|

|

|

|

|||||

|

|

|

Nvidia's data center revenue grew 56% year over year to $41.1 billion.

Relations with China remain a question mark for Nvidia's business.

Nvidia's stock is still very expensive by most metrics.

With earnings season in full swing, there was arguably no company whose results were more anticipated than Nvidia (NASDAQ: NVDA). Over the past couple of years, Nvidia has been in the spotlight due to its crucial role in the artificial intelligence (AI) pipeline.

The hype has propelled Nvidia to the world's most valuable public company, with a market cap of over $4.4 trillion. That's over $600 billion more than second-place Microsoft as of the time of this writing.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Nvidia's fiscal 2026 second-quarter earnings results were good, but a slowdown in its most important segment (data centers) and an underwhelming outlook for the third quarter (by Wall Street's expectations) caused the stock to drop by 3% after hours. Although the pullback might seem minimal, it's worth considering if now is a good time for investors to buy the stock.

Image source: Getty Images.

Nvidia's overall revenue in the second quarter of fiscal 2026 (ending July 27, 2025) increased 56% year over year to $46.7 billion and was 6% more than it made in the first quarter. Its net income grew 59% from last year to $26.4 billion. Both increases were impressive for a company of Nvidia's size, but all eyes were on Nvidia's data center revenue growth.

A large reason for Nvidia's recent success and increased investor interest is the graphics processing units (GPUs) it produces. These GPUs, along with their servers, are a crucial part of data centers and a large reason that companies are able to train, deploy, and scale AI at the levels we've been witnessing. GPUs are to Nvidia's business what iPhones are to Apple's business.

In the second quarter, Nvidia's data center revenue increased 56% from a year ago to $41.1 billion. Again, impressive growth, but short of the $41.3 billion that Wall Street analysts had estimated, which is partly why the stock dropped after reporting its earnings. It was the second quarter in a row that data center revenue missed analysts' estimates.

Nvidia predicts its Q3 revenue will come in at $54 billion, which would be up a 51% increase from last year.

Nvidia CEO Jensen Huang, has made it clear that Nvidia's focus is on being an AI infrastructure company. Huang said he expects the largest AI companies (Microsoft, OpenAI, Amazon, Alphabet, Meta Platforms, and the like) to spend between $3 trillion and $4 trillion on AI-related capital expenditures over the next five years, with Nvidia potentially capturing around 70% of that spend.

Whether this plays out as Huang expects remains to be seen, but if we assume he's correct in this assumption, Nvidia is in a great position to continue its impressive growth, and jumping ship on the company based on one quarter of "underwhelming" data center revenue growth would seem silly.

The one hiccup in Nvidia's way revolves around its and America's volatile relationship with China. The Trump administration set a ban on H20 chip (Nvidia's China-compliant AI chip) sales to China in April before reversing the decision in July after Nvidia agreed to pay the government a 15% tax on AI-chip revenue made in China. Notably, Nvidia disclosed that while the deal is in place, it has not yet been finalized.

Despite the walkback, China encouraged its companies to avoid buying the chip, causing Nvidia to stop its production of them. Overall, Nvidia's future remains promising, but the back-and-forth, volatile relationship with China is something to keep an eye on.

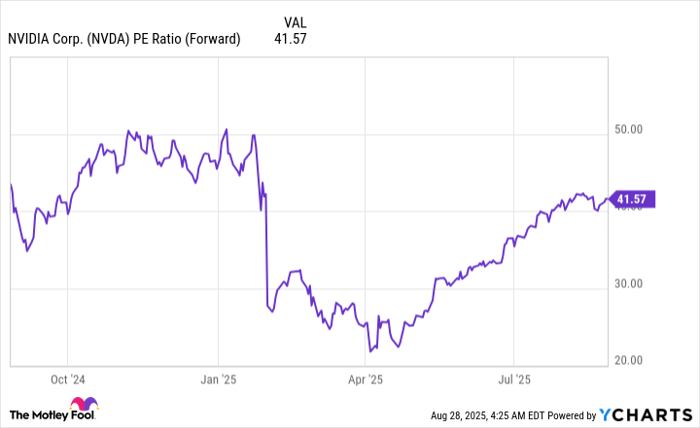

Even after a post-earnings pullback, Nvidia's stock remains expensive. It's currently trading at around 41.5 times its projected earnings for the next 12 months, well above the S&P 500's average for the tech sector, which is around 30.

NVDA PE Ratio (Forward) data by YCharts

Nvidia is also growing its earnings faster than most S&P 500 tech companies, so this in itself isn't a cause to avoid the stock. However, it is a sign to proceed with caution before going all-in because high valuations leave room for sharp pullbacks if Nvidia doesn't meet the lofty expectations that seem priced into the stock.

If you're investing in Nvidia for the long term (which you should be), my recommended approach would be to dollar-cost average your way into a stake or to increase the stake you currently have. This approach helps you gradually add shares while also helping to offset some of the seemingly inevitable volatility the stock will have.

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $659,823!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,113,120!*

Now, it’s worth noting Stock Advisor’s total average return is 1,068% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 25, 2025

Stefon Walters has positions in Apple and Microsoft. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 14 min |

Stock Market Today: Dow, Nasdaq Eke Out Gains; Gold, Silver Names Slide (Live Coverage)

NVDA

Investor's Business Daily

|

| 31 min | |

| 31 min | |

| 33 min | |

| 33 min | |

| 45 min |

Quantum Computing Stocks: Infleqtion Pops In First Day As Public Company

NVDA

Investor's Business Daily

|

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours |

Stock Market Today: Nasdaq, Dow Climb; Airline Name Flies Higher (Live Coverage)

NVDA

Investor's Business Daily

|

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours |

Stock Market Today: Dow Weakens As Nasdaq Lags; Biotech Name Hits Record (Live Coverage)

NVDA

Investor's Business Daily

|

| 4 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite