|

|

|

|

|||||

|

|

|

Guess?, Inc. (GES) reported second-quarter fiscal 2026 results, wherein both top and bottom lines beat the Zacks Consensus Estimate. While net sales increased, earnings decreased from the year-ago period’s actuals.

On Aug. 20, 2025, Guess? announced a deal with Authentic Brands Group and key shareholders to form a strategic partnership. Under the agreement, Authentic will acquire 51% of the company’s intellectual property, while the Rolling Stockholders will hold the remaining 49% and assume full ownership of its operating assets. The transaction is expected to close in the fourth quarter of fiscal 2026.

Guess? posted adjusted earnings of 26 cents per share, beating the Zacks Consensus Estimate of 14 cents. However, the bottom line deteriorated 38% from 42 cents reported in the year-ago quarter.

Guess?, Inc. price-consensus-eps-surprise-chart | Guess?, Inc. Quote

Net revenues amounted to $772.9 million, up 6% year over year, surpassing the consensus mark of $757 million. On a constant-currency (cc) basis, net revenues rose 3%. The strong performance was driven by better-than-expected comparable store sales in the European business and the Americas Retail segment.

Adjusted earnings from operations were $28.5 million, down 25% from $37.9 million reported in the year-ago quarter. The adjusted operating margin was 3.7%, down from 5.2% reported in the same quarter last year. This decline was primarily due to increased expenses, including higher advertising and store-related costs, as well as the unfavorable impact of business mix and higher markdowns.

The Europe segment’s revenues increased 14% on a reported basis and 9% at cc. Retail comp sales (including e-commerce) increased 11% on a reported basis and 5% at cc. The segmental operating margin was 10.6%, up 0.8% year over year, reflecting the benefit of higher revenues and favorable currency effects, partially offset by increased expenses, including elevated advertising and store costs, and higher markdowns.

Revenues in the Americas Retail segment decreased 1% in U.S. dollars and at cc. Retail comparable sales, including e-commerce, declined 5% in U.S. dollars and at cc. The operating margin in the segment was negative 3.7%, down 5.2% year over year. This decline was caused by elevated expenses, including increased advertising and store costs, the adverse effects of negative retail comparable sales, increased markdowns and lower initial markups, partially offset by the impact of newly acquired businesses.

Americas Wholesale revenues decreased 11% on a reported basis and 10% at cc. The segment’s operating margin improved to 19.6%, up 0.7% year over year, driven by elevated product margin, partially offset by the impact of lower revenues.

Asia revenues increased 3% on a reported basis and 2% at cc. Retail comp sales (including e-commerce) dropped 2% on both a reported basis and at cc. The operating margin in the segment was negative 6.8%, down 4.5% year over year. This downside was due to the impact of an unfavorable business mix.

Licensing revenues decreased 10% on a reported basis and at cc. Segmental operating margin was 95.4% compared with 93.3% in the year-ago quarter.

The company exited the quarter with cash and cash equivalents of $189.6 million and long-term debt and finance lease obligations of nearly $258.4 million. Stockholders’ equity was around $487.6 million.

Net cash provided by operating activities for the six months ended Aug. 2, 2025, was $1.5 million. Free cash flow for the same period amounted to negative $44.6 million.

GES announced a quarterly dividend of 22.5 cents per share, payable on Sept. 26, 2025, to its shareholders on record as of Sept. 10.

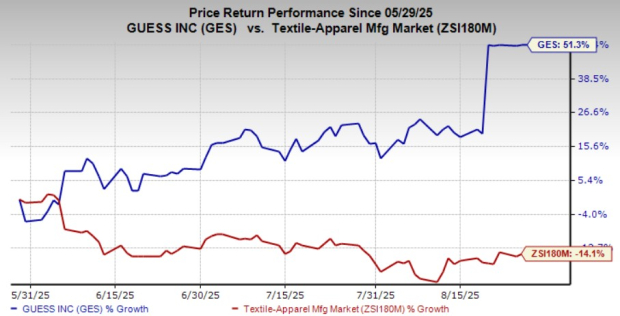

Shares of this Zacks Rank #3 (Hold) company have risen 51.3% in the past three months against the industry’s 14.1% decline.

Ralph Lauren Corporation (RL) designs, markets and distributes lifestyle products in North America, Europe, Asia and internationally. It currently flaunts a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for RL’s current fiscal-year sales and earnings indicates growth of 6% and 19.8%, respectively, from the year-ago reported figures. Ralph Lauren delivered a trailing four-quarter average earnings surprise of 8.5%.

Revolve Group, Inc. (RVLV) operates as an online fashion retailer for millennial and Generation Z consumers in the United States and internationally. It carries a Zacks Rank #2 (Buy) at present. Revolve Group delivered a trailing four-quarter average earnings surprise of 48.8%.

The Zacks Consensus Estimate for RVLV’s current fiscal-year revenues implies growth of 6.8% from the year-ago actuals.

Hanesbrands Inc. (HBI) designs, manufactures, sources and sells a range of innerwear apparel for men, women and children in the Americas, Europe, the Asia Pacific and internationally. It has a Zacks Rank of 2 at present. HBI delivered an earnings surprise of 56.1% in the trailing four quarters, on average.

The Zacks Consensus Estimate for Hanesbrands’ current fiscal-year earnings indicates growth of 65% from the year-ago reported figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-10 | |

| Jul-07 | |

| Jul-02 | |

| Jul-01 | |

| Jun-12 | |

| Jun-11 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-04 | |

| Jun-04 | |

| Jun-04 | |

| Jun-01 | |

| May-29 | |

| May-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite