|

|

|

|

|||||

|

|

|

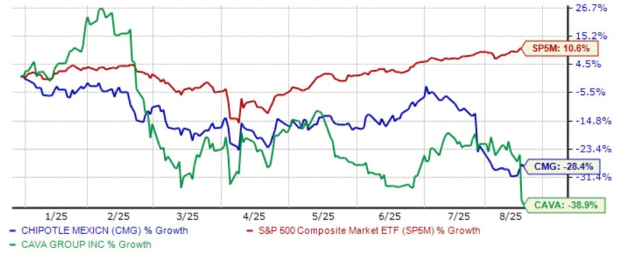

A notable restaurant duo, Chipotle Mexican Grill CMG and CAVA Group CAVA, both faced pressure following the release of their quarterly results, adding fuel to the already-poor share performance from each in 2025.

With both stocks coming well off all-time highs, it raises a valid question – what’s the better pick moving forward? Let’s take a closer look.

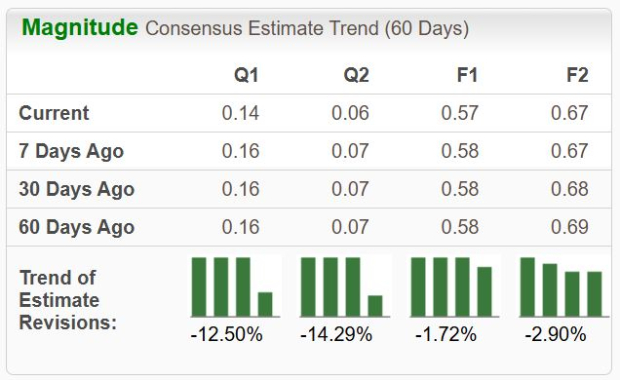

CAVA posted mixed results relative to our consensus estimates, exceeding the Zacks Consensus EPS estimate by 23% but falling short of sales expectation by nearly 3%. Sales were up 20% YoY, whereas earnings were down 15% from the year-ago period.

While the sales growth is undoubtedly strong, it was primarily driven by the opening of new locations, with CAVA opening 16 new restaurants throughout the period. But what investors didn’t like was comparable restaurant sales growth of 2.1%, a far cry from the 10.8% mark in the prior quarter. CAVA’s restaurant operating margin also totaled 26.3%, down from the 26.5% mark a year-ago.

Further, comparable restaurant sales growth of 2.1% primarily came from higher menu prices, with guess traffic being roughly flat. CAVA trimmed guidance across several metrics, most notably comparable restaurant sales growth, now expecting growth in a band of 4 – 6% compared to 6 – 8% prior for its FY25.

The slowing growth in its existing locations paired with decreased traffic helps explain the poor share reaction post-earnings, with analysts also recalculating their EPS and sales expectations following the print and downwardly revised guidance. The stock is currently a Zacks Rank #4 (Sell).

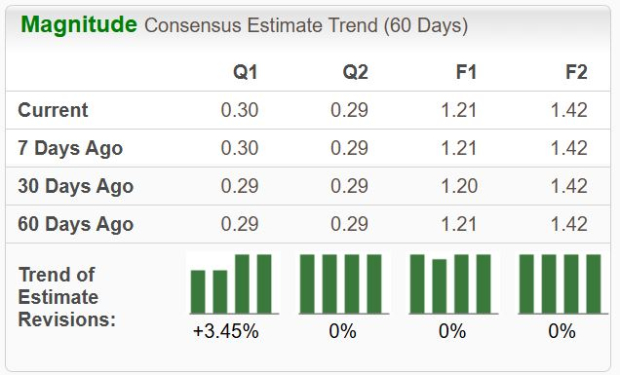

CMG’s results were similarly mixed concerning our consensus expectations, with the company posting a 3% EPS beat while falling short of sales expectations by roughly 1.2%. Sales were up 3% year-over-year, whereas earnings fell 3% from the year-ago period.

Notably, comparable restaurant sales fell 4% year-over-year. The company also trimmed its FY25 comparable restaurant sales growth guidance to flat year-over-year, which compares to a previously anticipated low-single-digit range.

Like CAVA, the company’s existing restaurants also faced a profitability crunch, with its restaurant level operating margin contracting to 27.4% vs. 28.9% in the year-ago period. Analysts haven’t had the same bearish reaction post-earnings concerning their revisions, with expectations for CMG largely remaining stable post-earnings and even increasing for its next release.

CMG is currently a Zacks Rank #3 (Hold).

While Chipotle Mexican Grill CMG and CAVA Group CAVA both reflect intriguing options for restaurant exposure, the reality remains that they’ve faced considerable share pressure from weak quarterly results that have revealed slowing growth.

Concerning the valuation picture, CAVA’s trading at a premium to CMG, with CMG’s restaurant margins just as strong (and with a history of consistency) while its EPS outlook also remains much more constructive.

The Zacks Rank #4 (Sell) rating on CAVA reflects a tough near-term outlook concerning share performance, whereas a largely-stable EPS picture for CMG keeps it a Zacks Rank #3 (Hold).

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| 6 hours | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite