|

|

|

|

|||||

|

|

|

Nine American companies are in the exclusive trillion-dollar club, but only three have achieved a valuation of $3 trillion.

Amazon's earnings are soaring thanks to its booming cloud business and its efforts to drive efficiency in its e-commerce segment.

Amazon has a clear pathway to the $3 trillion club by 2027, but it could get there even sooner.

There are nine American companies with valuations of $1 trillion or more right now, but only three have crossed the $3 trillion milestone:

Amazon (NASDAQ: AMZN) could be set to join that ultra-exclusive club thanks to its soaring earnings growth, and its expanding use of artificial intelligence (AI) across its cloud computing and e-commerce businesses. The company's market capitalization is $2.36 trillion as of this writing (Aug. 12), so its stock would have to climb by 27% to reach the $3 trillion milestone. Here's why I think that's likely to happen within the next two years.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Image source: Getty Images.

Amazon Web Services (AWS) is the world's largest cloud computing platform. It offers hundreds of solutions to help businesses navigate the digital age, whether they need simple tools like data storage and website hosting, or more complex tools to build software applications. But AWS also offers a growing portfolio of products and services to help businesses develop and deploy AI.

AWS designed its own data center chips for AI training and inference workloads, the latest of which is called Trainium 2. It offers up to 40% better price performance than competing chips, which is why it has become a key part of the hardware stack for top AI developers like Anthropic. Amazon says that demand continues to exceed supply for computing capacity, which should drive strong Trainium 2 sales for the foreseeable future.

AWS also offers a growing list of ready-made large language models (LLMs) through its Bedrock platform, which developers can use to supercharge their AI software projects. Among them is the Nova foundation model Amazon designed in-house, which has become the second most popular option on Bedrock thanks to its highly customizable nature. For example, developers can pre-train Nova with additional unlabeled data to extend its capabilities, which isn't possible with models from third parties like Anthropic.

AWS generated a record $30.8 billion in revenue during the second quarter of 2025 (ended June 30), which was only a fraction of Amazon's total revenue of $167.7 billion. However, AWS revenue increased by 17% year over year, making it one of the fastest-growing parts of the entire organization.

In a series of comments to shareholders on July 31, Amazon CEO Andy Jassy said that the AI business within AWS was generating revenue at a multi-billion-dollar annual run rate, with triple-digit percentage growth year over year.

AWS might have accounted for a minority of Amazon's revenue during Q2, but it was responsible for 57% of the company's $37.5 billion in operating income. In other words, it's the profit engine behind the entire organization. The retail business is Amazon's single largest source of revenue, but its profit margins are razor-thin, so its contribution to operating income is relatively small in comparison.

Amazon is improving efficiency to increase the retail segment's profitability. It divided its U.S. logistics network into eight regions in 2023, and the products in its fulfillment centers are now specific to each geographic area. As a result, orders travel shorter distances and reach customers much faster, which reduces costs. During Q2, the average travel distance for each package fell by 12% year over year, and the number of touches per package declined by 15%.

The company is also investing in AI across the retail business. It developed a tool called Project Private Investigator for its fulfillment centers, which uses AI and computer vision to identify defective products before they are shipped to customers, reducing the rate of returns. It also built an AI shopping assistant for Amazon.com called Rufus, which helps customers compare products and make faster purchase decisions.

These efforts have contributed to a surge in Amazon's profits. The company generated $1.68 in earnings per share (EPS) during Q2, which was a 33% increase from the year-ago period. The result was also 26% higher than Wall Street's consensus estimate, which followed a 17% beat in the first quarter.

This is becoming a habit for Amazon, because it also crushed Wall Street's quarterly earnings expectations by 23% throughout 2024.

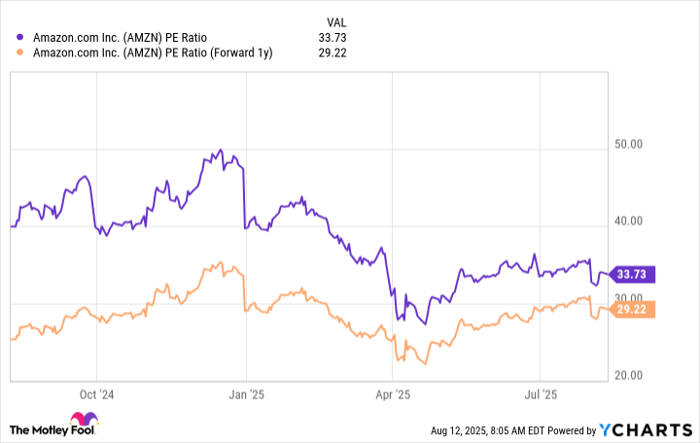

Based on Amazon's trailing 12-month EPS of $6.55, its stock is trading at a price-to-earnings (P/E) ratio of 33.7, which is a slight premium to the 32.9 P/E of the Nasdaq-100 technology index. In other words, you could argue that Amazon stock is roughly at fair value relative to its big-tech peers.

If we look ahead, Wall Street's consensus estimate (provided by Yahoo! Finance) suggests that Amazon could generate $7.54 in EPS during 2026, which places its stock at a forward P/E ratio of 29.2. That means the stock would have to climb by 15.4% over the next 18 months just to maintain its current P/E ratio of 33.7, which would place its market capitalization at over $2.72 trillion.

Data by YCharts.

By that stage, Amazon would have to grow its annualized EPS by another 10.3% to justify a $3 trillion valuation, which should be possible in 2027 if recent history is any guide. But there are a couple of things to consider:

Based on those points, I think there is a clear path for Amazon to join the $3 trillion club next year.

Before you buy stock in Amazon, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $649,544!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,113,059!*

Now, it’s worth noting Stock Advisor’s total average return is 1,062% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 13, 2025

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Apple, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 12 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours |

US filings for jobless aid rise modestly to 212,000 as layoffs remain at historically healthy levels

AMZN

Associated Press Finance

|

| 3 hours | |

| 3 hours | |

| 4 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite