|

|

|

|

|||||

|

|

|

Sysco Corporation SYY is currently trading at a discount to its historical and industry benchmarks. The SYY stock trades at a forward 12-month price-to-earnings ratio of 15.29, below its median level of 16.04 in the past year and lower than the industry’s average of 16.22. This suggests that SYY may be undervalued relative to its earnings potential, presenting an attractive opportunity for investors. The company's current Value Score of B further highlights its potential for long-term growth.

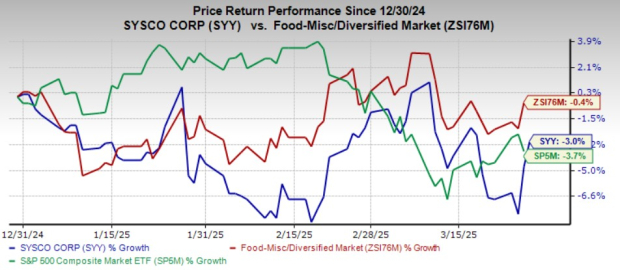

SYY’s shares have lost 3% in the past three months compared with the industry and the S&P 500 index’s decline of 0.4% and 3.7%, respectively. Currently trading at $74.04, SYY is 10% below its 52-week high of $82.23, touched on Dec. 6, 2024, presenting a compelling opportunity for value-focused investors, while regaining ground. While recent fluctuations indicate near-term challenges, SYY’s strategic initiatives and strong market position could support a potential recovery.

Let us analyze the fundamentals of Sysco to understand the key drivers behind its market position and financial resilience.

Sysco is actively enhancing efficiency through supply-chain optimization and structural cost-containment efforts. The company has made significant strides in improving supply-chain productivity, critical for maintaining competitive service levels in the foodservice industry. On July 1, 2024, Sysco introduced a performance-based sales compensation model to incentivize sales growth and drive new customer acquisitions. This, combined with targeted hiring in high-growth regions, aligns workforce incentives with organizational goals to enhance both operational and sales efficiency.

Despite broader market challenges, Sysco is experiencing strong momentum in the Food-Away-From-Home channel. In the second quarter of fiscal 2025, U.S. Foodservice operations saw a 4.1% sales increase, with total case volumes rising 1.4%. The International Foodservice segment also posted a 3.6% sales increase. By prioritizing innovation and tailored solutions for its diverse customer base, Sysco is well-positioned to capitalize on shifting industry trends, supporting long-term growth and profitability.

Strategic acquisitions remain a key pillar of Sysco’s expansion strategy. On the last earnings call, management highlighted merger and acquisition opportunities in both Ireland and Great Britain over the past year, strengthening the specialty capabilities in produce and protein. These acquisitions enhance Sysco’s distribution network and customer reach, reinforcing its competitive edge in the global foodservice industry.

Sysco continues to grapple with inflationary pressures, which have weighed on profitability. In the second quarter of fiscal 2025, product cost inflation rose 2.1%, caused by higher dairy and poultry prices. The impact of avian influenza has led to increased costs for eggs and poultry, while supply constraints have driven up prices in the broader protein segment.

Sysco is facing macroeconomic challenges characterized by a notable decline in restaurant traffic, which dropped 2% in the fiscal second quarter. This decline affected local case volume within U.S. Foodservice, which decreased 0.9% year over year. Persistent inflation and economic uncertainty could further pressure consumer spending, potentially slowing Sysco’s recovery and weighing on demand for its foodservice products.

Sysco has demonstrated resilience, driven by its strategic initiatives and strong market position. Despite challenges such as inflationary pressures and a decline in restaurant traffic, the company’s focus on supply-chain optimization, targeted acquisitions and sales efficiency supports long-term growth. While its attractive valuation presents an appealing opportunity, a difficult consumer environment remains a concern. All said, current stakeholders should maintain their position in the stock. Currently, Sysco carries a Zacks Rank #3 (Hold).

United Natural Foods, Inc. UNFI distributes natural, organic, specialty, produce and conventional grocery and non-food products in the United States and Canada. It currently carries a Zacks Rank of 2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The consensus estimate for United Natural Foods’ current financial-year sales and earnings implies growth of 1.9% and 485.7%, respectively, from the year-ago figures. UNFI delivered a trailing four-quarter earnings surprise of 408.7%, on average.

Utz Brands UTZ engages in the manufacture, marketing and distribution of snack foods in the United States and presently carries a Zacks Rank of 2. UTZ delivered a trailing four-quarter earnings surprise of 8.8%, on average.

The Zacks Consensus Estimate for Utz Brands’ current financial-year sales and earnings indicates growth of 1.2% and 10.4%, respectively, from the year-ago numbers.

BRF S.A. BRFS raises, produces and slaughters poultry and pork for processing, production and sale of fresh meat, processed products, pasta, margarine, pet food and other products. It currently carries a Zacks Rank of 2. BRFS delivered a trailing four-quarter earnings surprise of 9.6%, on average.

The Zacks Consensus Estimate for BRF S.A.'s current fiscal-year sales and earnings indicates growth of 0.3% and 22.2%, respectively, from the prior-year levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 3 hours | |

| 6 hours | |

| Feb-23 | |

| Feb-20 | |

| Feb-19 | |

| Feb-18 | |

| Feb-18 | |

| Feb-16 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite