|

|

|

|

|||||

|

|

|

PayPal Holdings PYPL released impressive third-quarter 2025 results on Oct. 28. Both earnings per share (EPS) and revenues comfortably surpassed the Zacks Consensus Estimates. Meanwhile, the company also raised its full-year guidance. Yet, despite this outperformance, the market’s initial response was muted, with shares slipping 7% since the earnings announcement through Thursday’s closing session.

Given this puzzling divergence between fundamentals and investor reaction, we intentionally waited before publishing our review to gauge whether price movements may reveal deeper sentiment trends.

Now, with the dust settling, it is clear that while the results reinforce PYPL’s robust growth trajectory, the market is weighing other factors alongside the upbeat financials. Let’s delve deeper and find out.

On paper, PayPal’s third quarter was solid. The company reported net revenues of $8.42 billion, up 7.3% year over year and topped the consensus mark of $8.26 billion. Non-GAAP EPS came in at $1.34, denoting a 11.7% increase year over year and well ahead of the Zacks Consensus Estimate of $1.19. Non-GAAP operating income rose 6%. Total Payment Volume (“TPV”) climbed 8.4% to $458.09 billion. Transaction margin dollars (“TM$”) increased 6% to $3.87 billion from the year-ago quarter. Active accounts increased 1% year over year to 438 million.

The company also raised its full-year guidance. It now expects non-GAAP EPS of $5.35-$5.39 (up from $5.15-$5.30) and transaction margin dollar growth of 5%-6%. Free cash flow guidance was reaffirmed at $6-$7 billion. It completed $1.5 billion in share repurchases during the third quarter, bringing share repurchases over the past four quarters to $5.7 billion. Management projects share repurchases to be roughly $6 billion in 2025.

While the earnings beat was clear, the sustainability of the drivers was questioned. In the third quarter, online branded checkout volume grew 5% on a currency-neutral basis. The growth was helped by less pressure on volumes from Asian marketplaces selling to the United States. However, later in the quarter, this improvement was offset by softer consumer discretionary spending in Europe and the United States. Although the company saw consistent growth in the number of checkout transactions, basket sizes or average order value decreased.

In the third quarter of 2025, PayPal's payment transactions decreased 5% to 6.3 billion, when payment service provider (“PSP”) transactions are included. The overall decline in payment transactions was partly influenced by changes in product and merchant mix, and the impact of foreign exchange hedges, which also contributed to a slight decline in the transaction take rate. The decline in transaction numbers does not imply a deterioration in performance but reflects compositional and operational factors, as well as how transactions are counted, specifically excluding PSPs that saw growth.

TM$, excluding interest on consumer balances, increased by 7% in the third quarter. This growth included a 1.5 point headwind due to higher expenses tied to transaction losses, mainly due to temporary service disruption in August, which primarily impacted Germany. In the third quarter, transaction losses increased by 50% year over year, primarily due to a rise in fraud incidents from PayPal’s products and services.

However, these concerns appear more tactical than structural. The broader narrative around PayPal’s recovery and reinvention remains intact.

Venmo is positioned as the preferred money movement platform for the young, affluent, digitally native consumers. Venmo’s user base is large and growing, with nearly 100 million total active accounts increasing at a mid-single-digit rate. In the third quarter of 2025, Venmo’s TPV rose 14%, accelerating sequentially from 12% in the second quarter of 2025. Venmo’s revenues jumped 20% year over year in the third quarter of 2025. Venmo is on track to generate $1.7 billion in revenues in 2025, excluding interest income. This reflects more than 20% upside and a 10-point acceleration compared to two years ago.

Venmo debit card hit a new record in the third quarter, attracting 1 million first-time users, partly driven by college partnerships. In the third quarter, monthly Venmo debit card actives grew by more than 40%. This led to a 7% year-over-year increase in overall Venmo monthly active users to about 66 million. Moreover, Pay with Venmo’s monthly active accounts grew by nearly 25% in the third quarter.

Branded checkout still represents a vital growth driver. In the third quarter, online branded checkout TPV grew 5% on a currency-neutral basis, despite choppy global macro trends.

Beyond the numbers, PayPal made some strategic moves to generate business. The company signed a two-year agreement with Blue Owl Capital, allowing Blue Owl-managed funds to buy about $7 billion worth of PayPal’s “Pay in 4” loans originated in the United States. It also teamed up with Google to deliver frictionless digital commerce experiences. PayPal launched PayPal links for easy money transfers through a personalized, one-time link. It gave early access to Perplexity’s Comet browser for U.S. and some global users. It also introduced PayPal World for seamless global wallet interoperability.

Additionally, PayPal is exploring “agentic commerce” experiences powered by AI partners. On the crypto front, PayPal’s stablecoin PYUSD is now integrated across platforms. Apart from this, U.S. PayPal customers can use the “Pay with Crypto” option at online checkout. These innovations position PayPal not just as a payments company but as a broader commerce platform.

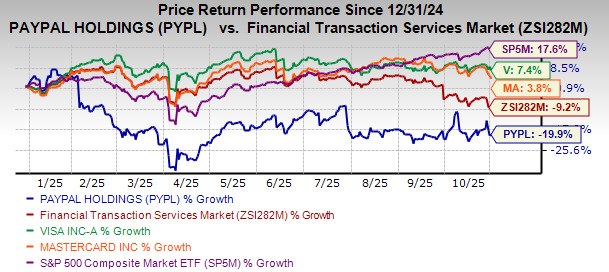

PYPL shares have dropped 19.9% year to date, largely due to intensifying competition in the fintech sector. Rivals like Visa Inc. V and Mastercard Incorporated MA continue to expand their offerings, challenging PayPal’s dominance in digital payments. Broader macroeconomic pressures and uncertainty surrounding the tariff policy have also dampened investor sentiment. While PYPL has struggled, Visa shares have climbed 7.4%, and Mastercard has risen 3.8% over the same timeframe.

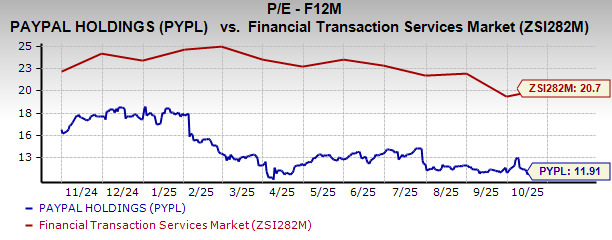

However, with the decline, PayPal shares are trading cheap, as suggested by the Value Score of A. In terms of forward 12-month P/E, PYPL stock is trading at 11.91X compared with the Zacks Financial Transaction Services industry’s 20.70X.

The stock is also cheaper than competitors, including Visa and Mastercard. Shares of Visa and Mastercard are currently trading at P/E of 26.58X and 29.85X, respectively.

PayPal’s estimate revisions reflect a positive trend for full-year 2025 and 2026. The Zacks Consensus Estimate for 2025 earnings is pegged at $5.29 per share, suggesting 13.8% growth over 2024. The consensus mark for 2026 earnings stands at $5.81 per share, calling for a 9.9% increase year over year.

PYPL’s third-quarter 2025 results underscore the company’s overall growth, including strong execution in Venmo, improving branded checkout capabilities, solid innovation in global payments and AI, strong partnerships and crypto integrations. Its raised guidance for the full year signals confidence in the business model and the strategic investments underpinning future growth. The 7% post-earnings share price drop is a reminder that markets can be as much about expectations and sentiment as about performance metrics.

Short-term noise creates long-term opportunity. Therefore, it seems prudent for investors to look past the market’s knee-jerk reaction and buy PayPal stock on weakness. The combination of buybacks and solid cash generation gives the stock a solid foundation for upside, and the future of digital payments still runs through PYPL.

PayPal currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 34 min | |

| 6 hours | |

| 7 hours | |

| 8 hours | |

| 9 hours | |

| 13 hours | |

| 14 hours | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite