|

|

|

|

|||||

|

|

|

Since February 2025, Kohl's has been in a holding pattern, posting a small loss of 3.9% while floating around $11.35. The stock also fell short of the S&P 500’s 4.5% gain during that period.

Is there a buying opportunity in Kohl's, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

We don't have much confidence in Kohl's. Here are three reasons why you should be careful with KSS and a stock we'd rather own.

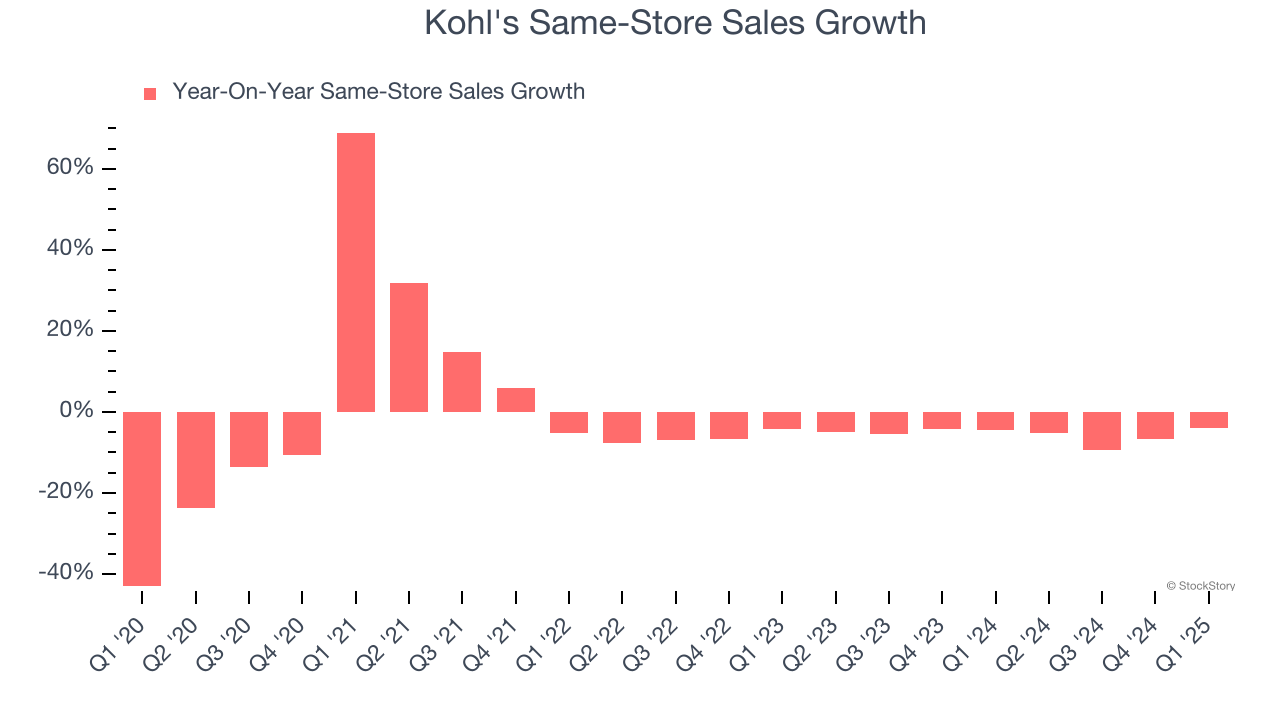

Same-store sales is an industry measure of whether revenue is growing at existing stores, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Kohl’s demand has been shrinking over the last two years as its same-store sales have averaged 5.5% annual declines.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Kohl’s revenue to drop by 5.2%, a decrease from This projection is underwhelming and implies its products will see some demand headwinds.

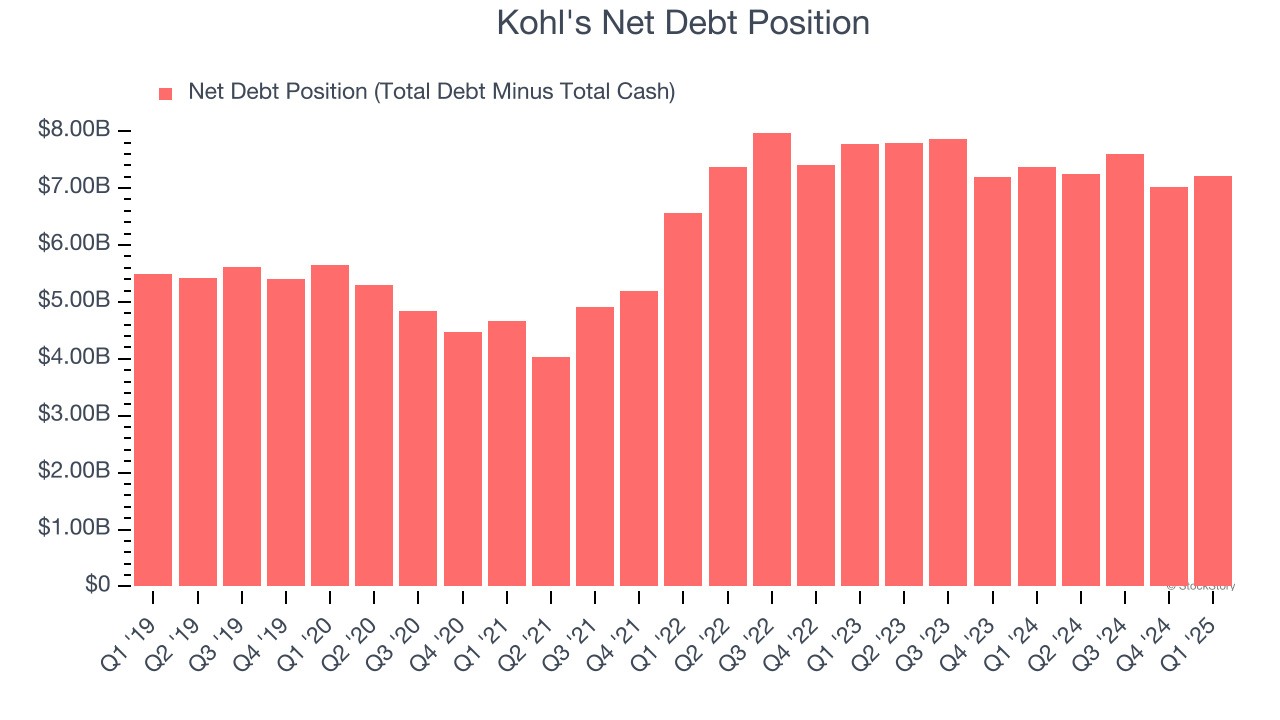

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

Kohl’s $7.37 billion of debt exceeds the $153 million of cash on its balance sheet. Furthermore, its 6× net-debt-to-EBITDA ratio (based on its EBITDA of $1.26 billion over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Kohl's could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Kohl's can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

Kohl's falls short of our quality standards. With its shares underperforming the market lately, the stock trades at 42.9× forward P/E (or $11.35 per share). At this valuation, there’s a lot of good news priced in - we think other companies feature superior fundamentals at the moment. Let us point you toward the Amazon and PayPal of Latin America.

Trump’s April 2024 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| 1 hour | |

| 9 hours | |

| Feb-20 | |

| Feb-19 | |

| Feb-18 | |

| Feb-17 | |

| Feb-16 | |

| Feb-13 | |

| Feb-11 | |

| Feb-11 | |

| Feb-09 | |

| Feb-09 | |

| Feb-09 | |

| Feb-03 | |

| Feb-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite