|

|

|

|

|||||

|

|

|

CrowdStrike CRWD and Qualys QLYS are both U.S.-based cybersecurity companies that specialize in protecting enterprises from evolving digital threats. While Qualys serves a niche space involving vulnerability management and compliance monitoring, CrowdStrike specializes in endpoint protection and extended detection and response (XDR), offering AI-native cloud security through its Falcon platform. Their shared emphasis on AI-enhanced cybersecurity positions them as key players in the evolving digital security landscape.

CrowdStrike and Qualys are capitalizing on the massive growth of the cybersecurity space, fueled by the rise of complex attacks, including credential theft and abuse, remote desktop protocol attacks and social engineering-based initial access. Per a Mordor Intelligence report, the cybersecurity market is projected to witness a CAGR of 12.63% from 2025 to 2030.

With this robust industry growth forecast, the question remains: Which stock has more upside potential? Let us break down their fundamentals, growth prospects, market challenges and valuation to determine which offers a more compelling investment case.

CrowdStrike provides its cybersecurity services mainly through its Falcon platform. CrowdStrike’s Falcon platform is renowned for being the industry’s first multi-tenant, cloud native, intelligent security solution. The Falcon platform helps in securing workloads across on-premise, cloud-based and virtualized environments running on several endpoints, such as desktops, laptops, servers, virtual machines and IoT devices.

CRWD’s cloud-based Falcon platform currently provides 29 cloud modules via a SaaS subscription model that is categorised under three categories — Endpoint Security, Security & IT Operations, and Threat Intelligence. The share of subscription-based sales to CrowdStrike’s total revenues grew from 72% in fiscal 2017 to 95% in fiscal 2025.

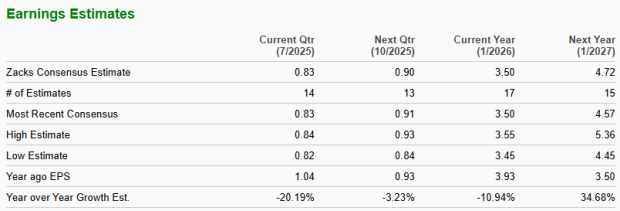

However, CrowdStrike’s recent quarterly reports have shown a deceleration in its growth rate. The company's revenue growth, while still robust, is not as explosive as in previous years. CrowdStrike had enjoyed more than 35% year-over-year top-line growth till fiscal 2024; the growth rate decelerated in fiscal 2025 to 29%. The current Zacks Consensus Estimate for fiscal 2026 and 2027 suggests that the top-line growth will further decelerate to around 21%.

Moreover, CrowdStrike’s rising costs are a cause of key concern. Over the last six fiscals, CrowdStrike’s Research & Development (R&D) expenses increased 12-fold, while Sales & Marketing (S&M) expenses have increased nearly ninefold to $1.52 billion in fiscal 2025 from $173 million in fiscal 2019. Additionally, in the first quarter of fiscal 2026, S&M and R&D expenses soared 25.5% and 34.7%, respectively, year over year.

Though the firm foresees these investments to generate benefits over the long run, higher expenses are weighing on the company’s bottom-line results. The Zacks Consensus Estimate for CrowdStrike’s fiscal 2026 earnings indicates a year-over-year decline of 10.9%.

Qualys is the leading provider of Vulnerability Management, Detection and Response (VMDR) solutions, and has been witnessing increased VMDR customer penetration for the past several quarters. Qualys continues to expand its customer base, with customers spending more than $500,000 annually, increasing 7% year over year to 212 in the second quarter of 2025. Also, its net dollar retention rate improved to 104% from 103% in the previous quarter.

Qualys has increased the depth of its portfolio with multiple product launches and enhancements, including the industry’s first Risk Operations Center with Enterprise TruRisk Management. Qualys also expanded its TotalAI solution with advanced AI security capabilities to extend threat coverage, provide multi-modal protections, and enable internal Large Language Model scanning to help organizations secure their Machine Learning Operations pipeline.

Qualys’ channel partner program, which involves expanding its cloud-based security solutions through a network of partners, including Managed Service Provider, Managed Security Service Provider and Value-Added Resellers, has been able to increase its revenues much faster than direct customers. In the second quarter of fiscal 2025, channel revenues grew 17% year over year compared with 4% growth from direct customers.

Qualys is expanding globally with an international revenue growth rate of 15% year over year, representing 43% of total revenues in the latest quarter. This organic expansion is enabling it to gain more customers and market share without acquisition costs.

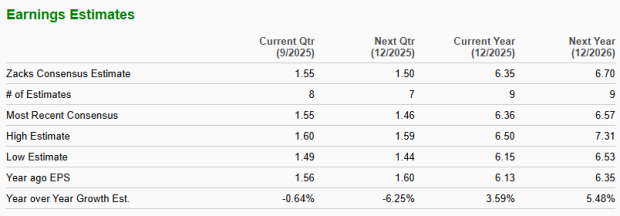

These factors are driving growth in Qualys’ top and bottom lines. The Zacks Consensus Estimate for Qualys’ 2025 earnings is pegged at $6.35 per share, indicating a year-over-year increase of 3.6%.

Year to date, CrowdStrike shares have appreciated 25.1%, while Qualys shares have plunged 7.9%.

Qualys is trading at a forward sales multiple of 6.82X, below the security industry’s 11.97X. CrowdStrike is trading at a forward sales multiple of 19.98X, indicating its overvaluation at present.

Both CrowdStrike and Qualys are key players in the cybersecurity space, but CrowdStrike is still navigating the headwinds emerging from slowing sales growth, rising expenses and shrinking profit margin. Additionally, Qualys is trading at a discount in comparison to CrowdStrike stock, making the stock more attractive at present.

Currently, Qualys flaunts a Zacks Rank #1 (Strong Buy), making the stock a must-pick compared to CrowdStrike, which has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-30 | |

| Mar-30 | |

| Mar-30 | |

| Mar-30 | |

| Mar-30 | |

| Mar-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite