|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Toast, Inc. (TOST) is making significant strides in its long-term growth strategy. The company has announced a robust outlook for 2025, projecting 29% year-over-year growth in fintech and subscription gross profit (higher than its prior 25–27% growth outlook). This momentum is being fueled by its strategy to expand in U.S. SMB restaurants as well as penetrate new markets. Its recent international expansion into Australia and a newly forged partnership with American Express (AXP), or AMEX, highlight its potential to solidify its foothold in restaurant technology and financial services globally.

The Australia launch marks Toast’s fourth international market, expanding into new customer segments across enterprise, global and food and beverage retail. Toast onboarded its first customer, Graze Craze, as part of this initiative. Already a U.S. customer, Graze Craze chose Toast over a local POS system provider. It now uses Toast’s guest displays, kitchen screens and online ordering, with plans to add marketing, loyalty and multi-location tools to support its expansion in Australia.

Another major move shaping Toast’s 2025 outlook is its strategic partnership with American Express. The collaboration aims to improve the dining experience for restaurants and diners across Resy, Tock and Toast locations in the United States, while creating new revenue streams for the company. The partnership intends to combine Resy and Tock’s guest tools with Toast’s Digital Chits to provide staff with customer insights during service. It will also explore new benefits for guests and AMEX Card Members, and increase visibility for restaurants, wineries, cafes and bars through the Local by Toast app.

Toast, Inc. price-consensus-chart | Toast, Inc. Quote

Toast is gaining share across SMB markets, even in metros with more than 30% penetration, showing its local go-to-market strategy is working. Net adds in 2025 are expected to exceed 2024’s total.

In the last reported quarter, the company served 148,000 locations, marking a 24% increase year over year, and exceeded 10,000 sites across international markets, enterprise customers and food and beverage retail. Total fintech and subscription gross profit increased 35% year over year to $464 million. For the third quarter, Toast expects $465–$475 million in subscription and fintech gross profit, implying 23–26% growth, and adjusted EBITDA of $140–$150 million.

While the outlook is encouraging, Toast faces intense competition from local POS providers as well as other powerhouse software providers like Block (XYZ) and Oracle (ORCL).

Tech giant Oracle offers a wide range of products, including POS systems like Oracle Retail Xstore and Oracle MICROS Simphony POS. MICROS Simphony targets large restaurant chains, hotels, casinos and resorts. As a unified cloud-based POS platform, it enables restaurant owners to efficiently manage both online and on-premise operations in real-time from any device. It provides exceptional hospitality from arrival to departure and beyond, using advanced POS and property management solutions.

Oracle’s revenues rose 11% in USD and cc year over year to $15.9 billion, driven by continued momentum from its Oracle Cloud Infrastructure business, including winning cloud-computing contracts from AI-focused startups. It provided robust guidance for fiscal 2026, expressing strong confidence in accelerating growth rates. Total company revenues are expected to reach at least $67 billion, representing 16% growth in cc and exceeding its previous guidance by more than $1 billion.

Block, formerly known as Square, offers financial and marketing services through its comprehensive commerce ecosystem that helps sellers start, run and grow their businesses. Block’s Square for Restaurants POS platform competes directly with TOST’s offerings. The company’s strategic priorities have shifted to strengthening customer engagement, launching new products and scaling go-to-market efforts, with clearer goals set for both user and revenue growth.

Management increased its full-year 2025 outlook. XYZ expects full-year gross profit of $10.17 billion, suggesting more than 14% year-over-year growth, and adjusted operating income of $2.03 billion, representing a 20% margin with a 2-point improvement from last year.

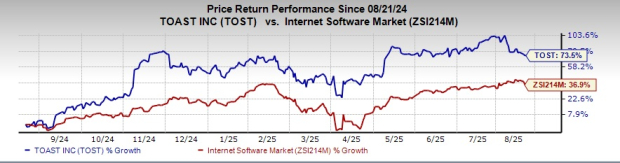

Shares of TOST have gained 73.5% in the past year compared with the Zacks Internet-Software industry's growth of 36.9%.

From a valuation standpoint, TOST trades at a forward price-to-sales of 4.6X, lower than the industry’s average of 7.28X.

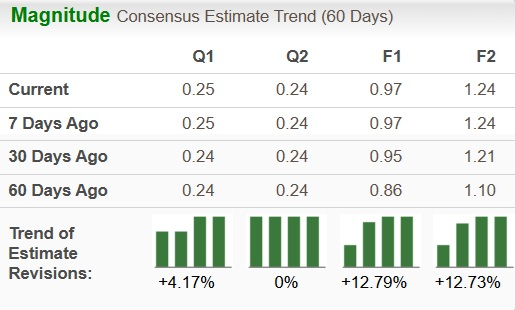

The Zacks Consensus Estimate for TOST’s earnings for 2025 has been revised up 12.8% to 97 cents over the past 60 days.

TOST currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 2 hours | |

| 4 hours |

CoreWeave Stock Falls Amid Blue Owl Doubts, Data Center Debt Financing Report

ORCL -5.40%

Investor's Business Daily

|

| 7 hours | |

| 8 hours | |

| 10 hours | |

| 10 hours | |

| 11 hours | |

| 12 hours | |

| 12 hours | |

| 12 hours | |

| 13 hours | |

| 13 hours | |

| Feb-19 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite