|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

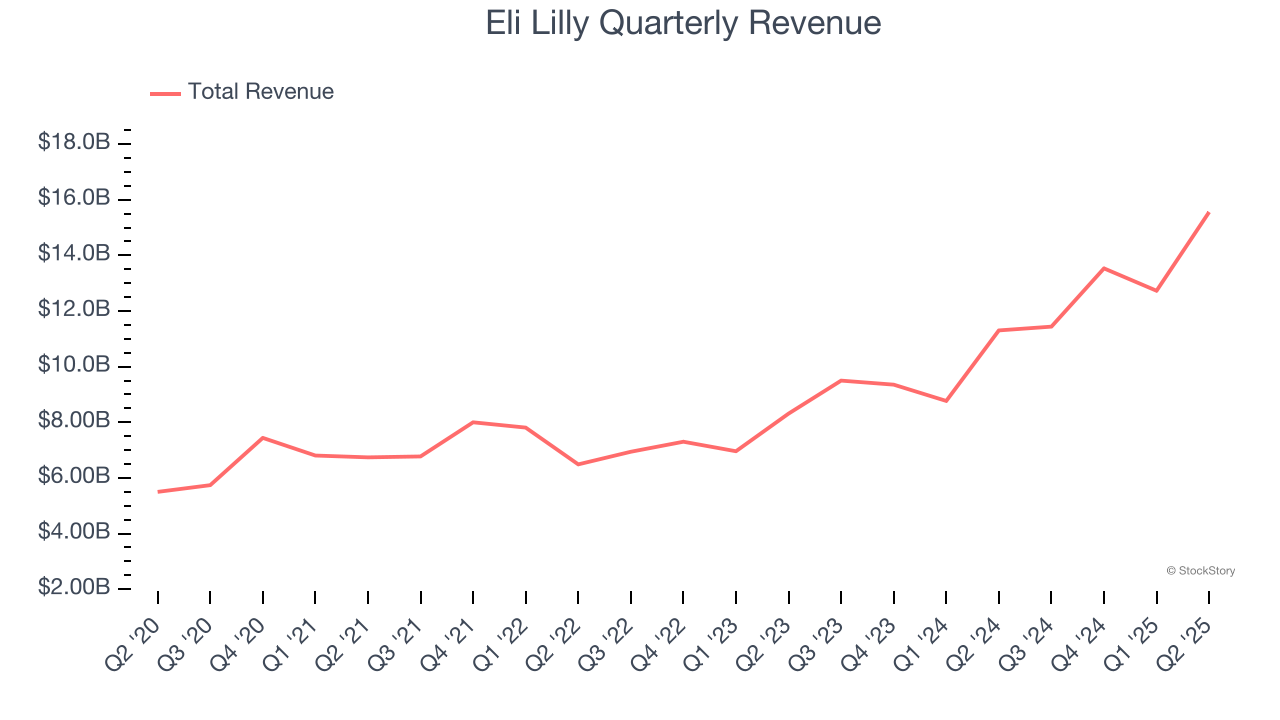

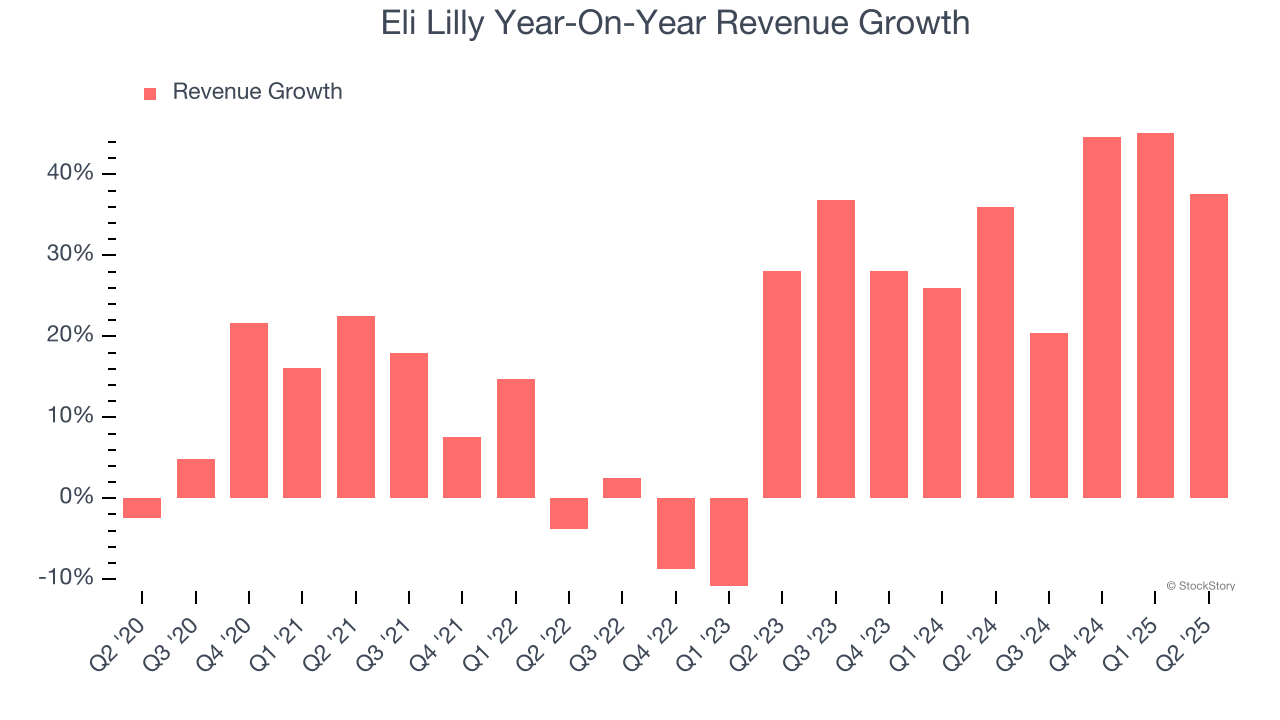

Global pharmaceutical company Eli Lilly (NYSE:LLY) reported revenue ahead of Wall Street’s expectations in Q2 CY2025, with sales up 37.6% year on year to $15.56 billion. The company’s full-year revenue guidance of $61 billion at the midpoint came in 1.5% above analysts’ estimates. Its non-GAAP profit of $6.31 per share was 12.9% above analysts’ consensus estimates.

Is now the time to buy Eli Lilly? Find out by accessing our full research report, it’s free.

"Lilly delivered another quarter of strong performance, achieving 38% year-over-year revenue growth driven by robust sales of Zepbound and Mounjaro and sustained momentum across our key medicines," said David A. Ricks, Lilly chair and CEO.

Founded in 1876 by a Civil War veteran and pharmacist frustrated with the poor quality of medicines, Eli Lilly (NYSE:LLY) discovers, develops, and manufactures pharmaceutical products for conditions including diabetes, obesity, cancer, immunological disorders, and neurological diseases.

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Eli Lilly’s 18.3% annualized revenue growth over the last five years was impressive. Its growth surpassed the average healthcare company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Eli Lilly’s annualized revenue growth of 34.3% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Eli Lilly reported wonderful year-on-year revenue growth of 37.6%, and its $15.56 billion of revenue exceeded Wall Street’s estimates by 5.4%.

Looking ahead, sell-side analysts expect revenue to grow 23.2% over the next 12 months, a deceleration versus the last two years. Still, this projection is eye-popping given its scale and suggests the market sees success for its products and services.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

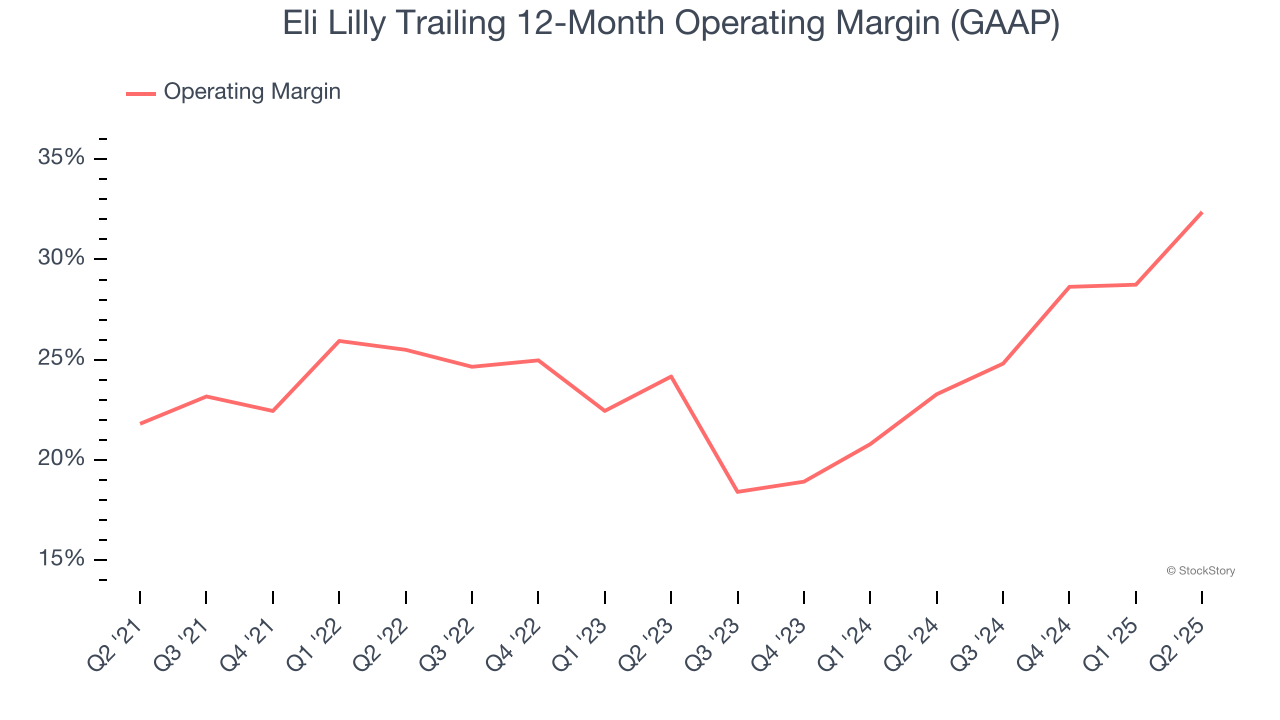

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Eli Lilly has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average operating margin of 26.3%.

Looking at the trend in its profitability, Eli Lilly’s operating margin rose by 10.6 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 8.2 percentage points on a two-year basis. These data points are very encouraging and show momentum is on its side.

This quarter, Eli Lilly generated an operating margin profit margin of 44.1%, up 11.3 percentage points year on year. This increase was a welcome development and shows it was more efficient.

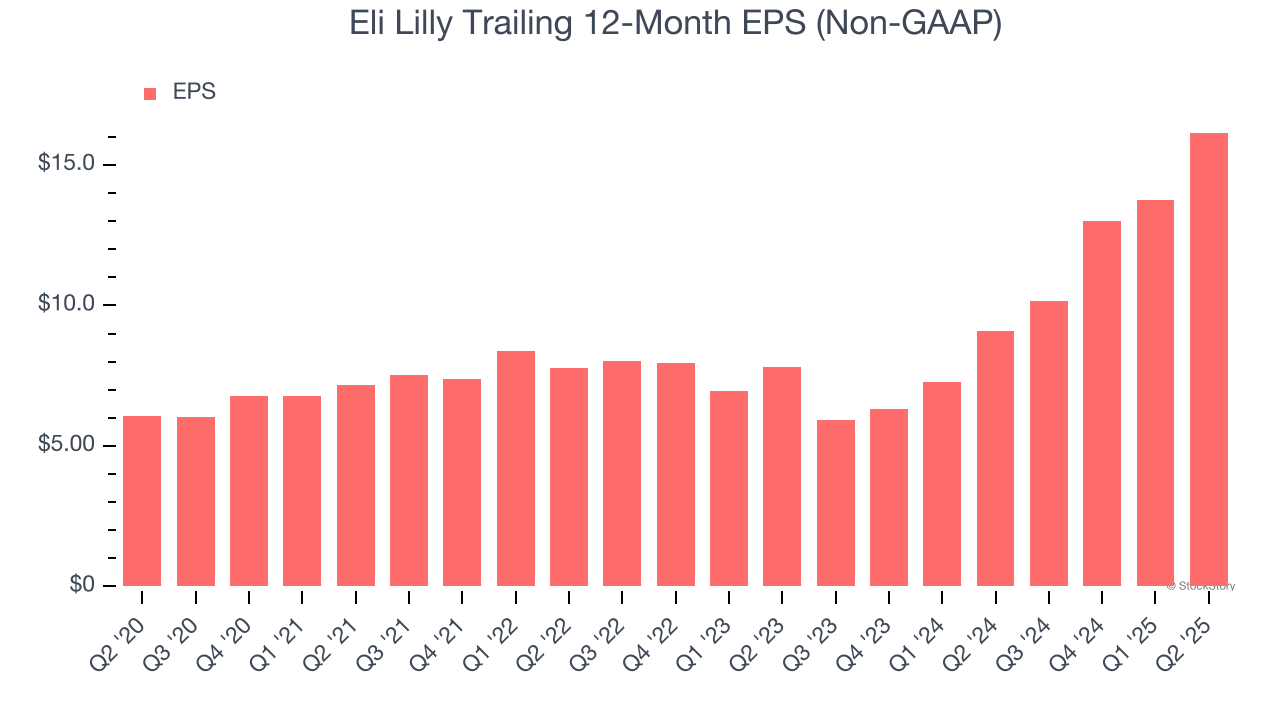

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Eli Lilly’s EPS grew at an astounding 21.6% compounded annual growth rate over the last five years, higher than its 18.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

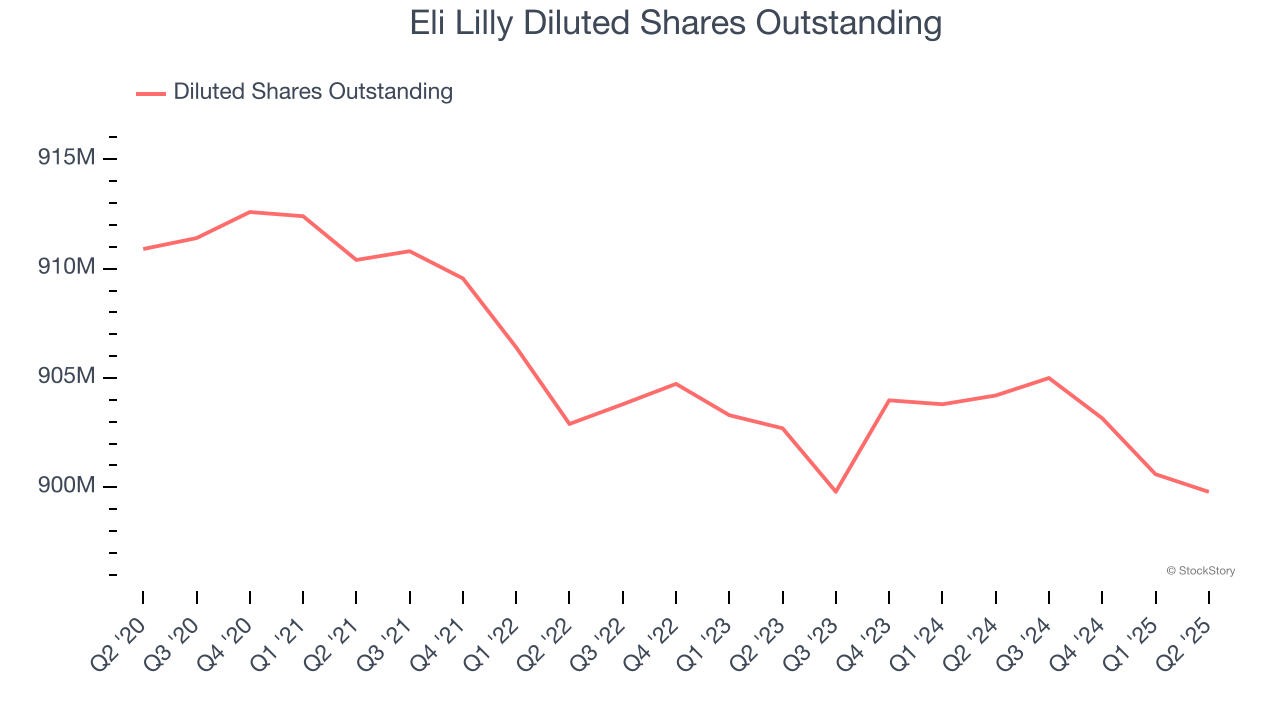

Diving into the nuances of Eli Lilly’s earnings can give us a better understanding of its performance. As we mentioned earlier, Eli Lilly’s operating margin expanded by 10.6 percentage points over the last five years. On top of that, its share count shrank by 1.2%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q2, Eli Lilly reported adjusted EPS at $6.31, up from $3.92 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Eli Lilly’s full-year EPS of $16.15 to grow 66.4%.

A strong quarter was overshadowed by orforglipron late-stage trial results. The highest dose of Eli Lilly's daily obesity pill helped patients lose almost 12% of their body weight, or roughly 27 pounds, at 72 weeks in a late-stage trial. This unfortunately underperformed expectations.

As for the quarter, we were impressed by how significantly Eli Lilly blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. Investors were likely hoping for more, and shares traded down 14.4% to $639.81 immediately after reporting.

Is Eli Lilly an attractive investment opportunity right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-21 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite