|

|

|

|

|||||

|

|

|

Last quarter's results were healthy enough, but Q3 guidance disappointed.

Twilio's foray into the artificial intelligence arena is quite promising.

But risk-tolerant investors will want to brace for above-average volatility.

With the stock down more than 20% just since Thursday's release of its second-quarter results, it would be easy to presume the worst of customer-communications technology company Twilio (NYSE: TWLO). That's a pretty big setback in a short period of time, after all, in an environment that's otherwise been mostly bullish.

Perhaps investors are right to steer clear. Or, maybe the market's choosing to come to the wrong conclusion about Twilio's profit guidance. Maybe this steep sell-off is a buying opportunity -- at least, for a particular kind of investor. Let's have a closer look.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

It's possible that you've heard of Twilio but don't know exactly what it is. In simplest terms, it helps companies automate their digital communications with consumers and customers. From text messaging to call center management to customer-identity verification, Twilio's solutions have become very relevant in the modern mobile era.

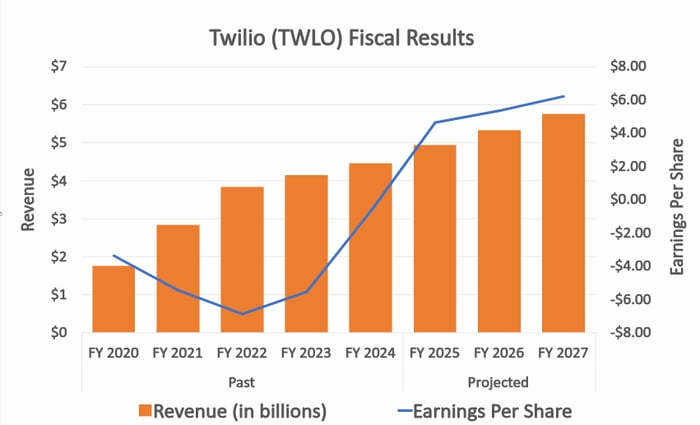

Nearly 350,000 active customers, including Uber Technologies, Shopify, and IBM, collectively contributed $1.23 billion in revenue last quarter, up 13% year over year. That top-line growth helped improve the year-ago Q2 non-GAAP operating income from $175.3 million to $220.5 million this time around.

Things seem to be slowing down, though. The company's revenue guidance for the quarter currently underway only calls for organic sales growth of between 8% and 9%, while its per-share earnings of between $1.01 and $1.06 fell short of the consensus estimate of $1.10. Investors panicked, and understandably so.

Now, they need to take a step back and look at the bigger picture. Yes, Twilio's third-quarter earnings guidance was disappointing. Its full-year outlook wasn't a whole lot better, either. It's possible, though, that the company is understating its near-term and even long-term potential upside.

The world didn't quite recognize it at the time, but Twilio's earliest tech (the company launched in 2008, for reference) was a rudimentary kind of artificial intelligence. That original technology is comically weak compared to far more modern AI solutions like ChatGPT or one of Palantir Technologies' platforms. At the time, though, it was pretty good, creating the premise that digital interactions with customers could be automated for the sake of efficiency and accuracy.

Image source: Getty Images.

Now the company is overhauling its solutions with modern-day artificial intelligence. For instance, in May, Twilio unveiled a solution it calls Conversational Intelligence. This platform aggregates and analyzes a particular consumer's entire communication history with an organization, turning it into concise actionable insight for a live customer service representative, or even for an AI-powered virtual customer service agent.

One aspect of Conversational Intelligence is particularly impressive. That's ConversationRelay, which allows developers to monitor and adapt a voice-based AI agent "on the fly" based on its performance with live customers. The end results of all of these new solutions are lower costs and increased revenue.

The opportunity is enormous. Outlooks from Precedence Research, SkyQuest Technology, and Market.us all agree that the worldwide AI-powered customer service agent market is set to grow at an average annual pace of more than 40% over the course of the next several years.

No other outfit is quite as well-positioned to capture its share of this growth as Twilio, in that it's already so well-established within this customer-communications technology space.

But the lackluster third-quarter profit guidance? Sure, that's a legitimate concern. Except maybe it isn't.

Yes, Twilio's expected per-share earnings of between $1.01 and $1.06 were shy of analysts' expectation of $1.10. Don't lose perspective, though. That's still better than 2024's Q3 bottom line of $1.02. Let's also not forget that this company is in the habit of topping analysts' quarterly earnings estimates, having only missed them once since 2021. Odds are good that it will be able to continue doing so into the foreseeable future.

Data source: StockAnalysis.com. Chart by author.

Arguably, any profit-margin pressure Twilio may be experiencing in the immediate future reflects an investment in artificial intelligence tools or marketing that will ultimately help it grow even more than it was apt to just a year ago. That's an expense that most investors would be OK with if they could just look past the headlines about its disappointing Q3 earnings guidance.

They eventually will, of course, turning this exaggerated dip into a fantastic buying opportunity. The pros think so, anyway. Analysts' current consensus target of $130.79 is 36% above the stock's present price. Most of these analysts also currently rate Twilio shares as a strong buy. Several of them doubled down on their bullishness following the release of the company's Q2 numbers, while a handful of them even raised their targets, citing the progress already seen with its AI-powered initiatives.

Just be sure you're able to stomach the volatility that's sure to linger while the market figures out what it thinks of Twilio now following its post-earnings tumble.

Before you buy stock in Twilio, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Twilio wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $660,783!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,122,682!*

Now, it’s worth noting Stock Advisor’s total average return is 1,069% — a market-crushing outperformance compared to 184% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 13, 2025

James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends International Business Machines, Palantir Technologies, Shopify, Twilio, and Uber Technologies. The Motley Fool has a disclosure policy.

| Mar-07 | |

| Mar-06 | |

| Mar-05 | |

| Mar-04 | |

| Mar-04 | |

| Mar-02 | |

| Mar-02 | |

| Mar-02 | |

| Mar-02 | |

| Mar-01 | |

| Mar-01 | |

| Feb-28 | |

| Feb-26 | |

| Feb-20 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite