|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Brookfield Asset Management is a large Canadian asset manager with a focus on infrastructure.

The stock has risen dramatically thanks to management's focus on expanding its business.

Despite a 45% price advance, there is still a material growth opportunity ahead of Brookfield Asset Management.

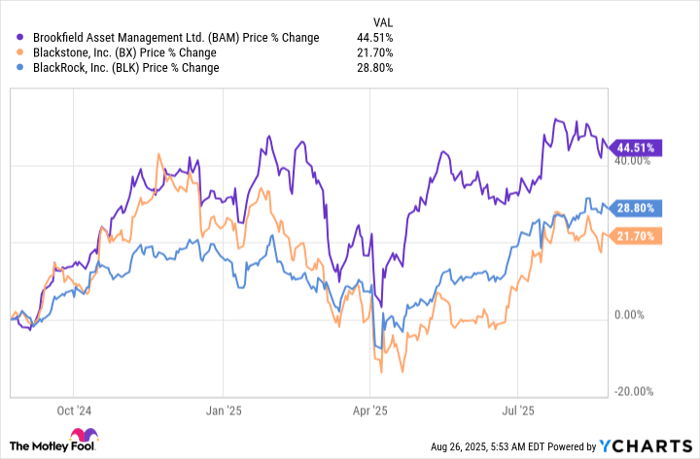

Brookfield Asset Management (NYSE: BAM) is a growth and income story. But there's a wrinkle here because the stock has risen dramatically during the past year, jumping by 45% and easily outpacing the S&P 500 index (SNPINDEX: ^GSPC). Investors looking at Brookfield Asset Management now have to ask themselves if there's more room to run or if Wall Street has fully priced the opportunity. Here's why you might still want to buy this high-yield stock.

As an asset manager, Brookfield Asset Management takes money from others and, for a fee, invests it on their behalf. Historically the company has focused on infrastructure projects, but it has been branching out a bit more lately. Today it has offerings in the clean energy, infrastructure, real estate, private equity, and credit markets. Each one is a substantial business, supporting a total fee-bearing capital base of roughly $550 billion across all five.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Image source: Getty Images.

Fee-bearing capital is where the company is focused on growing, with a target of increasing that number to $1.1 trillion by 2030. Management believes it is well positioned to do this because it is homing in on three key global trends: digitization, decarbonization, and deglobalization. As fee-bearing capital increases, so does the company's ability to generate revenue and earnings on its income statement.

Based on management's internal projections, it believes it will be able to increase fee-related earnings 17% a year through 2030. It expects that this growth will support dividend growth of 15% a year. These are big numbers, noting that a 15% dividend growth rate would mean doubling the dividend in about five years.

Wall Street is clearly well aware of the opportunity here, noting the stock's material share price advance during the past year. However, there are still some interesting numbers to consider. For example, if the dividend were to double, based on the math of dividend yields, the stock price would need to double, too, in order to maintain Brookfield Asset Management's current dividend yield of 2.9%.

The dividend yield here, meanwhile, is above the yields of some of the company's large U.S. peers. Blackstone's (NYSE: BX) yield is 2.5% and BlackRock's (NYSE: BLK) yield is 1.8%. This is notable because it highlights that Brookfield Asset Management's yield isn't out of line with peers. In fact, using yield as a rough gauge of valuation, this comparison actually suggests that the Canadian asset manager may even be cheap relative to competitors.

Looking at a more traditional valuation ratio like the price-to-earnings (P/E) ratio is a bit less favorable. Brookfield Asset Management's P/E is about 42, compared to Blackstone's 46 and BlackRock's 28. But even here, Brookfield Asset Management's valuation doesn't look wildly out of line. That hints that the earnings and dividend growth projected could, indeed, still lead to solid share price advances over the next five years or so.

The complicating factor here is the fast rise in Brookfield Asset Management's stock during the past year. It has not only outperformed the market by a wide margin, but it has also solidly outperformed both Blackstone and BlackRock. It wouldn't be shocking to see the stock pull back some in the near term, particularly if there is a bear market.

Ultimately, the real opportunity is long-term when you look at Brookfield Asset Management today. However, if you have a buy-and-hold approach, it looks like management's growth plan could lead to further dividend hikes and an even higher stock price for patient investors. Just go in prepared to stick around through a market downturn, since five years is actually a fairly long time on Wall Street.

Before you buy stock in Brookfield Asset Management, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Brookfield Asset Management wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $656,895!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,102,148!*

Now, it’s worth noting Stock Advisor’s total average return is 1,062% — a market-crushing outperformance compared to 184% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 25, 2025

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Blackstone. The Motley Fool recommends Brookfield Asset Management. The Motley Fool has a disclosure policy.

| 29 min | |

| 3 hours | |

| 4 hours | |

| 5 hours | |

| 7 hours | |

| 7 hours | |

| 8 hours | |

| 10 hours | |

| 12 hours | |

| 15 hours | |

| Feb-19 |

Private-Credit Warning Signs Flash After Blue Owl Unloads $1.4 Billion in Assets

BX -5.37%

The Wall Street Journal

|

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite