|

|

|

|

|||||

|

|

|

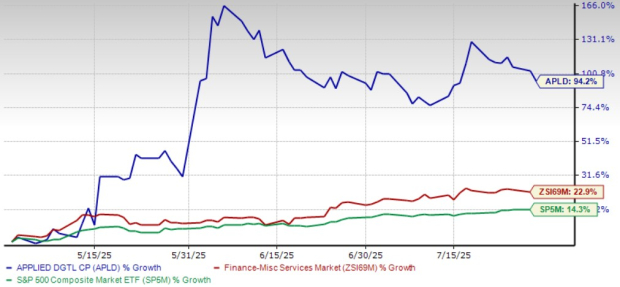

Applied Digital Corporation’s APLD shares have soared 94% over the past three months, reversing the downtrend seen through mid-April. The earlier weakness stemmed not from company-specific issues but broader industry headwinds, including lease cancellations by some hyperscalers during first-quarter 2025. However, bullish commentary from Microsoft MSFT and Meta Platforms META in their first-quarter earnings — highlighting sustained demand in hyperscale, colocation, and AI workloads — reignited investor optimism in AI infrastructure plays like APLD.

The stock has significantly outperformed the broader Finance sector’s growth of 22.9% as well as the S&P 500 Index’s 14.3% increase. This strong outperformance reflects growing investor confidence in APLD’s positioning amid the massive capital outlay expected from hyperscalers in 2025.

APLD posted a first-quarter net loss of 16 cents per share compared to earnings of 52 cents a year ago. The decline was due to elevated depreciation and amortization costs related to aggressive infrastructure expansion. With sales showing robust growth, the earnings dip is seen more as a strategic investment than an operational weakness.

With the stock’s recent surge, investors may wonder whether there’s still upside potential. Let’s evaluate the tailwinds and challenges shaping APLD’s long-term investment appeal.

Three-Month Price Performance

Booming AI Demand: Major hyperscalers, Microsoft and Meta, plan to spend $80 billion and $62.5 billion, respectively, to expand AI infrastructure. Others like Amazon, Alphabet and Oracle are also ramping up data center buildouts. Despite a 7% year-over-year decline in APLD’s Data Center Hosting sales last quarter, this surging demand may soon land APLD its first hyperscaler lease at the Ellendale campus, setting the stage for accelerated revenue growth.

Aggressive Expansion in Motion: APLD has deployed nearly $1 billion in assets over the past year, largely for data center construction. The company now operates 286 MW of fully contracted hosting capacity, mainly for Bitcoin miners, and is building three new facilities that will add another 700 MW by 2027. This buildout positions APLD to capture AI and HPC workload demand.

Improving Liquidity Position: A new $150 million equity facility allows APLD to raise capital in $25 million increments over three years, easing near-term funding needs. Additional partnerships with Macquarie Asset Management and Sumitomo Mitsui Bank further solidify its balance sheet, helping offset recent cash burn from capex-heavy operations.

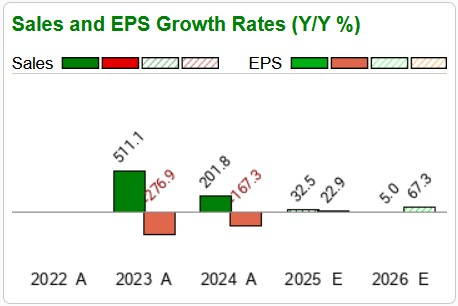

Sales and EPS Growth Rates

Despite its growth outlook, APLD faces elevated depreciation costs that may continue pressuring its bottom line in the near term. Seasonal power cost fluctuations also impacted Data Center Hosting margins in the first quarter. While overall sales rose, revenues fell short of estimates due to a 35.7% sequential drop in Cloud Services revenues, tied to operational challenges in shifting from reserved to on-demand contracts. This issue has since been resolved, and revenue normalization is expected in the coming quarters.

Infrastructure investments of $30-$50 million per month are planned for the next 12-18 months. While these projects can drive substantial long-term growth, the immediate concern is monetization. The 400 MW Ellendale campus will come online in 2025, but a lack of signed hyperscaler leases could compress near-term gross margins until utilization ramps up.

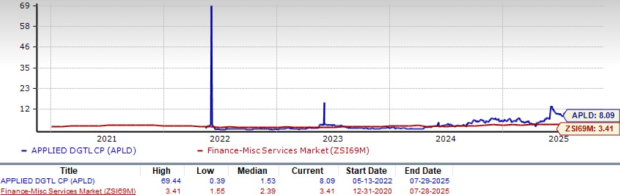

Valuation has risen sharply alongside the stock, with APLD now trading at 8.09X forward 12-month price-to-sales (P/S) versus the industry’s 3.41X and its own 5-year median of 1.53X. This premium reflects elevated growth expectations, and while it may appear stretched, it’s arguably justified given the scale of upcoming infrastructure rollouts and industry tailwinds.

5-Year P/S F-12M Ratio

While APLD’s recent stock surge has pushed valuations higher, the company is well-positioned to benefit from a generational AI infrastructure buildout. Its aggressive expansion, improving liquidity and potential for securing hyperscaler clients support a long-term bullish thesis. Investors should view near-term earnings pressure as a trade-off for future growth. Backed by compelling fundamentals and sector tailwinds, APLD now carries a Zacks Rank #2 (Buy) and remains an attractive opportunity for long-term investors willing to ride out interim volatility. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 20 min | |

| 29 min | |

| 32 min | |

| 40 min | |

| 44 min | |

| 59 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite