|

|

|

|

|||||

|

|

|

Lamar Advertising Company LAMR holds a significant market share in the U.S. outdoor advertising business. Its diversified tenant base, opportunistic acquisitions and efforts to upgrade its portfolio are key growth drivers.

However, caution among advertisers amid the uncertain macroeconomic situation and competition from other outdoor advertisers and other media forms is likely to affect its performance in the near term. High debt burden also ails.

Early this month, LAMR reported second-quarter 2025 adjusted funds from operations (AFFO) per share of $2.22, which outpaced the Zacks Consensus Estimate of $2.15. The figure also compared favorably with the prior-year quarter's tally of $2.08.

Results reflected year-over-year growth in the top line. However, higher direct advertising and general and administrative expenses during the quarter acted as a dampener.

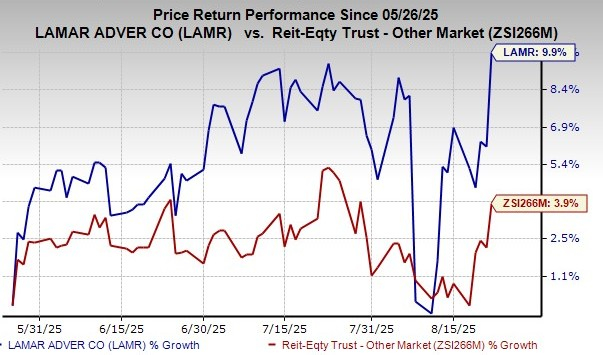

Shares of this Zacks Rank #3 (Hold) company have risen 9.9% over the past three months, outperforming the industry’s upside of 3.9%.

Lamar enjoys an impressive national footprint and holds a leading position as a provider of logo signs in the United States. The company enjoys a diversified tenant base comprising tenants from the services, health care, restaurants, retailers, automotive, insurance and gaming categories. This aids in stable revenue generation. In the second quarter of 2025, local and regional sales accounted for 79% of the company’s billboard revenues. Moreover, local and regional sales reported growth for the 17th consecutive quarter.

Over the recent years, Lamar has made efforts to upgrade its portfolio, increasing occupancy in its existing advertising displays and enabling it to enjoy a significant market share in the U.S. outdoor advertising business. The company has added a large number of digital screens through acquisitions and internal conversions over the past several years. It offers customers the largest network of digital billboards in the United States, with more than 5,200 displays as of the end of the second quarter of 2025.

Out-of-home (OOH) advertising has been growing at a rapid pace and continues to increase its market share in comparison with other forms of media. In the upcoming years, higher technology investments are expected to provide support to OOH advertising. The company’s expansion activities over the recent years bode well for long-term growth. During the six months ended June 30, 2025, Lamar completed multiple acquisitions worth $87.1 million.

Lamar operates in an industry that is characterized by high barriers to entry due to permitting restrictions. Moreover, as there is a control on the permits, inventory as well as an intrusion from other market players, both local and national, are restricted. This helps support advertising rates.

Solid dividend payouts remain the biggest attraction for REIT investors, and Lamar remains committed to the same. In the past five years, the company has raised its dividend eight times. Its five-year annualized dividend growth rate is 21.49%, which is encouraging.

LAMR faces competition from other outdoor advertisers for customers, display locations and structures. The company also competes with other forms of media, such as television, radio, print media, direct mail marketers and online, mobile and social media platforms. So, despite a significant portion of the company’s revenues coming from local businesses, this competition from national players may partly impede its growth momentum. Moreover, given the uncertain macroeconomic situation, advertisers remain cautious, impacting Lamar’s revenue growth.

Despite the Federal Reserve announcing rate cuts late in 2024, the interest rate is still high and is a concern for Lamar Advertising. The company has a substantial debt burden, and its total debt as of June 30, 2025, was approximately $3.38 billion.

Analysts seem bearish on this stock, with the Zacks Consensus Estimate for its 2025 FFO being revised southward by 1.6% over the past month.

Some better-ranked stocks from the broader REIT sector are Welltower WELL and Tereno Realty TRNO, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for WELL’s 2025 FFO per share has been raised marginally over the past month to $5.06.

The consensus estimate for TRNO’s 2025 FFO per share has been revised upward marginally to $2.61 over the past month.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO), a widely used metric to gauge the performance of REITs.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| Jul-22 | |

| Jul-21 | |

| Jul-13 | |

| Jul-10 | |

| Jul-08 | |

| Jul-08 | |

| Jul-06 | |

| Jul-01 | |

| Jun-30 | |

| Jun-25 | |

| Jun-23 | |

| Jun-23 | |

| Jun-23 | |

| Jun-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite