|

|

|

|

|||||

|

|

|

CrowdStrike Holdings, Inc. CRWD is preparing to announce its fiscal 2026 second-quarter earnings after the closing bell on Aug. 27. CrowdStrike has gained favor on Wall Street as demand for contemporary security solutions remains robust.

However, its stock faced downward pressure after the company provided a rather disappointing fiscal second-quarter revenue guidance. As a result, the upcoming earnings report is critical for CrowdStrike’s stock performance, prompting investors to consider strategic actions at this juncture.

CrowdStrike’s revenue growth for the fiscal first quarter was not particularly strong, with a year-over-year increase of 20%, reaching $1.10 billion. This growth rate is lower than the 29% year-over-year growth for the full fiscal year 2025.

Looking ahead, CrowdStrike anticipates that its revenues for the second quarter will fall between $1.14 billion and $1.15 billion. The mid-point of the guidance indicates 19% year-over-year growth, but this rate still falls short of the growth the company experienced in the fiscal first quarter.

Not only is CrowdStrike’s revenue guidance worrisome, but its cash generation decreased in the fiscal first quarter. The company reported free cash flow of $279.4 million, which is lower than the $322.5 million it generated in the same period last year. This decline is attributed to $61 million in expenses incurred last summer due to a platform outage.

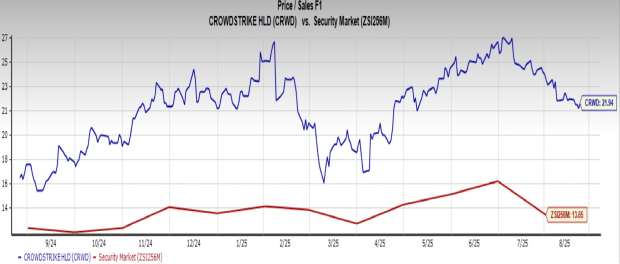

On top of it, CrowdStrike’s forward price-to-sales (P/S) ratio stands at 21.9 compared to 13.7 for the Security industry. The high valuation of CrowdStrike, along with lower-than-expected revenue growth and decreasing free cash flow, suggests that new investors should be careful and wait for the fiscal second-quarter results before investing in the stock.

Image Source: Zacks Investment Research

New investors also shouldn’t forget that CrowdStrike is facing pricing pressure from well-funded competitors like Microsoft Corporation MSFT. The Microsoft 365 E5 includes endpoint security. As a result, customers already paying for E5 face minimal additional costs for endpoint security, making it challenging for CrowdStrike as companies seek to optimize their technology investments.

CrowdStrike’s fiscal second-quarter results might not be extraordinary, but continued growth is anticipated, likely reassuring stakeholders to keep their shares.

Additionally, CrowdStrike’s long-term outlook remains bright. This is highlighted by their annual recurring revenue (ARR) reaching a record $4.4 billion in the fiscal first quarter, marking a 22% rise from the same period last year. Although ARR growth has slowed in recent quarters due to last year’s Falcon outage, management believes the long-term effects will be short-lived. They expect ARR to reach $10 billion by fiscal year 2031, representing a 127% increase from the current levels.

Furthermore, reaching $10 billion would still be a small part of CrowdStrike’s projected addressable market of $116 billion, showing considerable growth potential in the coming years. For now, CrowdStrike has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks Rank #1 (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 |

These Stocks Lead Dow Jones In February. Hint: It's Not AI Companies.

MSFT

Investor's Business Daily

|

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite