|

|

|

|

|||||

|

|

|

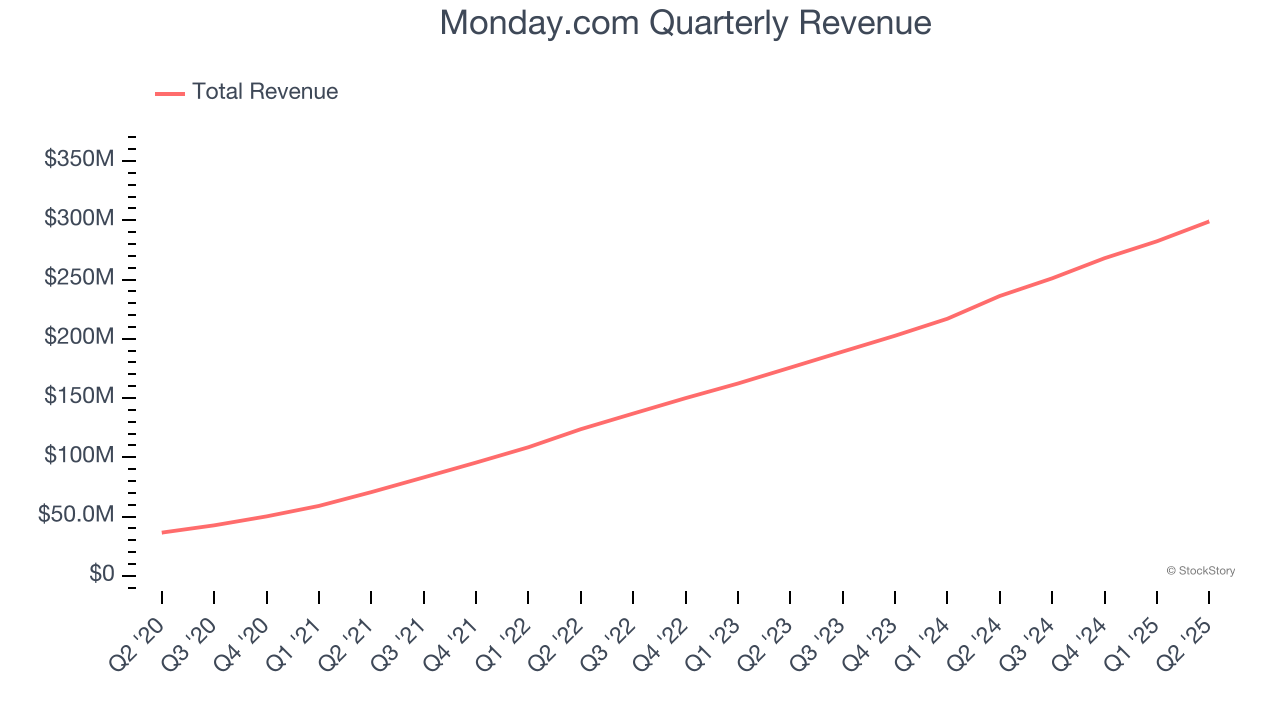

Project management software maker Monday.com (NASDAQ:MNDY) reported revenue ahead of Wall Street’s expectations in Q2 CY2025, with sales up 26.6% year on year to $299 million. The company expects next quarter’s revenue to be around $312 million, close to analysts’ estimates. Its non-GAAP profit of $1.09 per share was 27% above analysts’ consensus estimates.

Is now the time to buy Monday.com? Find out by accessing our full research report, it’s free.

“This quarter demonstrated our relentless focus on driving highly efficient growth at scale, and I’m energized by the momentum in our business and the opportunities we see ahead,” said Eliran Glazer, monday.com CFO.

Founded in 2014 and named after the dreaded first day of the work week, Monday.com (NASDAQ:MNDY) is a software-as-a-service platform that helps organizations plan and track work efficiently.

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Monday.com grew its sales at an exceptional 38.9% compounded annual growth rate. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, Monday.com reported robust year-on-year revenue growth of 26.6%, and its $299 million of revenue topped Wall Street estimates by 1.8%. Company management is currently guiding for a 24.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 23.6% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is healthy and implies the market is baking in success for its products and services.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

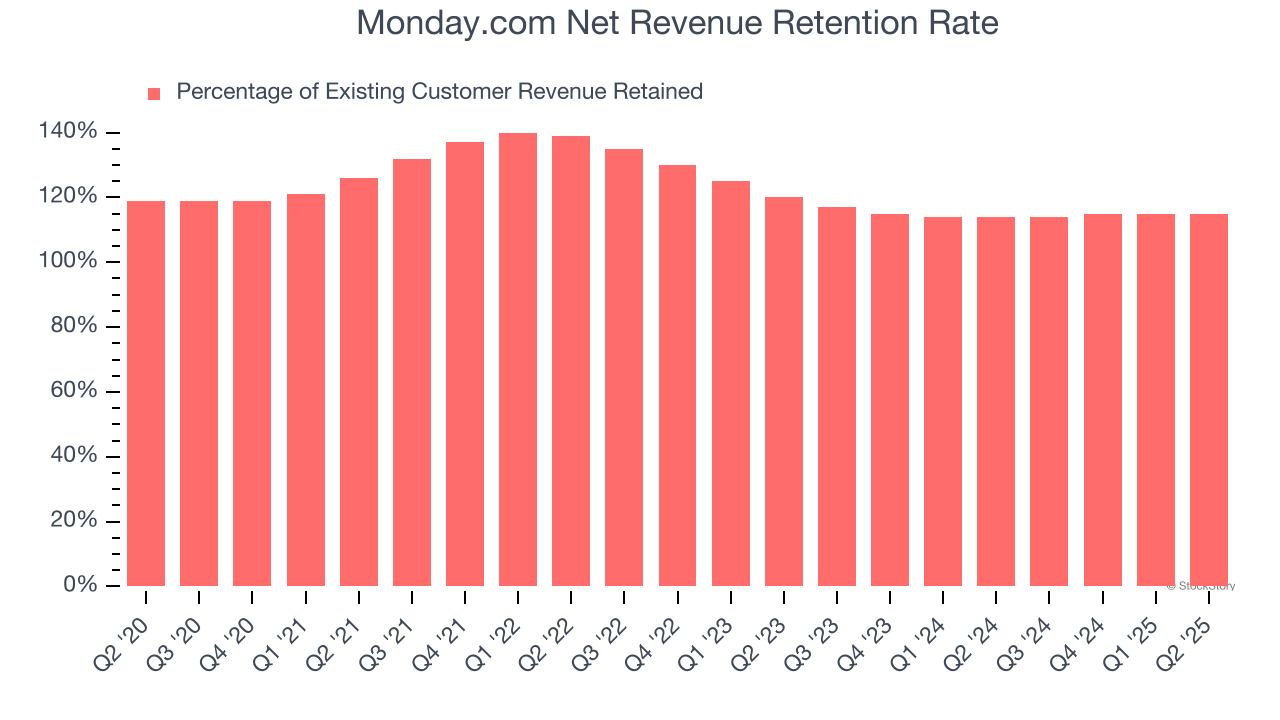

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Monday.com’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 115% in Q2. This means Monday.com would’ve grown its revenue by 14.7% even if it didn’t win any new customers over the last 12 months.

Monday.com has a good net retention rate, proving that customers are satisfied with its software and getting more value from it over time, which is always great to see.

It was encouraging to see Monday.com beat analysts’ revenue and operating profit expectations this quarter. On the other hand, its revenue guidance for next quarter missed slightly, which is weighing on shares. Overall, this quarter could have been better. The stock traded down 19% to $201 immediately following the results.

So do we think Monday.com is an attractive buy at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-16 | |

| Feb-16 | |

| Feb-15 | |

| Feb-14 | |

| Feb-13 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite