|

|

|

|

|||||

|

|

|

Broadcom's custom AI accelerators are a great alternative to GPUs for AI hyperscalers.

Management sees a massive growth rate over the next few years for this product line.

Even with the chipmaker's strong growth outlook, its stock is still quite expensive.

Nvidia (NASDAQ: NVDA) and its GPUs have become the industry standard in AI computing power. You'd be hard-pressed to find any serious AI competitor that isn't using Nvidia GPUs, but other options are emerging. Now that most companies know what AI workloads will look like, the flexibility of a GPU isn't necessarily needed, which allows AI hyperscalers to design a chip specifically around a certain workload.

These computing units are known as AI accelerators, and Broadcom (NASDAQ: AVGO) is one of the primary partners that AI hyperscalers use to develop them. Broadcom's business looks poised to rapidly expand over the next few years thanks to increasing demand for these specialized computing units. But will that make it the next Nvidia?

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Image source: Getty Images.

Broadcom hasn't become a household name like Nvidia, although it's still a giant. Broadcom's market capitalization is around $1.4 trillion, making it the seventh-largest company listed on a U.S. exchange. That's about one-third the size of Nvidia, showcasing that it's already a tech giant.

The chipmaker has multiple product offerings ranging from cybersecurity to mainframe hardware to virtual desktop software via its VMware acquisition. Still, the most important part of the Broadcom investment thesis centers around custom AI accelerators and connectivity switches.

Starting with connectivity switches, these devices connect GPUs and XPUs (Broadcom's typical acronym when referring to custom AI accelerators) in a data center. These switches are critical and allow workloads to be distributed across different computing clusters and then stitched back together to form an answer. Without these switches, AI data centers with hundreds of thousands of GPUs would be significantly less effective.

Moving to its custom AI accelerators or XPUs, Broadcom believes that there is a serviceable addressable market between $60 billion and $90 billion that will emerge by 2027 from just three customers. Broadcom also has four other customers working on their XPU designs with the company, so this potential market could dramatically expand.

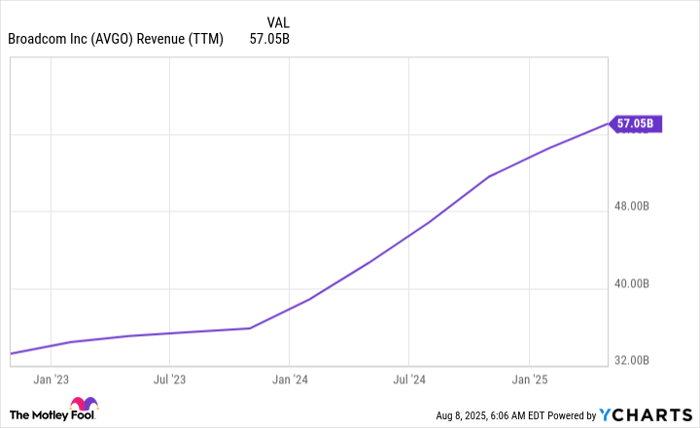

Considering Broadcom's trailing-12-month revenue was just shy of $60 billion, and its AI revenue was $4.1 billion in Q1, this could be a huge growth factor in the coming years.

AVGO Revenue (TTM) data by YCharts

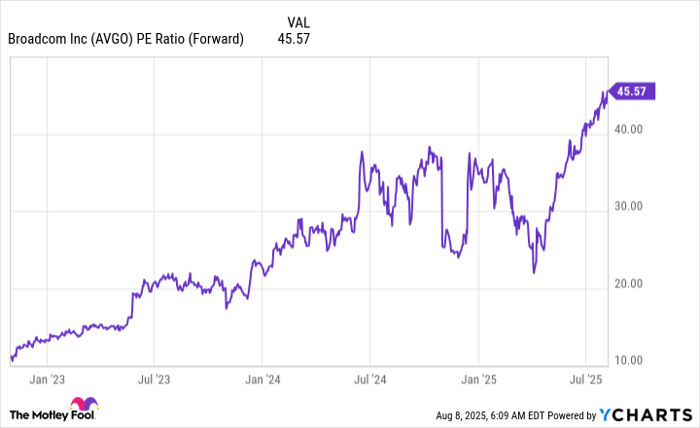

But does all this make Broadcom a buy right now? The market isn't blind to the fact that Broadcom's growth opportunity over the next few years is massive. It's well aware of its potential, which is why the stock has a premium valuation attached to it. Broadcom's stock trades for more than 45 times forward earnings, which is more expensive than Nvidia's 42 times forward earnings valuation.

AVGO PE Ratio (Forward) data by YCharts

While Broadcom may have projections of rapid growth, Nvidia is currently outperforming it in this department, with its revenue rising 69% in its latest quarter versus Broadcom's 20%. So, Broadcom's premium valuation over Nvidia doesn't make a ton of sense right now.

It will need to deliver some serious growth numbers to justify its current price tag, especially if it wants to outperform Nvidia over the long run. While I believe that Broadcom will have immense success with its custom AI accelerators, the price tag is too expensive to justify buying shares over Nvidia.

I want Broadcom to show me that this AI accelerator growth is real and following along the trajectory management laid out. If it can do that, then Broadcom could be a compelling investment. But right now, it's just a bit too expensive to purchase shares versus Nvidia.

Before you buy stock in Broadcom, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Broadcom wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $660,783!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,122,682!*

Now, it’s worth noting Stock Advisor’s total average return is 1,069% — a market-crushing outperformance compared to 184% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 13, 2025

Keithen Drury has positions in Broadcom and Nvidia. The Motley Fool has positions in and recommends Nvidia. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-13 | |

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite