to witness an improvement in its top line but a decline in its bottom line when it reports second-quarter 2025 results.

The Zacks Consensus Estimate for BRK.B’s second-quarter revenues is pegged at $98.5 billion, indicating a 5.2% increase from the year-ago reported figure.

The consensus estimate for earnings is pegged at $5.24 per share. The Zacks Consensus Estimate for BRK.B’s second-quarter earnings witnessed no movement in the past 30 days. The estimate suggests a year-over-year decrease of 2.6%.

Berkshire Hathaway’s earnings beat the Zacks Consensus Estimates in two of the trailing four quarters and missed in the remaining two, the average surprise being 13.39%.

Our proven model does not conclusively predict an earnings beat for Berkshire this time around. This is because a stock needs to have the right combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold), which increases the chances of an earnings beat. This is not the case, as you can see below.

You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Earnings ESP: BRK.B has an Earnings ESP of 0.00%. This is because both the Most Accurate Estimate and the Zacks Consensus Estimate are pegged at $5.24.

Berkshire Hathaway Inc. price-eps-surprise | Berkshire Hathaway Inc. Quote

Zacks Rank: BRK.B currently has a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

Berkshire Hathaway’s insurance operations are likely to have benefited from better pricing, solid retention rates, increased average premiums per auto policy, broader market exposure and positive reserve developments. A not-so-active catastrophe environment is likely to have aided underwriting profitability in the to-be-reported quarter.

Continued expansion in the insurance segment is also expected to have driven growth in the company’s float.

GEICO, Berkshire Hathaway’s private passenger auto insurance business, is likely to have benefited from an increase in average premiums per policy, lower claims frequency, and enhanced operating efficiencies.

Investment income is also expected to have improved, supported by higher yields and an expanded investment asset base.

BNSF, the company’s railroad subsidiary, may have faced headwinds from an unfavorable business mix and reduced fuel surcharge revenues. However, its earnings are likely to have received a boost from higher unit volumes, better employee productivity and lower operating expenses.

Meanwhile, the utilities and energy segment is expected to come up with stronger results, driven by increased earnings from natural gas pipelines and other energy-related operations.

Service and Retail divisions also stand to gain from an improving economic climate, with heightened consumer activity fueling revenue expansion and margin growth.

Share buybacks are likely to have supported the bottom line.

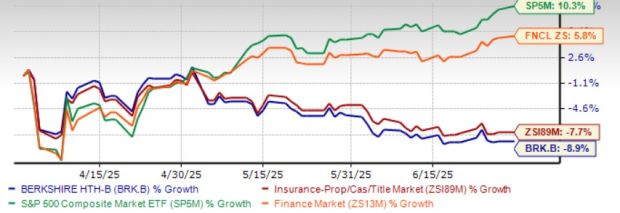

The stock underperformed the industry, sector and the S&P 500 in the second quarter of 2025.

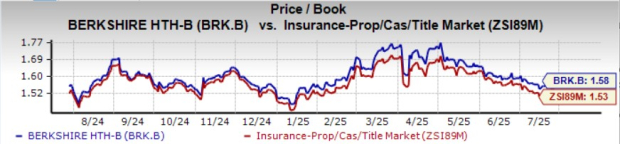

The stock is trading at a price-to-book value of 1.58X, slightly higher than the industry’s 1.53X.

It is attractively valued compared with other insurers like The Progressive Corporation PGR and The Allstate Corporation ALL.

Berkshire Hathaway’s insurance operations form the core of its business model, accounting for roughly one-quarter of total revenues and serving as a key engine of long-term growth. While its insurance operations remain the primary driver of return on equity, they are susceptible to catastrophe-related losses, which can introduce volatility to underwriting results.

Yet, Berkshire’s broad and diversified business model ensures overall stability.

The Insurance segment’s ongoing expansion has fueled growth in its insurance float—the pool of premiums held before claims are paid—which rose from around $114 billion at the end of 2017 to $173 billion by the first quarter of 2025. This float provides a low-cost source of capital that Berkshire has adeptly invested in high-quality businesses and assets with durable earnings potential and strong returns, including significant holdings in Apple, Coca-Cola, BNSF Railway, and various utility companies.

Berkshire’s solid financial standing also enables steady share repurchases—an effective capital allocation approach that contributes to long-term shareholder value creation.

Berkshire Hathaway, a conglomerate with over 90 subsidiaries spanning a wide range of industries, brings diversification and dynamism to shareholders’ portfolios.

Berkshire’s insurance business is likely to benefit from solid results at GEICO as well as higher interest income from short-term investments.

However, an unfavorable return on capital, a likely decline in the second-quarter bottom line, lowered times interest earned, and contracting margins keep us cautious. Also, given its premium valuation, investors should adopt a wait-and-see approach for BRK.B stock.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 2 hours | |

| 6 hours | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite