|

|

|

|

|||||

|

|

|

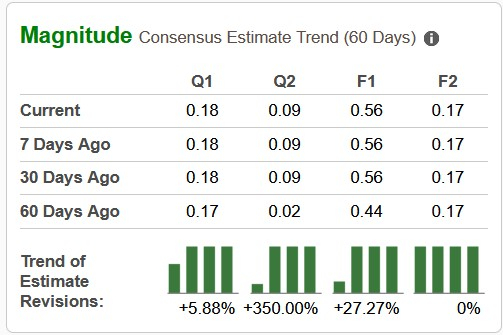

Aurora Cannabis ACB is slated to release first-quarter fiscal 2026 results on Aug. 6, before market open. The Zacks Consensus Estimate for earnings and revenues is pegged at 18 cents per share and $70.88 million, respectively.

The earnings estimate, which has remained stable over the past seven days, indicates a whopping 263.6% growth year over year. The Zacks Consensus Estimate for quarterly revenues suggests a year-over-year increase of 5.4%.

The consensus mark for fiscal 2026 revenues is pegged at $272.1 million, implying a rise of 7.6% year over year, and the same for EPS is pinned at 56 cents, suggesting a year-over-year improvement of 100%. This medical cannabis producer’s earnings surpassed the Zacks Consensus Estimate in three of the trailing four quarters and missing once, delivering an average surprise of 50.10%.

Per our proven model, a stock with a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold), along with a positive Earnings ESP, has higher chances of beating estimates. This is not the case here, as you can see below.

Earnings ESP: ACB has an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Zacks Rank: The company currently carries a Zacks Rank #4 (Sell). You can see the complete list of today’s Zacks #1 Rank stocks here.

Aurora Cannabis is slated to report fiscal first-quarter 2026 results later this week, following a record-setting fiscal 2025 driven by its focused “medical-first” strategy. The upcoming results are expected to reflect sustained momentum in global medical cannabis sales, supported by expanded product offerings, ongoing international market penetration and operational excellence.

Australia continues to be a key growth lever, where Aurora Cannabis recently expanded its IndiMed portfolio with the launch of TEMPO 22 cultivars, catering to rising patient demand for high-potency, value-segment medical cannabis. The company’s deep-rooted infrastructure and longstanding relationships in the region have fortified its second-highest market share position, with management optimistic about further patient accessibility and product uptake. This is likely to have boosted top-line growth in the soon-to-be-reported quarter.

In Europe, strong performance in Germany is likely to have led the top-line growth during the fiscal first quarter, benefiting from cannabis de-scheduling and increasing patient registrations. Aurora Cannabis’ strategic focus on ensuring consistent product availability has been crucial, while the ramp-up of German-cultivated IndiMed offerings must have further cemented its leadership. Sales are likely to have been hurt by temporary regulatory headwinds in Poland. However, management remains bullish on the market’s long-term growth prospects, underpinned by planned launches of high-quality cultivars.

Additionally, the U.K. business is expected to have gained traction from the launch of inhalable cannabis concentrates, an innovative format catering to evolving patient needs. These product introductions mark another step in Aurora Cannabis’ mission to diversify dosage forms and enhance patient access in global markets.

On the operational front, the recent $3 million upgrade to Aurora Cannabis’ Alpine facility in British Columbia has doubled yields and potency, which might have supported top-line growth with a new supply line in place.

While management anticipates first-quarter revenues to be slightly lower than the fourth-quarter fiscal 2025 level due to temporary international market fluctuations, margins are expected to remain robust, supported by a favorable product mix and continued cost discipline. Adjusted EBITDA is projected to moderate sequentially but remain positive, maintaining Aurora Cannabis’ position as one of the few profitable global cannabis players.

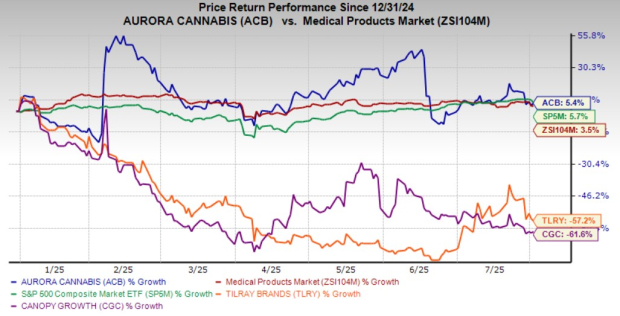

On a year-to-date basis, shares of ACB have gained 5.4%, outperforming its close peers, Tilray Brands TLRY and Canopy Growth CGC and the Medical Products industry.

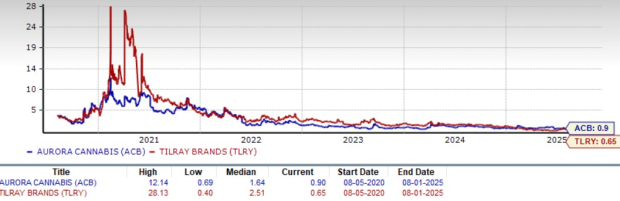

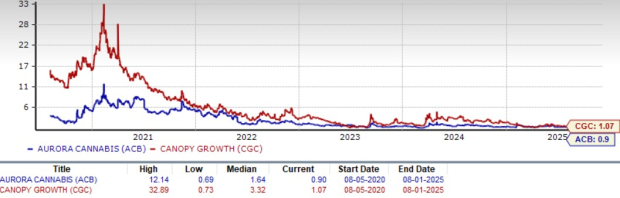

In terms of valuation, Aurora Cannabis trades at a forward 12-month P/S of 0.9 — above Tilray Brands (0.65) and below Canopy Growth (1.07). Despite Tilray Brands offering lower multiples, ACB’s premium reflects stronger growth expectations. Moreover, a higher valuation of Canopy Growth despite its declining share price makes it an expensive choice.

ACB vs TLRY

ACB vs CGC

While Aurora Cannabis continues to demonstrate strong execution in its global medical cannabis strategy, near-term headwinds warrant a cautious stance. Temporary regulatory disruptions in Poland, competitive pressures in international markets, and the anticipated sequential revenue dip in first-quarter fiscal 2026 temper immediate upside potential. Additionally, while Aurora Cannabis’ margin profile remains industry-leading, further scalability in high-margin markets is essential to drive meaningful top-line growth. With the stock’s recent gains reflecting much of the operational improvements, it would be wise for investors to await clearer visibility on sustained revenue acceleration and international market stabilization.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-01 | |

| Jun-30 | |

| Jun-30 | |

| Jun-29 | |

| Jun-29 | |

| Jun-26 | |

| Jun-25 | |

| Jun-25 | |

| Jun-25 | |

| Jun-24 | |

| Jun-24 | |

| Jun-22 | |

| Jun-18 | |

| Jun-18 | |

| Jun-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite