|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

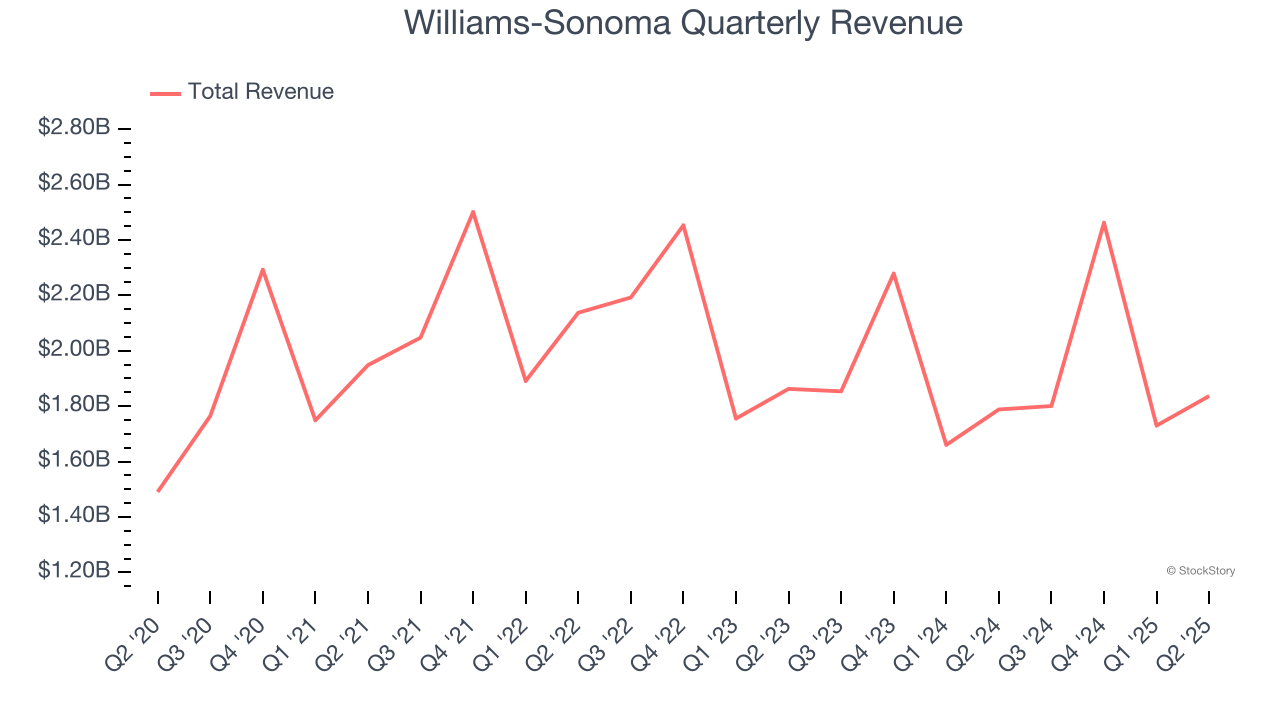

Kitchenware and home goods retailer Williams-Sonoma (NYSE:WSM) met Wall Street’s revenue expectations in Q2 CY2025, with sales up 2.7% year on year to $1.84 billion. Its GAAP profit of $2 per share was 11.4% above analysts’ consensus estimates.

Is now the time to buy Williams-Sonoma? Find out by accessing our full research report, it’s free.

Started in 1956 as a store specializing in French cookware, Williams-Sonoma (NYSE:WSM) is a specialty retailer of higher-end kitchenware, home goods, and furniture.

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $7.83 billion in revenue over the past 12 months, Williams-Sonoma is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Williams-Sonoma’s sales grew at a tepid 5.1% compounded annual growth rate over the last six years (we compare to 2019 to normalize for COVID-19 impacts) as it closed stores.

This quarter, Williams-Sonoma grew its revenue by 2.7% year on year, and its $1.84 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last six years. This projection is underwhelming and suggests its products will face some demand challenges.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

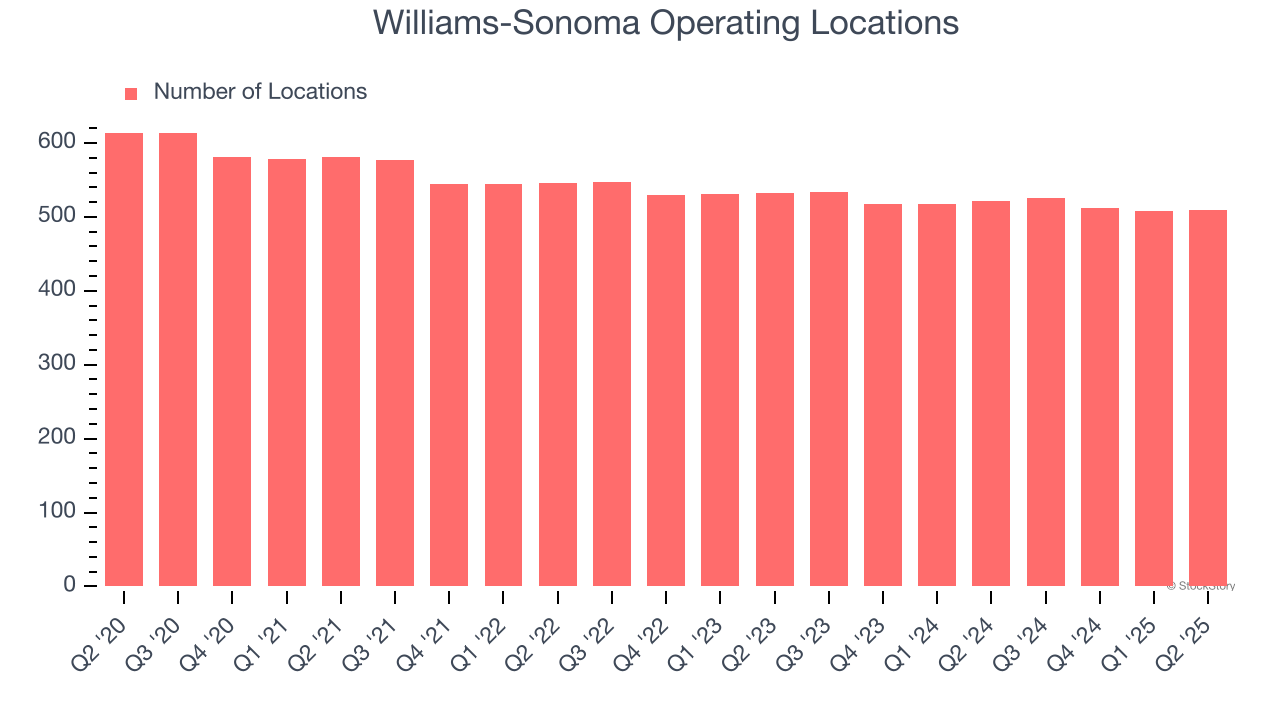

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Williams-Sonoma listed 509 locations in the latest quarter and has generally closed its stores over the last two years, averaging 2% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

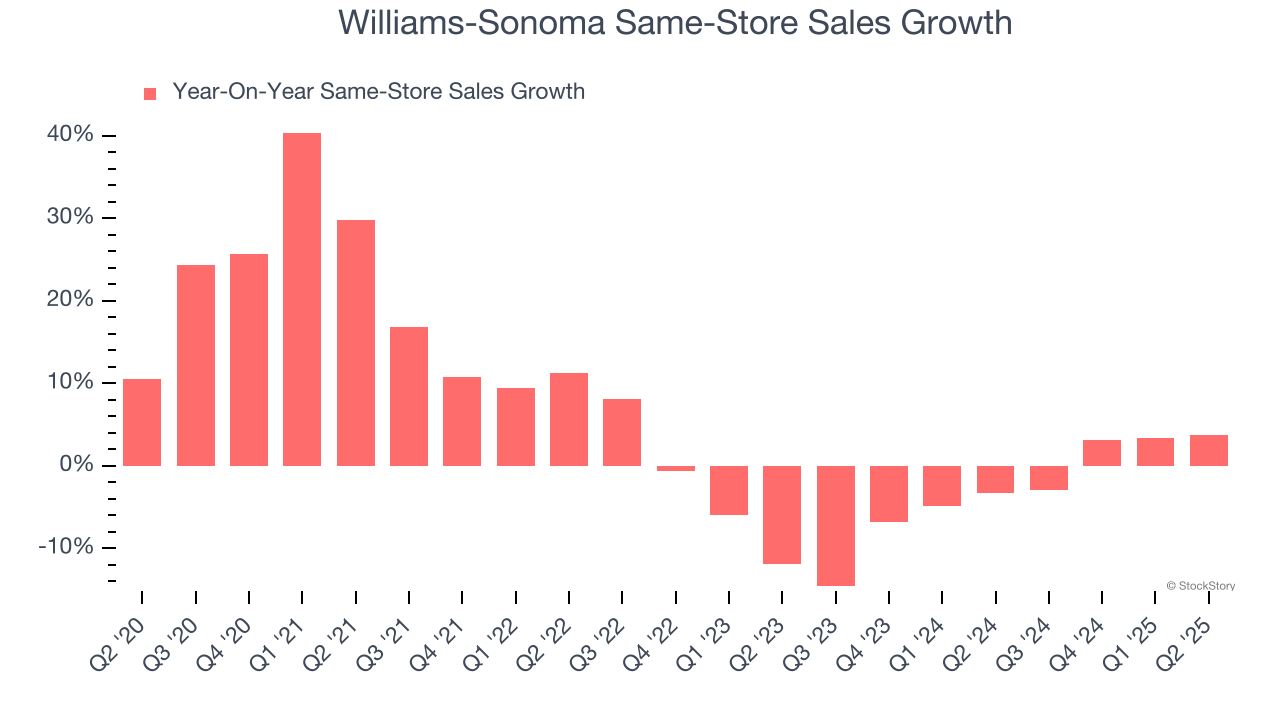

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Williams-Sonoma’s demand has been shrinking over the last two years as its same-store sales have averaged 2.8% annual declines. This performance isn’t ideal, and Williams-Sonoma is attempting to boost same-store sales by closing stores (fewer locations sometimes lead to higher same-store sales).

In the latest quarter, Williams-Sonoma’s same-store sales rose 3.7% year on year. This growth was a well-appreciated turnaround from its historical levels, showing the business is regaining momentum.

We were impressed by how significantly Williams-Sonoma blew past analysts’ earnings expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 2.7% to $203 immediately after reporting.

Indeed, Williams-Sonoma had a rock-solid quarterly earnings result, but is this stock a good investment here? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

| 1 hour | |

| 2 hours | |

| 4 hours | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-16 | |

| Feb-12 | |

| Feb-11 | |

| Feb-10 | |

| Feb-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite