|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

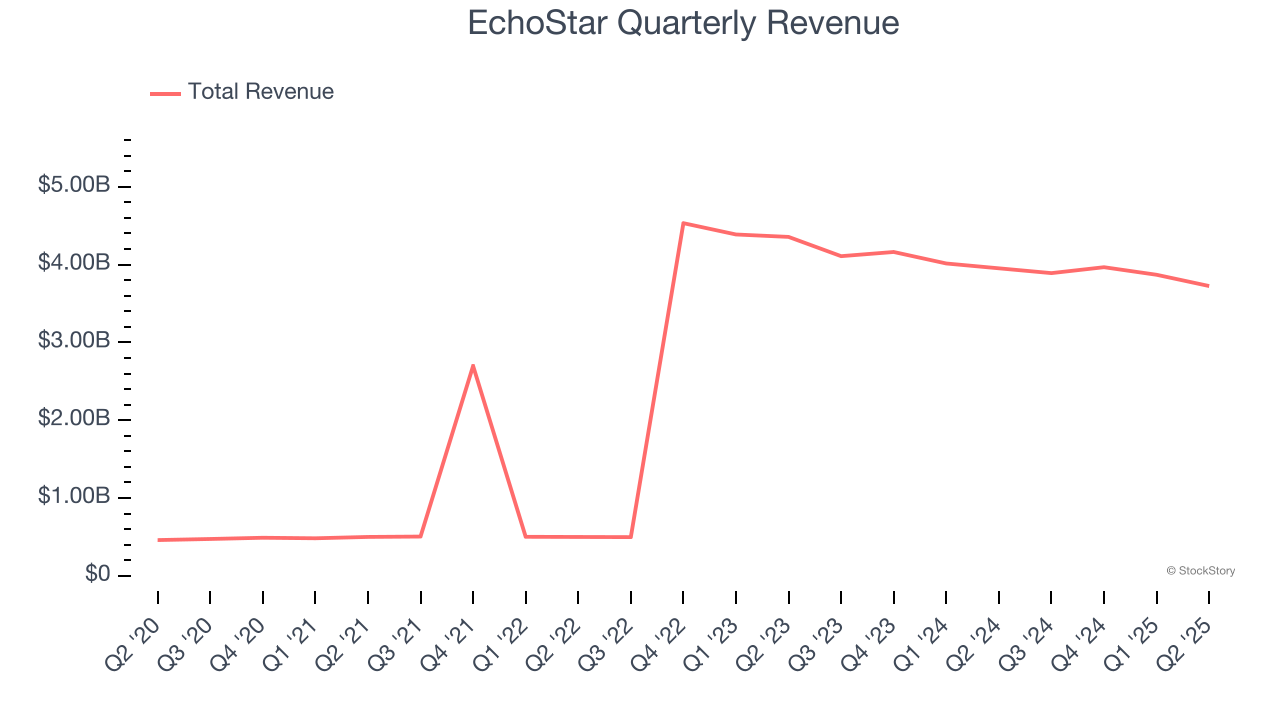

Satellite communications company EchoStar (NASDAQGS:SATS) fell short of the market’s revenue expectations in Q2 CY2025, with sales falling 5.8% year on year to $3.72 billion. Its GAAP loss of $1.06 per share was 7.7% below analysts’ consensus estimates.

Is now the time to buy EchoStar? Find out by accessing our full research report, it’s free.

"EchoStar performed well in the second quarter and was in line with our high performance expectations," said Hamid Akhavan, president and CEO, EchoStar Corporation.

Following its 2023 acquisition of DISH Network, EchoStar (NASDAQ:SATS) provides satellite communications, pay-TV services, wireless networks, and broadband solutions across consumer and enterprise markets.

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $15.45 billion in revenue over the past 12 months, EchoStar is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices.

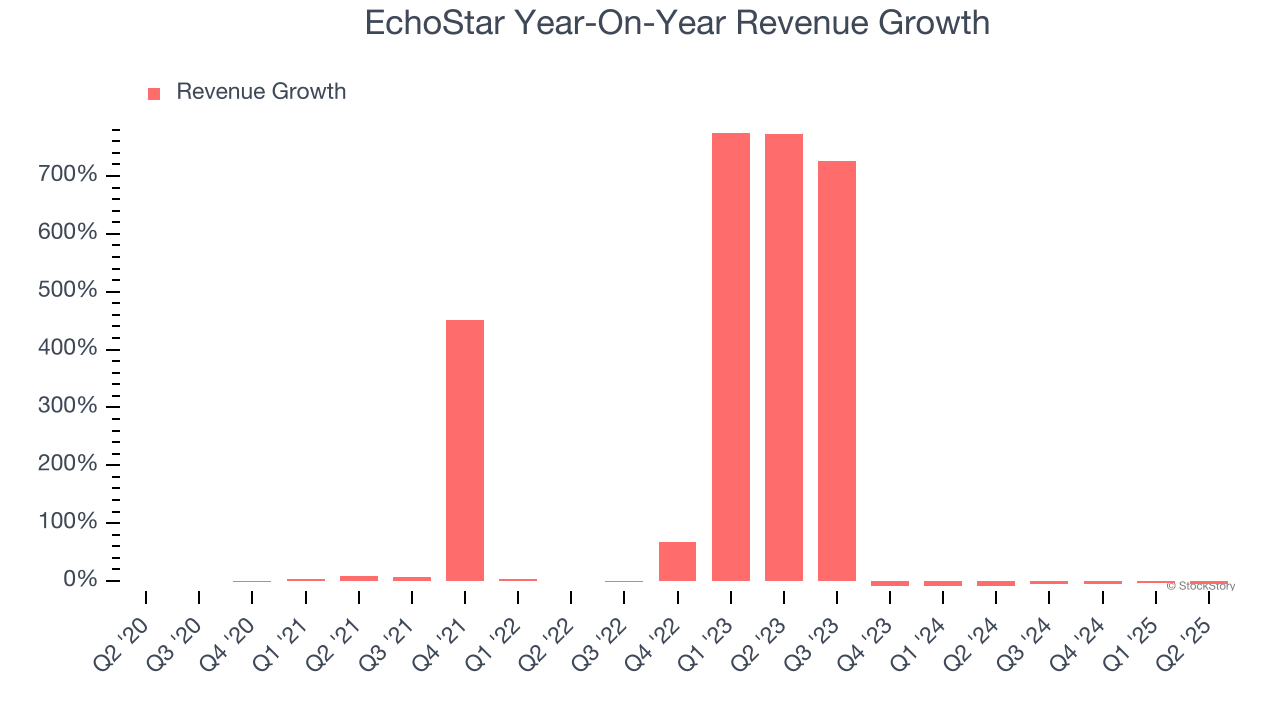

As you can see below, EchoStar’s 52.1% annualized revenue growth over the last five years was incredible. This shows it had high demand, a useful starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. EchoStar’s annualized revenue growth of 5.9% over the last two years is below its five-year trend, but we still think the results were respectable.

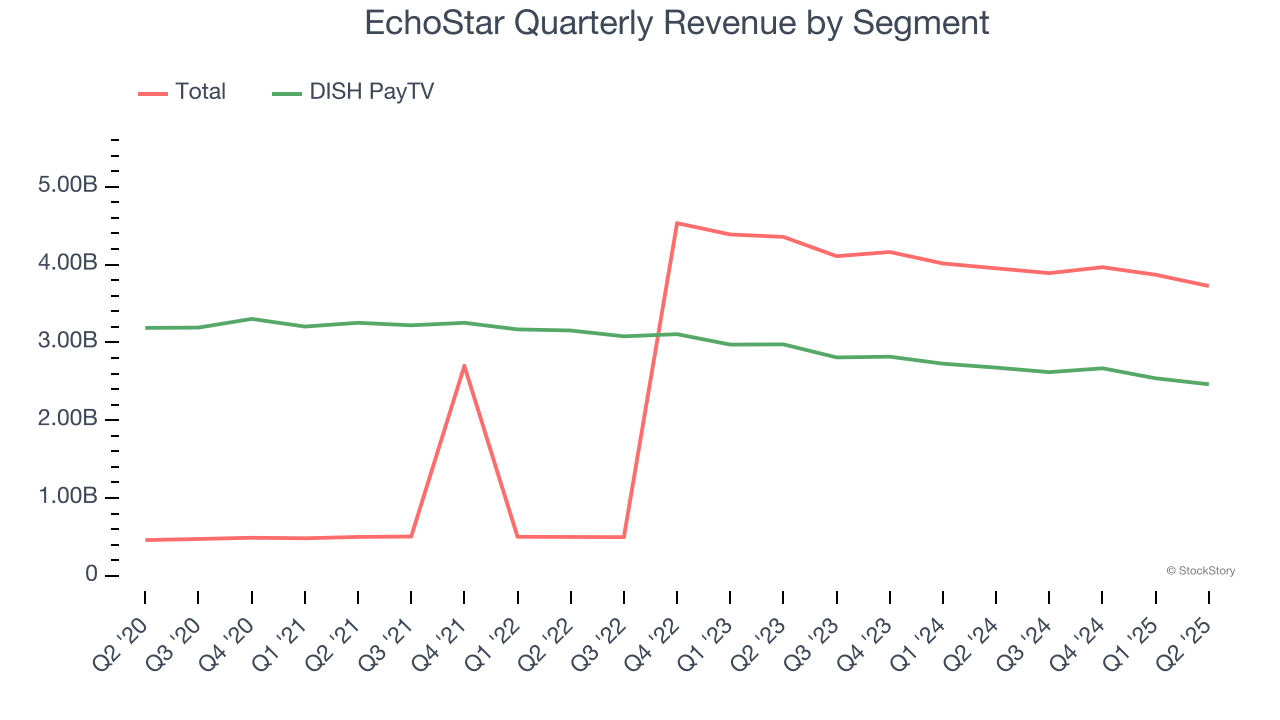

EchoStar also breaks out the revenue for its most important segment, DISH PayTV. Over the last two years, EchoStar’s DISH PayTV revenue averaged 7.9% year-on-year declines. This segment has lagged the company’s overall sales.

This quarter, EchoStar missed Wall Street’s estimates and reported a rather uninspiring 5.8% year-on-year revenue decline, generating $3.72 billion of revenue.

Looking ahead, sell-side analysts expect revenue to decline by 2.7% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

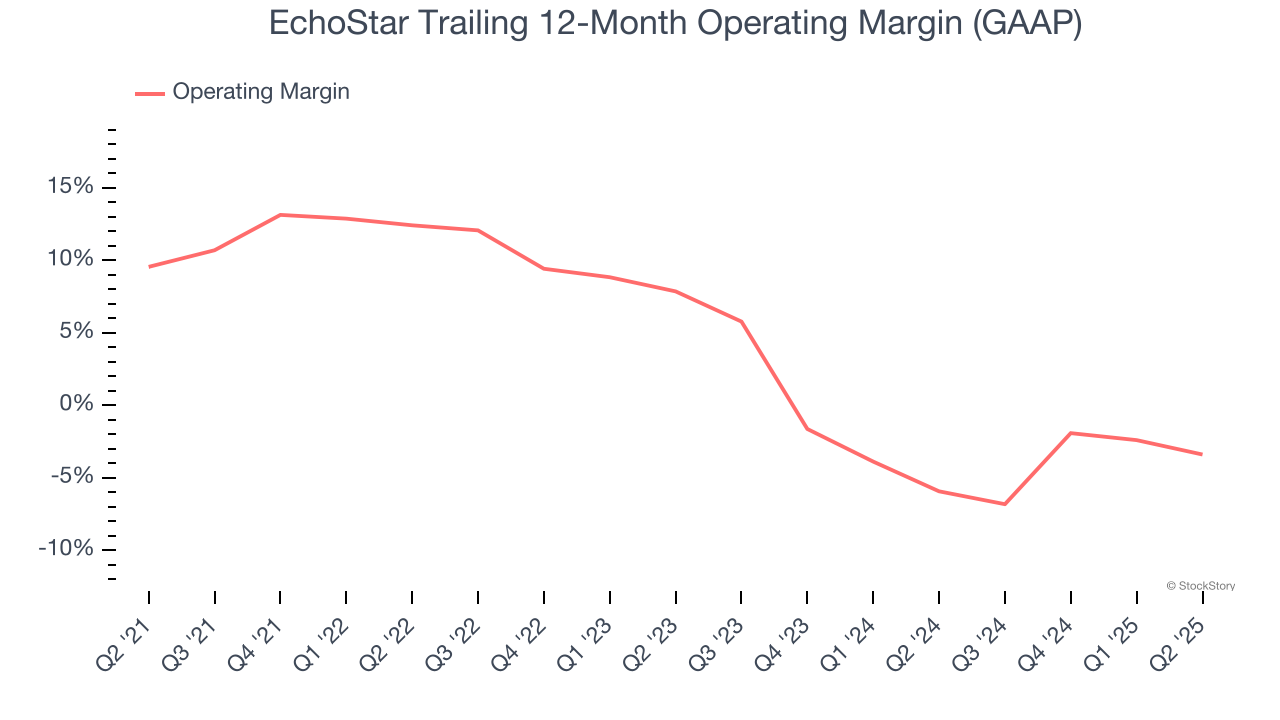

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

EchoStar was roughly breakeven when averaging the last five years of quarterly operating profits, inadequate for a business services business.

Looking at the trend in its profitability, EchoStar’s operating margin decreased by 13 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. EchoStar’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q2, EchoStar generated an operating margin profit margin of negative 5.7%, down 4.1 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

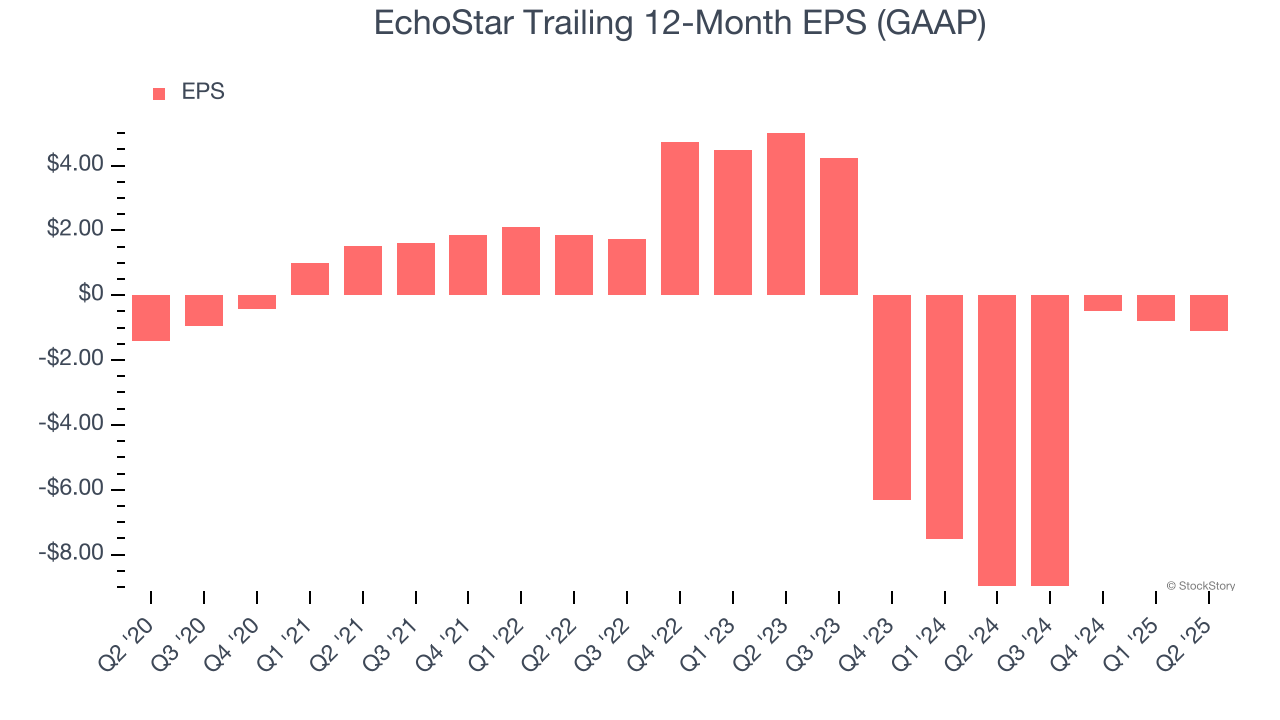

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although EchoStar’s full-year earnings are still negative, it reduced its losses and improved its EPS by 4.8% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for EchoStar, its EPS declined by 49% annually over the last two years while its revenue grew by 5.9%. This tells us the company became less profitable on a per-share basis as it expanded.

We can take a deeper look into EchoStar’s earnings to better understand the drivers of its performance. EchoStar’s operating margin has declined by 11.5 percentage points over the last two years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q2, EchoStar reported EPS at negative $1.06, down from negative $0.76 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects EchoStar to perform poorly. Analysts forecast its full-year EPS of negative $1.10 will tumble to negative $4.72.

We struggled to find many positives in these results. Its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 8.8% to $29.70 immediately following the results.

EchoStar’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-18 | |

| Feb-17 | |

| Feb-17 | |

| Feb-05 | |

| Feb-05 | |

| Feb-04 | |

| Feb-03 | |

| Feb-03 | |

| Feb-03 | |

| Jan-31 | |

| Jan-30 | |

| Jan-30 | |

| Jan-30 | |

| Jan-29 | |

| Jan-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite