|

|

|

|

|||||

|

|

|

E-commerce software platform Shopify (NYSE:SHOP) beat Wall Street’s revenue expectations in Q2 CY2025, with sales up 31.1% year on year to $2.68 billion. On top of that, next quarter’s revenue guidance ($2.76 billion at the midpoint) was surprisingly good and 4.6% above what analysts were expecting. Its GAAP profit of $0.69 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Shopify? Find out by accessing our full research report, it’s free.

Originally created as an internal tool for a snowboarding company, Shopify (NYSE:SHOP) provides a software platform for building and operating e-commerce businesses.

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Shopify’s 26% annualized revenue growth over the last three years was solid. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, Shopify reported wonderful year-on-year revenue growth of 31.1%, and its $2.68 billion of revenue exceeded Wall Street’s estimates by 5.2%. Company management is currently guiding for a 27.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 19% over the next 12 months, a deceleration versus the last three years. We still think its growth trajectory is attractive given its scale and suggests the market is baking in success for its products and services.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

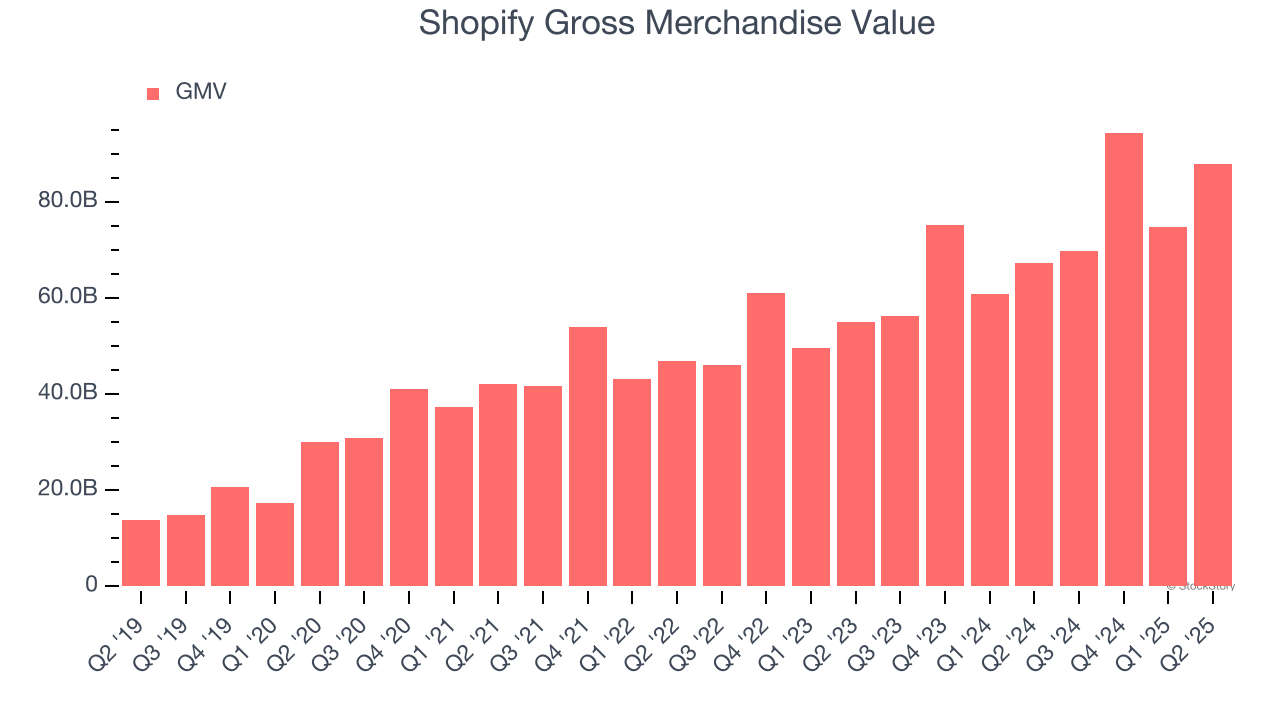

GMV, or gross merchandise value, is the total value of goods and services sold on Shopify’s platform. This is the number from which the company will ultimately collect fees (usually called a take rate), and the higher it is, the higher the switching costs, enabling Shopify to monetize in additional ways (like subscription revenue for more services).

Shopify’s GMV punched in at $87.84 billion in Q2, and over the last four quarters, its growth was impressive as it averaged 25.8% year-on-year increases. This alternate topline metric grew slower than total sales, meaning its revenue from adjacent products such as merchant loans and AI-driven inventory management software outpaced its transaction fees. This signals the company is locking its customers further into its platform and mining them for profits.

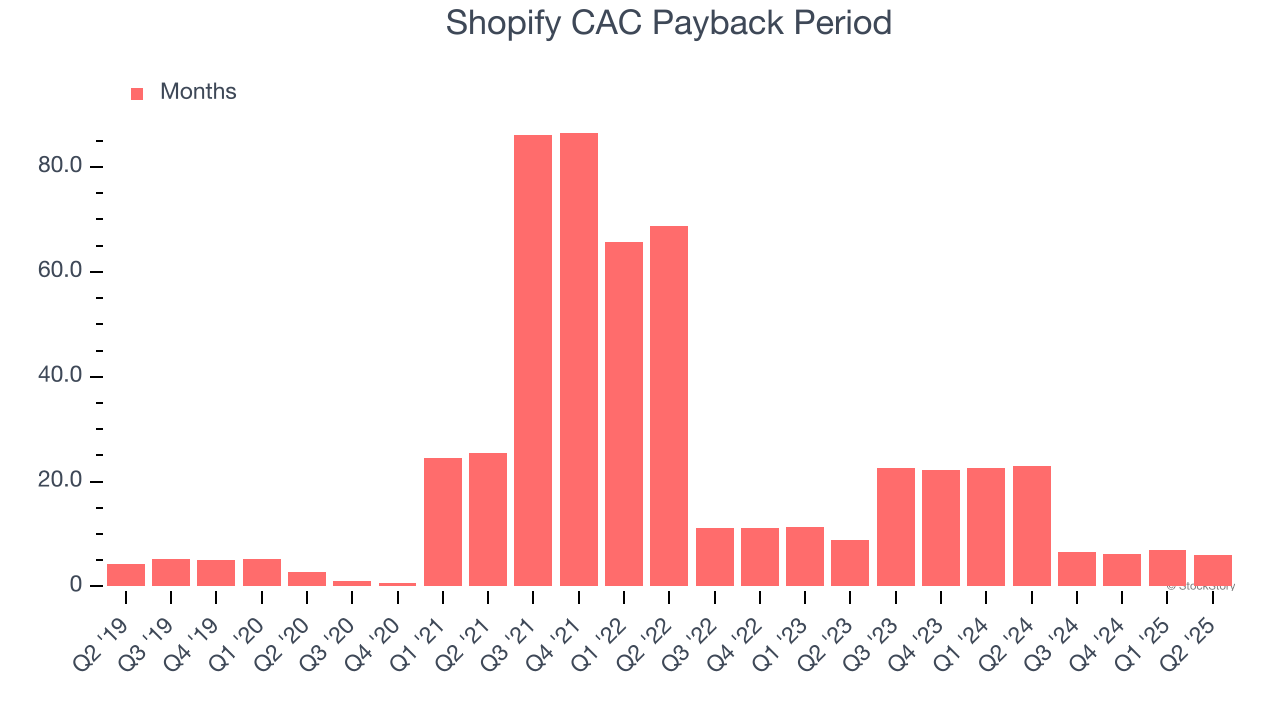

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Shopify is extremely efficient at acquiring new customers, and its CAC payback period checked in at 6 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation due to its scale. These dynamics give Shopify more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

We were impressed by how significantly Shopify blew past analysts’ gross merchandise volume expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Looking ahead, Q3 revenue guidance came in ahead of expectations as well. Zooming out, we think this was a very solid print. The stock traded up 10.5% to $140.49 immediately following the results.

Sure, Shopify had a solid quarter, but if we look at the bigger picture, is this stock a buy? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite