|

|

|

|

|||||

|

|

|

Berkshire Hathaway Inc. (BRK.B) stock is trading at about a 10% discount to its 52-week high of $542.07. The stock closed at $476.56 yesterday, after losing 1.1% in the day’s trading.

Berkshire Hathaway is a conglomerate with more than 90 subsidiaries engaged in diverse business activities. This, in turn, provides stability in various economic cycles.

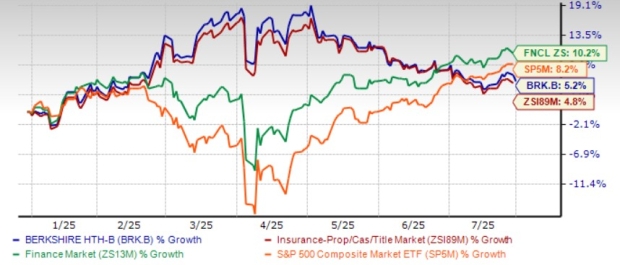

Its shares have underperformed the industry, the Finance sector, as well as the Zacks S&P 500 composite index year to date.

BRK.B is now trending below its 50-day simple moving average (SMA), indicating the possibility of a downside ahead.

Shares of Chubb Limited CB have gained 0.8% but those of The Progressive Corporation PGR have lost 2.8% year to date, respectively.

Chubb, a top global provider of property and casualty insurance and reinsurance, is strategically tapping into growth opportunities within the middle-market segment across both domestic and international regions. The company is focused on long-term growth by strengthening its core package solutions and expanding its specialty insurance product lineup. It is also advancing key strategic initiatives that support its broader expansion goals and bolster its competitive positioning.

Progressive, one of the leading auto insurers in the United States, is well-equipped to maintain profitability, driven by its strong market position, comprehensive product portfolio and outstanding underwriting and operational performance. The company has refined its strategic approach by prioritizing bundled auto insurance offerings, minimizing exposure to high-risk properties, and enhancing segmentation through innovative and targeted solutions.

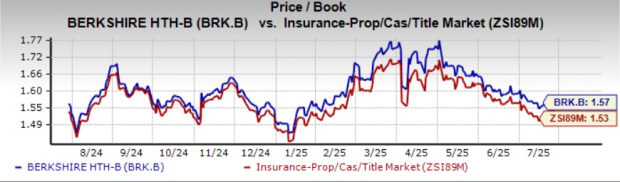

The stock is overvalued compared with its industry. It is currently trading at a price-to-book multiple of 1.57, higher than the industry average of 1.53.

Berkshire is relatively cheap compared to Progressive and Chubb.

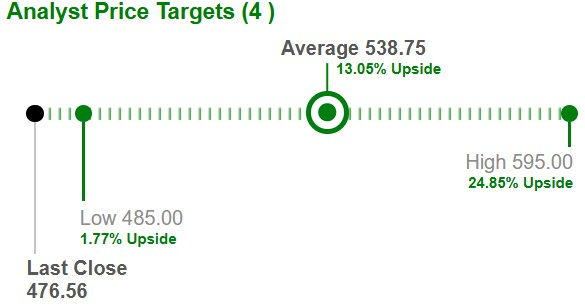

Based on short-term price targets offered by four analysts, the Zacks average price target is $538.75 per share. The average suggests a potential 13.1% upside from the last closing price.

Despite being a conglomerate, Berkshire Hathaway’s insurance operations lie at the core of its business model, generating roughly 25% of total revenues and are a key driver of long-term growth. The segment’s broad market exposure, disciplined pricing and solid underwriting performance enable it to remain resilient even during market downturns.

This strength is complemented by Berkshire’s diversified structure, which provides stability across various economic cycles. Berkshire Hathaway Energy (BHE), its regulated utility subsidiary, contributes steady, predictable cash flows and is deeply invested in renewable energy. BHE’s focus on clean power aligns Berkshire with the accelerating global shift toward electrification and sustainability.

The Utilities and Energy segment also includes Burlington Northern Santa Fe (BNSF), a critical but currently challenged asset due to a less favorable business mix and reduced fuel surcharge revenues. Nonetheless, increasing demand for utility services is expected to support the segment’s future performance.

Meanwhile, Berkshire’s Manufacturing, Service, and Retail units are well-positioned to benefit from a strengthening economy, with rising consumer activity boosting revenues and improving margins.

A major financial asset for Berkshire is its growing insurance float—funds held between premium collection and claim payouts—which increased from approximately $114 billion in 2017 to $173 billion by the first quarter of 2025. This float provides low-cost capital that the company strategically allocates to high-quality, durable investments such as Apple, Coca-Cola, BNSF and its utility assets.

Berkshire’s strong financial position also enables ongoing share repurchases, enhancing shareholder value through disciplined capital management.

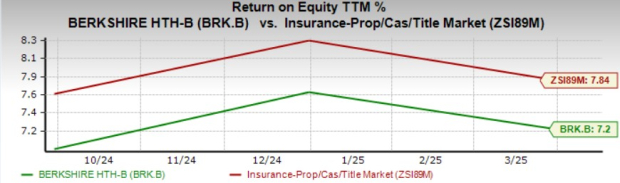

Return on equity (“ROE”) in the trailing 12 months was 7.2%, underperforming the industry average of 7.8%. Return on equity, a profitability measure, reflects how effectively a company is utilizing its shareholders’ funds. It is noteworthy that though BRK.B’s ROE is lagging the industry average, the company has been continuously generating improved ROE.

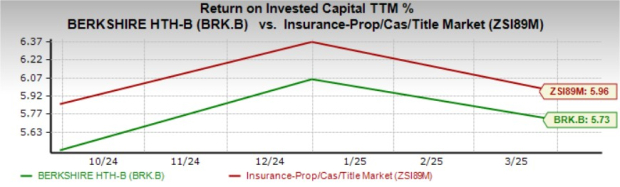

The same holds true for return on invested capital (ROIC), which has increased every year since 2020. This reflects BRK.B’s efficiency in utilizing funds to generate income. However, ROIC in the trailing 12 months was 5.7%, lower than the industry average of 6%.

The Zacks Consensus Estimate for 2025 earnings implies a 6.7% year-over-year decrease, while the same for 2026 suggests a 5% increase. The expected long-term earnings growth is pegged at 7%, better than the industry average of 6.8%.

The consensus estimate for 2025 and 2026 earnings witnessed no movement in the past 30 days.

Holding shares of Berkshire Hathaway renders dynamism to shareholders’ portfolios. BRK.B has delivered significant value to shareholders for almost six decades under the leadership of Warren Buffett.

The focus will now shift to how the behemoth performs when Greg Abel succeeds Warren Buffett as CEO of Berkshire, effective Jan. 1, 2026. Warren Buffett will continue to be the company's executive chairman.

Given Berkshire Hathaway’s premium valuation, unfavorable return on capital, an expected near-term decline in earnings and muted analyst sentiments surrounding the company, it is better to adopt a wait-and-see approach for this Zacks Rank #3 (Hold) stock.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-28 |

Stock Market Week: Reaction To Iran, Berkshire Earnings, Apple Event

BRK-B

Investor's Business Daily

|

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-27 | |

| Feb-27 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite