|

|

|

|

|||||

|

|

|

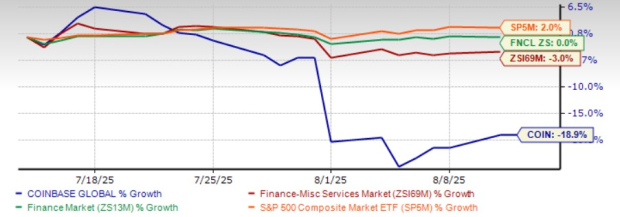

Shares of Coinbase Global Inc. COIN have lost 18.9% in the past month compared with the industry’s decline of 3%. In the meantime, the sector has risen 0.1% and the Zacks S&P 500 composite has gained 2%.

COIN, the crypto leader, is poised to benefit from listing a broader range of crypto assets and tokenized equities, international expansion and increased volatility. It is continually undertaking strategic growth initiatives like launching the Base app and CFTC-regulated perpetual futures contracts for Bitcoin and Ether, adding DEX trading to its app for U.S. users and joining traditional finance with crypto, among others, to tap the crypto boom. CEO Brian Armstrong envisions Coinbase to be the “everything exchange.”

COIN has been trading below its 50-day simple moving average (SMA), signaling a short-term bearish trend. The 50-day SMA is a key indicator for traders and analysts to identify support and resistance levels. It is considered particularly important as it is the first marker of an uptrend or downtrend.

Shares of Robinhood Markets HOOD and Interactive Brokers Group, Inc. IBKR, both crypto-oriented companies, have gained 514% and 126.5% in a month, respectively.

Robinhood has evolved from a brokerage firm mainly trading in digital assets to a more mature and diversified entity, striving to widen its market and reach. Robinhood continues to diversify its product base to acquire new clients and gain market share.

Interactive Brokers is known for its advanced electronic trading platforms and global market access. The company leverages proprietary systems to automate nearly every aspect of the brokerage process — from trade execution and risk management to compliance and customer onboarding —enabling it to operate with minimal human intervention and significantly lower costs than traditional brokers.

Coinbase, America’s largest registered crypto exchange, stands to gain from increased volatility and rising prices in the crypto asset market. Yet, in the second quarter of 2025, it suffered due to lower trading activity and subdued crypto volatility. COIN’s earnings missed expectations for the first time in the last 10 reported quarters.

Coinbase stands to gain from strengthened banking relationships, the securing of new licenses and the introduction of customized products for diverse customer segments. With a clear growth strategy, the company is increasing its market share in both the U.S. spot and derivatives markets, broadening its product suite and expanding its presence globally. A strong liquidity position enables continued strategic investments aimed at enhancing offerings and driving sustainable growth.

The accelerating adoption of stablecoins is poised to further boost revenues. Coinbase has posted positive EBITDA for eight consecutive quarters, supported by the durability of its subscription-based model. Dedicated to bringing crypto utility to a global audience, the company aspires to onboard more than a billion people into the crypto economy. To advance this goal, it is channeling significant investment into core infrastructure and platforms, including Layer 2 technologies, its Base network and stablecoin development.

Coinbase is a fundamentally strong company. It ended 2024 with $9.3 billion in resources, which is defined as cash & cash equivalents and USDC, up $3.8 billion year over year. Debt has been decreasing over the past several quarters, while the total debt capital ratio has been improving. Also, its higher times interest earned implies that the company can comfortably service its debt. However, Coinbase recently priced $2.6 billion convertible notes, which increases concerns about dilution and financial leverage.

COIN’s return on equity in the trailing 12 months was 16%, lower than the industry average of 16.4%.

The return on invested capital in the trailing 12 months was 10.2%, which compared favorably with the industry average of 4.9%. This reflects the insurer’s efficiency in utilizing funds to generate income.

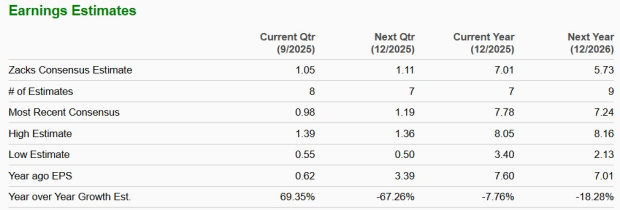

The Zacks Consensus Estimate for 2025 earnings has moved 93.6% north but the same for 2026 has moved 7.4% south in the past 30 days.

The Zacks Consensus Estimate for 2025 and 2026 earnings suggests a 7.8% and 18.3% year-over-year decrease, respectively. It carries a Growth Score of F.

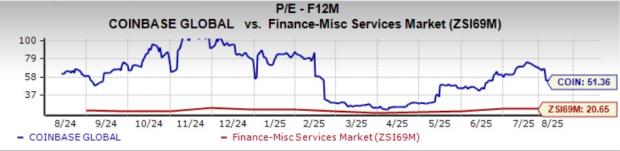

Coinbase shares are trading at a premium to the industry. Its 12-month forward price-to-earnings of 51.36X is much higher than the industry average of 20.65X. Its Value Score of F indicates a stretched valuation at this moment.

Shares of Robinhood Markets and Interactive Brokers are also trading at multiples higher than the industry average.

Coinbase’s efforts to accelerate growth in the crypto market, increase market share in spot trading on consumer and institutional trading platforms and improve trading experience, along with continued innovation, should help it accelerate growth.

However, crypto asset price risk and lower volatility could adversely impact Coinbase’s operating results. A decline in the market price of Bitcoin, Ethereum and other crypto assets could hurt earnings, the carrying value of crypto assets and future cash flows. This may also affect liquidity and the company’s ability to meet ongoing obligations.

Also, a premium valuation, price erosion, unfavorable ROE, decline in earnings estimates for the current as well as next year, mixed analyst sentiment and a VGM Score of F keep us wary on this Zacks Rank #4 (Sell) stock presently.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 8 hours | |

| 13 hours | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite