|

|

|

|

|||||

|

|

|

As DICK’S Sporting Goods Inc. DKS prepares to announce its second-quarter fiscal 2025 earnings on Aug. 28, investors are closely watching for insights into its performance this season.

DKS is expected to register a year-over-year sales increase in the quarter under review. The Zacks Consensus Estimate for revenues is pegged at $3.6 billion, indicating a rise of 3.6% from the year-ago quarter’s reported figure.

However, the consensus estimate for earnings is pegged at $4.29 per share, which indicates a dip of 1.8% from the year-ago reported number. The consensus mark has remained stable in the past seven days. The company has a trailing four-quarter earnings surprise of 5.6%, on average.

DICK'S Sporting Goods, Inc. price-consensus-eps-surprise-chart | DICK'S Sporting Goods, Inc. Quote

DICK’S quarterly performance is likely to have reflected gains from solid strategic efforts, brand strength and market share gains. Also, strong comparable store sales (comps) and healthy transaction growth are expected to have acted as tailwinds. The company has also been enhancing service levels through its digital and store experiences to cater well to the athletes’ needs.

Supported by pricing optimization, differentiated product access and the continued strength of vertical brands like DSG, CALIA and VRST, DKS is well-positioned to see margin benefits carry into the fiscal second quarter. Ongoing investments in digital, stores and marketing are designed to fuel long-term growth. If the revenue impact of these investments continues to outpace expense growth, the company could sustain margin expansion in the fiscal second quarter despite cost pressures.

DKS is also enhancing service levels at all its digital and store experiences to cater well to the athletes’ needs. It is leaning heavily into three growth pillars: expanding experiential formats like House of Sport and Field House (about 32 new stores across 2025), strengthening key categories with premium access to launches, and accelerating its e-commerce and digital ecosystem. The company’s omnichannel push, including app-driven launches and digital platforms like GameChanger and DICK’S Media Network, continues to outpace overall growth. Its store-expansion initiatives, driven by DICK'S House of Sport, Golf Galaxy Performance Center, Public Lands and Going, Going, Gone! Stores, bode well. These areas are expected to play a bigger role in scaling revenues in the to-be-reported quarter.

However, DICK’S continues to face an uncertain macroeconomic environment, while tariff-related challenges are expected to pressure performance in the near term. The company’s earnings outlook already factors in the anticipated impact of existing tariffs. Higher wage rates, along with increased investments in talent and technology to create a better athlete experience, and investments in marketing, have been leading to elevated costs for a while. This is expected to result in an increase in SG&A expenses in the to-be-reported quarter. Our model indicates adjusted SG&A expenses to increase 7.9% year over year for the fiscal second quarter.

Our proven model conclusively predicts an earnings beat for DICK'S this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat, which is exactly the case here.

DICK'S currently has an Earnings ESP of +0.62% and a Zacks Rank of 3. You can uncover the best stocks before they’re reported with our Earnings ESP Filter.

DICK'S has a forward 12-month price-to-earnings ratio of 15.28x, which is below the five-year high of 22.59x and the Retail - Miscellaneous industry’s average of 19.39x.

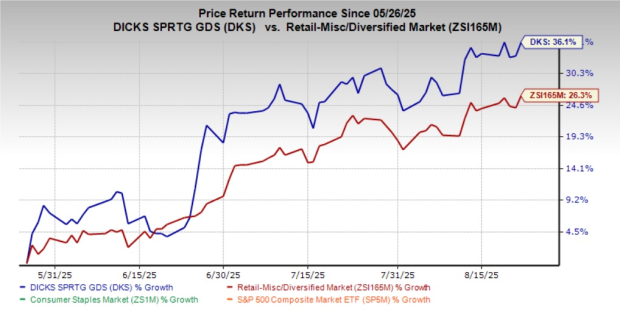

The recent market movements show that DKS’ shares have gained 36.1% in the past three months compared with the industry's 26.3% growth.

Here are some other companies, which, according to our model, have the right combination of elements to beat on earnings this reporting cycle.

Abercrombie & Fitch Co. ANF has an Earnings ESP of +2.62% and a Zacks Rank of 3 at present. ANF’s earnings for the second quarter of fiscal 2025 are expected to decrease 9.2% on a year-over-year basis. The consensus mark for its quarterly earnings has moved up 0.9% to $2.27 per share in the past 30 days. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Abercrombie & Fitch’s quarterly revenues is pegged at $1.19 billion, which suggests growth of 4.8% from the figure reported in the prior-year quarter. ANF has a trailing four-quarter earnings surprise of 11.2%, on average.

Five Below, Inc. FIVE currently has an Earnings ESP of +13.35% and a Zacks Rank of 3. FIVE is likely to register growth in its top and bottom lines when it reports second-quarter fiscal 2025 results. The Zacks Consensus Estimate for its quarterly revenues is pegged at $997.3 million, indicating 20.2% growth from the figure reported in the year-ago quarter.

The consensus estimate for FIVE’s earnings has moved up by two pennies in the past 30 days to 61 cents per share. The consensus estimate indicates growth of 13% from the year-ago quarter’s actual. FIVE has a trailing four-quarter earnings surprise of 42.3%, on average.

Dollar Tree Inc. DLTR currently has an Earnings ESP of +9.63% and a Zacks Rank of 3. The company is likely to register a decline in its top and bottom lines when it reports second-quarter fiscal 2025 results. The consensus mark for DLTR’s quarterly revenues is pegged at $4.5 billion, which indicates a plunge of 39.7% from the figure reported in the prior-year quarter.

The Zacks Consensus Estimate for Dollar Tree’s earnings has moved up by a penny in the past 30 days to 37 cents per share. The consensus estimate indicates a drop of 44.8% from the year-ago quarter’s actual. DLTR delivered a negative trailing four-quarter earnings surprise of 6.9%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 7 hours | |

| 7 hours | |

| 8 hours | |

| 9 hours | |

| 10 hours | |

| 12 hours | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite