|

|

|

|

|||||

|

|

|

During the pandemic, investors got overly excited about the prospects for this business.

As pandemic pressures eased, shares plunged, partly thanks to management's decision to overhaul its operations.

Q2 earnings were weak, but there were glimmers of progress that suggest a long-term opportunity.

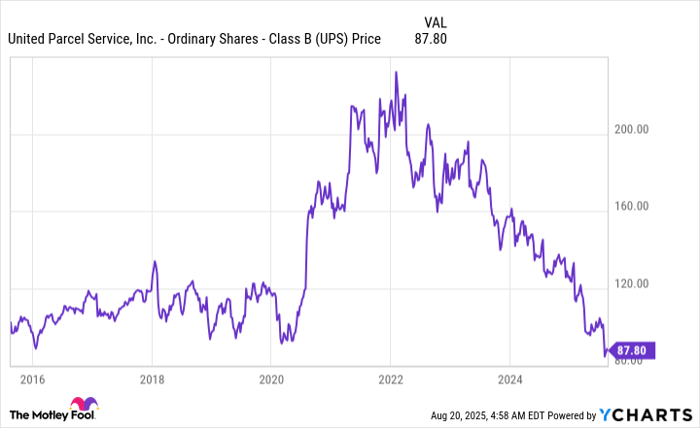

The world was in a shocking state of uncertainty during the coronavirus pandemic's height, leading to odd dislocations in the stock market. United Parcel Service (NYSE: UPS) found itself caught in a temporary updraft in demand for its services, and investors got excited, pushing the stock price skyward. Then things went back to normal, and UPS' share price plunged. For long-term investors who like to buy and hold, the stock might be worth looking at because of this.

On one level, UPS did nothing wrong when the pandemic hit. It simply operated in a business, package delivery, that had a strong story. People stuck at home, socially distancing, shopped online more. That required packages to be shipped in greater numbers, at least for a little while. But investors have a bad habit of taking current trends and extending them out too far into the future. So the unusual conditions of the pandemic were treated as if they were the new normal.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Data by YCharts.

The world figured out how to live with COVID-19. People went back to stores. Demand for package delivery returned to historically normal levels. And UPS' stock cratered, despite the fact that a bear market had turned into a bull market. At this point, UPS stock is trading down around 60% from its pandemic-era peak. In fact, the stock is now back to around the levels it traded at prior to the pandemic.

During all this upheaval, management did something important. It made the decision that UPS needed to update its operations. That process is ongoing, and it has investors worried about the future. The stock continues to languish and will likely do so for longer. UPS is a turnaround story at this point.

Image source: Getty Images.

The big-picture view of what UPS is doing is fairly simple. It is updating its operating systems, streamlining operations, and focusing on its most profitable business. These are the types of things you want a company to do. The problem is that there are costs associated with these actions, and those costs are weighing heavily on business performance and the income statement right now.

For example, in the second quarter, there were "after-tax transformation strategy costs of $57 million." That covers things like closing locations and reducing headcount. Even after an offset from an asset sale and other one-time benefits, this one-time charge still took $0.04 off earnings. Focusing on more profitable business has also meant reducing lower-margin deliveries, notably from UPS' largest customer, Amazon. That's a big hindrance to revenue, which fell 2.7% year over year in Q2.

However, not all the news is bad. Notably, revenue per piece in the U.S. market rose 5.5%. Customer and product mix accounted for 200 basis points of the improvement. That's exactly what you would hope to see as UPS works to reduce lower-value package delivery volume. Notably, adjusted operating margin was flat year over year, despite lower revenue. Again, that's what you would expect to see based on what management is attempting to do.

Delivering packages is a business that is likely to get more important over time, not less. So UPS' business is vital to the world. What it is attempting to do is update its operations so it can be as profitable as possible, which is the right move to make. There are costs associated with this decision, but it looks like progress is being made. The one caveat here, however, is that the 7.4% dividend yield is increasingly looking less sustainable.

The dividend payout ratio in the second quarter was above 100%. Income investors need to go in aware of the risk of a dividend cut. But, for those interested in a turnaround story, UPS looks like it is making important progress. That could make the stock, backed by a delivery business that would be nearly impossible to recreate, worth buying and holding for the long term.

Before you buy stock in United Parcel Service, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and United Parcel Service wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $650,499!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,072,543!*

Now, it’s worth noting Stock Advisor’s total average return is 1,045% — a market-crushing outperformance compared to 182% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 18, 2025

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon and United Parcel Service. The Motley Fool has a disclosure policy.

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-22 | |

| Feb-22 | |

| Feb-21 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite