|

|

|

|

|||||

|

|

|

Dollar General Corporation’s DG remodel initiative may not have grabbed the headlines, but its financial and operational impact is harder to overlook. In the first quarter of fiscal 2025 alone, the company remodeled a staggering 1,227 stores — 668 through Project Elevate and 559 under Project Renovate. These efforts are part of a broader plan to execute approximately 4,885 real estate projects in 2025, including 2,000 Project Renovate and 2,250 Project Elevate remodels.

While the cost of these upgrades is substantially lower than building new stores, Dollar General expects impressive first-year annualized comp sales lifts of 6-8% for Project Renovate and 3-5% for Project Elevate, converting the mature store base into a growth engine.

What makes this remodel strategy powerful is its dual benefit — revitalizing aging stores and improving the in-store experience with category updates and merchandising enhancements. This boosts store productivity per square foot. Additionally, with remodels targeting nearly 20% of the store base each year, DG maintains a continuous refresh cycle without overextending capital.

Dollar General’s ability to complete most of these remodels by the third quarter also allows for extended sales benefits throughout the fiscal year. With improved shelf availability, leaner inventory and better store standards accompanying these remodels, the company is achieving significant operational improvements.

With store construction costs up 40% since 2019, Dollar General’s strategic pivot toward remodeling over rapid expansion appears well-calculated. If the early indicators hold, DG may be rewriting the playbook on how to grow without adding square footage.

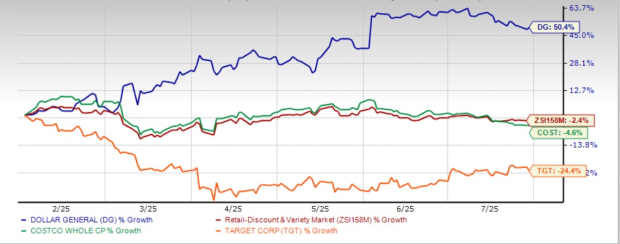

Dollar General stock has rallied 50.4% over the past six months against the industry’s decline of 2.4%. The company has also comfortably outperformed key peers such as Target Corporation TGT and Costco Wholesale Corporation COST. During the same period, Target shares have declined 24.4%, while Costco has seen a 4.6% drop.

Dollar General’s forward 12-month price-to-earnings ratio of 17.60 reflects a lower valuation compared to the industry’s average of 31.65. DG carries a Value Score of A. DG is trading at a premium to Target (with a forward 12-month P/E ratio of 13.28) but at a discount to Costco (47.31).

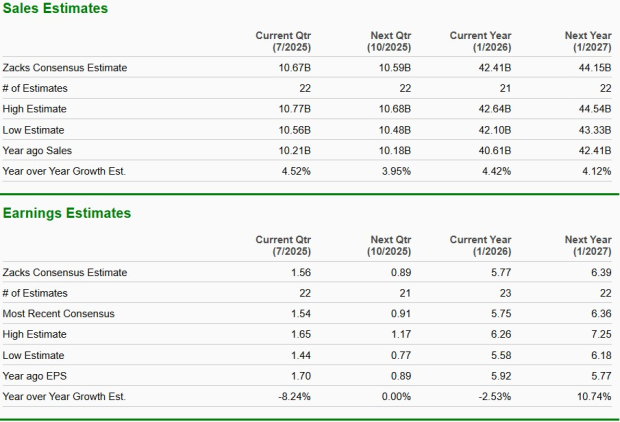

The Zacks Consensus Estimate for Dollar General’s current financial-year sales suggests year-over-year growth of 4.4%, while estimates for earnings per share imply a decline of 2.5%.

Dollar General currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite