|

|

|

|

|||||

|

|

|

PayPal now makes up 15% of Punch Card Management's portfolio.

The company has rebranded its services and profit margins are widening.

Management is aggressively repurchasing stock.

Warren Buffett has inspired investors to mimic in his style and try to beat the market. One fund manager who takes the buy-and-hold approach to heart is Norbert Lou of Punch Card Management. This patient investor has a concentrated portfolio that rarely takes new positions, staying disciplined in the Buffett manner.

However, last quarter, Lou surprised the market with his latest 13-F filing by investing in two new stocks for his concentrated portfolio. One is PayPal (NASDAQ: PYPL), which now makes up 15% of his portfolio. With the stock still down 77% from highs set during the pandemic, is PayPal now a value investor's dream? Let's take a closer look at this financial technology (fintech) giant and see if it is a buy today.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

PayPal's downfall came from relying on too many acquisitions that became overwhelming for the business to absorb. It acquired many different companies over the years, including iZettle, Honey, and Xoom, which have generally been disappointments. Now, with new management in charge, PayPal is simplifying its value proposition for consumers and its merchant partners.

With the core PayPal service, the company has rebranded the application as a way to easily shop for discounts instead of its historical money transfer service. Sitting between millions of merchants and hundreds of millions of shoppers, PayPal has been able to partner with brands on cash-back programs for shoppers who pay with PayPal. This has helped what the company calls "branded experiences" see accelerating growth to 8% year over year last quarter. This includes payment methods like in-store shopping with the PayPal and Venmo debit cards, which are gaining wide adoption.

The other core pillar of the PayPal business today is Braintree, its unbranded checkout option for online payment processing for merchants. New management shook up this business, which was targeting unprofitable merchant partnerships. Trimming the fat has slowed payment volume growth for Braintree, but the company now believes it has gotten past the peak headwinds from these decisions, with Braintree volumes forecast to grow in the quarters ahead.

Image source: Getty Images.

Another tactic from PayPal's new management has been increasing efficiency within the organization. The company hired too many people during the COVID-19 pandemic and went through several layoffs. It is now focused on its core value propositions only, and large pillars of the business like Venmo and Braintree.

Profitability has begun to recover. Operating margin has widened from less than 14% in 2022 to 19% during the past 12 months, with plenty of room to keep expanding. Along with overall sales growth, this has led operating income to more than double from $2 billion to $4.67 billion during the past 12 months, which is close to a record high. Clearly, the company has gotten back on the right footing and is looking to keep earnings increasing in the years to come. This is likely a reason Punch Card Management recently took a position in the stock.

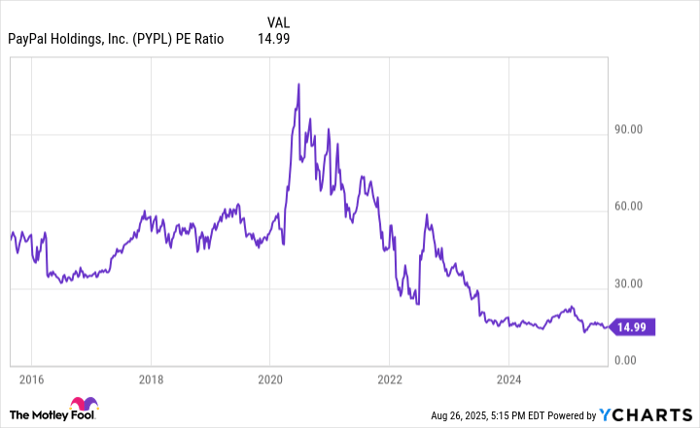

PYPL PE Ratio data by YCharts

Even though PayPal's operating earnings have begun to recover, the stock is still trading at about the same levels it crashed to in 2022, at about $70 a share as of this writing (Aug. 26). With a cheap stock and a bunch of cash piling up on its balance sheet, PayPal management has begun to buy back its own shares in earnest. Shares outstanding are down about 20% in the past five years, with accelerating repurchases in recent quarters. It is now buying back close to 10% of its shares outstanding on an annualized rate, which could have a big impact on the growth of earnings per share down the line.

PayPal is able to repurchase so much of its stock because the shares trade at a low price-to-earnings (P/E) ratio of less than 15. For a company with growing revenue, increasing efficiencies to enhance profit margins, and repurchasing a ton of stock, PayPal is trading at a cheap valuation today. If you are a believer in the long-term health of the PayPal, Venmo, and Braintree businesses, then now is a good time to follow Punch Card Management and invest in this stock.

Before you buy stock in PayPal, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and PayPal wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $661,220!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,114,162!*

Now, it’s worth noting Stock Advisor’s total average return is 1,069% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 25, 2025

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends PayPal. The Motley Fool recommends the following options: long January 2027 $42.50 calls on PayPal and short September 2025 $77.50 calls on PayPal. The Motley Fool has a disclosure policy.

| 2 hours | |

| 6 hours | |

| 6 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours | |

| 8 hours | |

| 8 hours | |

| 9 hours | |

| 9 hours | |

| 9 hours | |

| 9 hours | |

| 9 hours | |

| 9 hours | |

| 10 hours |

Stock Market Today: Dow Dives As EU Makes Trump Tariff Move; Novo Plunges On This (Live Coverage)

PYPL +5.76%

Investor's Business Daily

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite