|

|

|

|

|||||

|

|

|

The Estee Lauder Companies Inc. (EL) reported fourth-quarter fiscal 2025 results, with the top and bottom lines beating the Zacks Consensus Estimate. However, net sales and earnings declined year over year.

Adjusted earnings of 9 cents per share beat the Zacks Consensus Estimate of 8 cents in the fiscal fourth quarter. The bottom line decreased 85% from earnings of 64 cents in the year-ago quarter.

The Estee Lauder Companies Inc. price-consensus-eps-surprise-chart | The Estee Lauder Companies Inc. Quote

The company's quarterly net sales of $3,411 million beat the Zacks Consensus Estimate of $3,402 million. However, the top line declined 12% year over year. Organic net sales declined 13% to reach $3,381 million, reflecting decreases across all product categories, except Fragrance, and all geographic regions.

Skin Care’s sales were down 16% year over year to $1,705 million. The downside is primarily due to Estee Lauder and La Mer, reflecting the challenges in the company’s Asia travel retail business.

Makeup revenues declined 11% year over year to $982 million, primarily due to lower Estee Lauder sales from softness in Asia travel retail, declines across all regions for M·A·C, and reduced North American sales for Too Faced, impacted by retail softness and the timing of shipments.

In the Fragrance category, revenues of $560 million increased 4%, led by luxury brands Le Labo and Jo Malone London. Growth was supported by successful hero product franchises, innovation, targeted consumer expansion throughout fiscal 2025, and increased consumer-facing investments.

Hair Care sales totaled $141 million, down 15% year over year, largely due to ongoing brick-and-mortar challenges in North America, which offset benefits from the fourth-quarter fiscal 2025 launch of Aveda in Amazon’s U.S. Premium Beauty store.

Sales in the Americas fell 6% year over year to $949 million. Revenues in the Europe, the Middle East & Africa (EMEA) region declined 22% to $1,293 million. In the Asia-Pacific region, sales tumbled 3% to $1,166 million.

The Estee Lauder Companies’ adjusted gross margin improved 10 basis points year over year to 71.9%. This growth was primarily fueled by gains from the company’s Profit Recovery and Growth Plan (“PRGP”).

The company reported an operating loss of $390 million compared with a loss of $233 million in the prior-year period. Excluding returns and charges related to restructuring and other activities, the operating loss was $288 million compared with a loss of $137 million a year ago, caused by declines across all product categories and geographic regions, with the exception of Asia/Pacific. Adjusted Operating Income declined 61% to reach $137 million.

This Zacks Rank #3 (Hold) company exited the quarter with cash and cash equivalents of $2,921 million, long-term debt of $7,314 million and total equity of $3,865 million.

The net cash flow provided for operating activities for the 12 months ended June 30, 2025, was $1,272 million. Capital expenditures during this time amounted to $602 million. The company said it paid a dividend totaling $618 million during this time.

EL announced a quarterly dividend of 35 cents per share on its Class A and Class B Common Stock, payable Sept. 16 to its shareholders of record as of Sept. 2, 2025.

In February 2025, The Estee Lauder Companies announced an expansion of the PRGP, including a comprehensive restructuring initiative aimed at transforming its operating model. The plan is set to be largely executed with completion expected in fiscal 2027, when the company anticipates realizing nearly all of the full run-rate benefits. The PRGP is designed to support a return to sales growth in fiscal 2026, restore a solid double-digit adjusted operating margin over the next few years and continue to mitigate the impact of external market volatility.

The Estee Lauder Companies anticipates incurring restructuring and related charges ranging from $1.2 billion to $1.6 billion before taxes as part of its PRGP. The restructuring initiative is expected to generate annual gross benefits estimated between $800 million and $1 billion, before taxes. As part of this effort, the company predicts a net reduction in positions of approximately 5,800 to 7,000.

For fiscal 2026, reported net sales are estimated to rise 2-5% compared with the prior-year level. The company’s adjusted organic net sales are also anticipated to grow 0-3% in the year. The adjusted earnings per share are likely to increase 26-39%, ranging from $1.90 to $2.10 in fiscal 2026. Adjusted operating margin is expected at 9.4-9.9%.

For the first quarter of fiscal 2026, the company expects organic net sales in the range of a low-single-digit decline to slightly positive. This outlook indicates high-single-digit growth in the global travel retail business, a return to solid growth in mainland China and a more moderate decline in other markets.

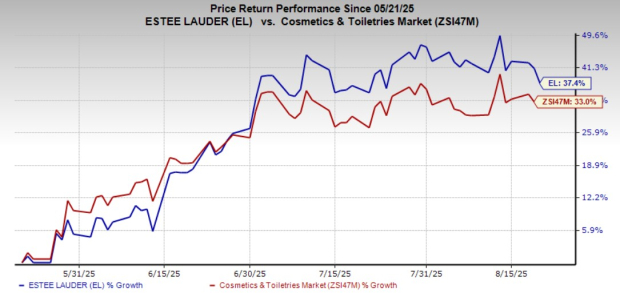

EL stock has gained 37.4% in the past three months compared with the industry’s growth of 33%.

Levi Strauss & Co. (LEVI) designs, markets, and sells apparels and related accessories for men, women, and children in the United States and internationally. It flaunts a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Levi’s current fiscal-year earnings indicates growth of 4% from the year-ago actual. LEVI delivered a trailing four-quarter average earnings surprise of 25.9%.

Wolverine World Wide, Inc. (WWW) designs, manufactures, sources, markets, licenses, and distributes footwear, apparel, and accessories. It currently sports a Zacks Rank of 1. WWW delivered a trailing four-quarter average earnings surprise of 39.1%.

The Zacks Consensus Estimate for Wolverine’s current fiscal-year earnings and sales indicates growth of 44% and 6.1%, respectively, from the year-ago actuals.

Dillard's, Inc. (DDS) operates retail department stores in the southeastern, southwestern, and midwestern areas of the United States, currently carries a Zacks Rank #2 (Buy). DDS delivered a trailing four-quarter average earnings surprise of 24%.

The Zacks Consensus Estimate for Dillard's current fiscal-year sales and earnings indicates a decrease of 0.1% and 16.8%, respectively, from the year-ago period’s levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-30 | |

| Mar-30 | |

| Mar-30 | |

| Mar-27 | |

| Mar-27 | |

| Mar-26 | |

| Mar-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite