|

|

|

|

|||||

|

|

|

General Motors GM sold more than 19,000 electric vehicles (EVs) last month, up a whopping 115% year over year. The surge was largely led by strong demand for the Chevrolet Equinox EV model. The US legacy automaker is advancing well in its electrification journey, thanks to its robust portfolio, including 13 models across its Chevrolet, GMC and Cadillac brands.

General Motors was the second-largest EV seller in the United States last year, just behind Tesla TSLA and managed to keep up the momentum through the first half of 2025. General Motors’ EV sales in the last reported quarter more than doubled. Meanwhile, GM’s closest peer, Ford F, witnessed more than a 30% drop in second-quarter EV sales year over year. EV giant Tesla recorded a 13.4% decline in deliveries in the three months ending June.

While General Motors' EV sales have been impressive, it will be interesting to watch if the company can sustain its sales growth amid policy shifts and U.S. President Trump’s unfriendly stance on e-mobility. Let’s take a closer look at the company’s fundamentals to assess if General Motors is worth buying at the moment.

General Motors’ second-quarter 2025 earnings beat was its 12th straight quarterly beat. Strong vehicle demand and stable vehicle pricing led to record first-half 2025 revenues of $91 billion. GMNA (General Motors North America) segment revenues were also a first-half record at roughly $77 billion.

The company was hit with $1.1 billion in net tariffs in the last reported quarter, although EPS of $2.53 exceeded expectations by 6%. However, GM expects net tariff costs in the third quarter to be higher than in the second quarter. It stuck to its guidance of gross tariff impact of $4-$5 billion for the full year but expects to offset roughly 30% of that through strategic initiatives like cost cuts, stable pricing and production adjustments. GM reaffirmed its adjusted EBIT forecast for the full year between $10 billion and $12.5 billion.

General Motors Company price-consensus-eps-surprise-chart | General Motors Company Quote

In the first half of the year, GM’s U.S. market share climbed to 17.3%, up 1.2 percentage points from the same period last year — a steady, positive trend. The company continues to expand its U.S. manufacturing footprint and domestic supply chain, while also investing heavily in battery, software, and autonomous vehicle innovation. Internationally, GM is making meaningful progress. In China, it’s working closely with its joint venture partner to improve sales, streamline inventory and boost profitability.

The strong performance of its new energy vehicles is also boosting results. Chevrolet has emerged as the number two EV brand in the United States, thanks to the success of the Blazer EV and Equinox EV. Meanwhile, Cadillac became the fifth-largest EV brand in the last reported quarter. GM is also scaling its hands-free driving system, Super Cruise. The technology is on track to generate over $200 million in revenues in 2025, with expectations to more than double by 2026.

The company’s investor-friendly moves also augur well. It completed a $2 billion accelerated share repurchase program in the second quarter of 2025, retiring 10 million more shares. This brings the total shares bought back under that program to 43 million. Notably, GM resumed open market buybacks in early July.

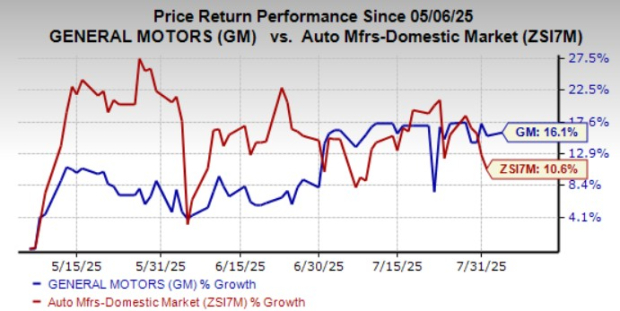

Over the past three months, shares of General Motors have risen 16%, outperforming the industry as well as Ford and Tesla, which gained 5% and 12%, respectively.

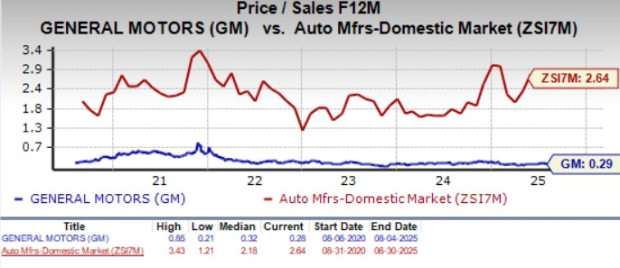

From a valuation standpoint, General Motors appears relatively undervalued. The stock trades at a forward price-to-sales (P/S) ratio of just 0.29, well below the industry’s 2.64. GM also boasts a Value Score of A. In comparison, Tesla and Ford trade at a P/S ratio of 9.7 and 0.27, respectively

While GM continues to make strides in EVs and innovation, near-term headwinds are worth noting. Fleet pricing has come under pressure due to rising competition, and this trend is expected to persist in the second half of the year. GM also flagged higher warranty costs, particularly for the L87 powertrain and early EV software issues, which will be a drag in 2025.

Capital spending remains high and can weigh on free cash flow. While the company expects 2025 capex to be in the range of $10–$11 billion, the figure is expected to rise slightly to $10–$12 billion in 2026 and 2027 as GM ramps up production and future model launches.

The Zacks Consensus Estimate for GM’s 2025 EPS and sales implies a year-over-year decline of 11% and 4.3%, respectively.

Adjusted EBIT for the first half of the year came in at $6.5 billion. Based on full-year guidance, second-half earnings are expected to be about $1.75 billion lower at the midpoint of the outlook. This is essentially due to three reasons. First, tariffs will remain a burden. Second, the company expects lower wholesale volumes in North America. Lastly, increased spending to prepare for the rollout of next-gen full-size trucks and the expansion of U.S. EV capacity will also weigh on the results.

Additionally, EV profitability may take a hit from softening demand because of the phase-out of government incentives like the federal tax credit. Given these headwinds, this isn’t the best time for new investors to jump in.

The stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite