|

|

|

|

|||||

|

|

|

Investors can buy Netflix, Inc. (NFLX) stock roughly 15% below its all-time highs and at some of its most oversold RSI levels over the past few years to start August.

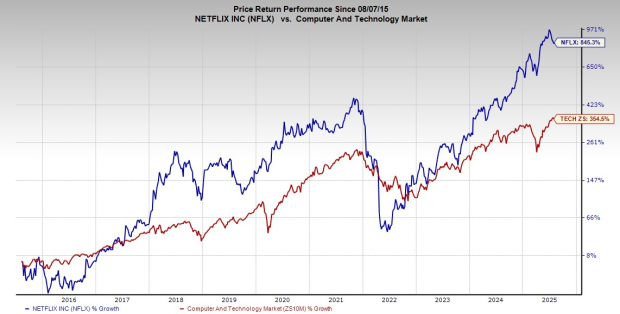

Netflix easily outperformed the stock market and the Tech sector over the last several years, without the benefit of artificial intelligence euphoria. The streaming TV and technology giant is also far less exposed to potential tariff and trade war setbacks compared to many of its big tech peers.

Wall Street took profits on Netflix stock throughout July after its furious first-half rally that’s part of a 550% surge off its summer 2022 lows. Despite this charge, and its massive long-term outperformance, Netflix offers investors great value.

Investors sold the news after the streamer’s beat-and-raise second quarter earnings release on July 17, which confirmed Netflix’s robust growth outlook in a non-speculative and stable growth area of the economy that’s not reliant on the AI revolution.

This backdrop makes Netflix one of the best technology stocks to buy in the second half of 2025.

Netflix stock tumbled between November 2021 and July 2022 as Wall Street feared its growth days were numbered and that it wouldn’t be able to churn out huge profits like Apple and other mega-cap tech stocks.

That selloff seems like a lifetime ago. Netflix successfully addressed all of Wall Street’s worst fears and then some, helping the stock blow away all of the Magnificent 7 stocks outside of Nvidia during the past three years. More recently, NFLX has charged 95% higher in the last year, tripling the Zacks Tech sector.

NFLX rolled out a lower-cost, ad-supported subscription plan in the fall of 2022. Netflix has also successfully raised prices on its top-tier premium plans while remaining one of the best deals in streaming TV for ad-based plans compared to Disney and other rivals. And the company effectively cracked down on account sharing to help boost user growth.

Netflix added 18.9 million paid subscriptions in Q4 2024, marking its largest quarter of net adds on record, topping the Covid-lockdown surge. It closed 2024 with 301.63 million global paid memberships, up 16% year-over-year. NFLX announced last April that it would stop disclosing subscriber growth each quarter starting with the first quarter of 2025, though it will publicize major milestones.

Image Source: Zacks Investment Research

The company effectively streamlined its operations, grew its user base, rolled out more content, and, most importantly, expanded its bottom line. Netflix has also improved its balance sheet, and its board authorized an additional $15 billion stock buyback program in early 2025.

On a macro level, Netflix doesn’t need to spend billions of dollars on data centers or other AI-focused growth efforts to thrive. On a speculative note, NFLX could be due for a stock split, with it trading at around $1,170 a share.

Netflix completely transformed Hollywood entertainment and television over the last 15-plus years, turning it into one of the biggest winners on Wall Street. The company remains near the top of the crowded streaming industry despite growing challenges from deep-pocketed rivals such as Apple (AAPL) and Amazon, and heavy investments from Disney (DIS) and other traditional titans.

NFLX’s successful expansion into big-budget blockbuster movies and TV and reality TV are helping it thrive as the U.S. and the world cut the cord for good. Live sports were the last hope for linear TV and the biggest market for television advertising.

Yet Disney is launching a full-scale direct-to-consumer streaming version of ESPN in the fall at a $29.99 per month price point. Netflix already made its way into live sports, landing deals with the NFL, WWE, boxing, and more. On top of that, it's rolling out more video game content to make it as close to a one-stop entertainment shop as possible.

There is growing speculation that Netflix will experiment with user-generated content to help compete against YouTube, which owns the largest share of TV viewing (12%), according to Nielsen, ahead of Disney, Paramount, NBC Universal, and Netflix.

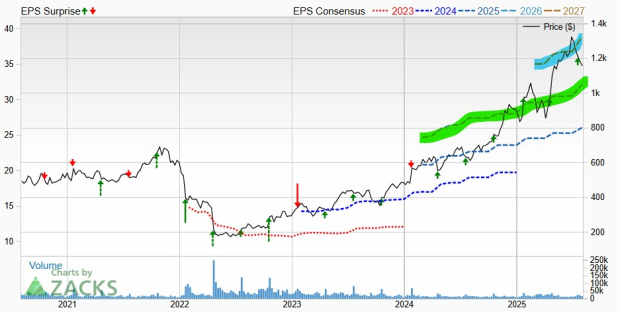

NFLX topped our Q2 earnings estimate on July 17 and provided upbeat guidance, with its FY26 consensus up over 5% since then. The company’s recently improving earnings outlook earns Netflix a Zacks Rank #1 (Strong Buy) and extends its impressive run of upward earnings revisions.

The company confirmed last quarter its plans to “roughly double ads revenue in 2025.” Separately, The Wall Street Journal reported earlier this year that Netflix is aiming to double its annual revenue by 2030.

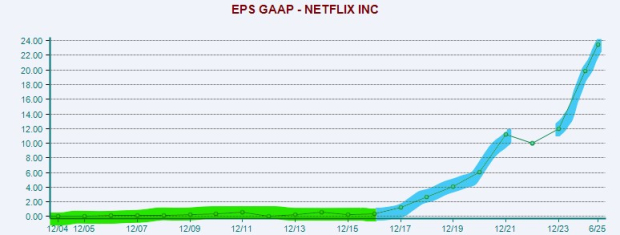

In the short run, NFLX is projected to increase its revenue by 16% in 2025 and 13% next year to reach nearly $51 billion, doubling its 2020 total.

The streaming company more than tripled its earnings between 2020 and 2024. Netflix is expected to grow its EPS by another 31% in 2025 and 23% in FY26, following 65% growth last year. The company is targeting a 29.5% operating margin for 2025, up from 26.8% last year.

Netflix was one of the best-performing stocks of the 2010s, and it is up 260% since the start of 2020 to outpace Tech’s 150%. It soared 415% in the last three years and 550% from its 2022 lows, leaving all of the Magnificent 7 (outside of Nvidia) in the dust.

Despite its roughly 15% drop from its June 30 peaks, NFLX is still up 30% in 2025 vs. Tech’s 9%. The pullback over the last month has it trading at some of its lowest RSI levels over the past five years, down from some of its highest.

The stock is trying to hold its ground near its late April/early May breakout levels and its long-term 21-week moving average.

Any drop to Netflix's 200-day would likely represent an even better buying opportunity. But playing the market timing game is no easy task.

Image Source: Zacks Investment Research

Netflix's pullback might not last much longer since it trades at more than a 90% discount to its 10-year highs and 31% below its 10-year median at 39X forward earnings.

On the price-to-earnings-to-growth (PEG) ratio front, Netflix trades in line with Tech at 1.7 despite its massive outperformance and nearly 60% below its five-year highs. Disney's PEG ratio sits at 1.6, yet DIS stock climbed just 14% in the past 10 years.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 29 min | |

| 32 min | |

| 57 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite